Our mental models about mobility—individually owned cars, gas stations, traffic jams, the driver’s license as a rite of passage—are on the verge of disruption. Mobility is about to become cheaper, more convenient, a better experience, safer, and cleaner—not 50 or even 25 years from now, but perhaps within a dozen.

We describe the coming transformation as mobility’s Second Great Inflection Point, because it has the potential to be as profound as the one that put horses to pasture and revolutionized industries and societies worldwide. A defining characteristic of the new world taking shape is that the automotive industry, which has operated for more than a century alongside but decidedly disconnected from other components of what transportation has come to mean, will blend into a more interconnected, customer-centric ecosystem. That shift boosts the odds that the momentous changes afoot will affect your business, even if the closest you currently get to a car is your morning commute.

In a companion article, we describe the pressures on the old model, the bursts of innovation (ranging from vehicle autonomy and connectivity to electrification and ridesharing), and the evolving expectations that are propelling us toward the second great inflection point (see “Mobility’s second great inflection point”). Here, we drill down on what lies ahead: How exactly will cars, roads, and the customer experience soon be changing? (Think mainstream electric vehicles [EVs]; robots reading maps; interconnected, intelligent infrastructure networks; and, for a growing number of situations, “pay per use.”) What does that portend for competitive dynamics across the broadening mobility ecosystem? (As profit pools reorder and business models transform, opportunities will arise for a wider array of players, challenging OEMs’ notions of their competitive sets.) What are the implications for society, and what speed bumps may we hit along the way? Finally, how should leaders who aren’t yet immersed in the mobility revolution prepare for its imminent arrival? Fresh thinking about industry borders, adjacent opportunities, transport and logistics, and partnership possibilities are all needed.

Glimpses of the near future

For the past century, the automotive sector has been siloed—on multiple dimensions. Out of the approximately $8 trillion to $10 trillion spent each year on the transport of people and goods, “only” about a quarter comes from what is commonly understood as the car industry. Those businesses are as massive as they are separate. Fuel and energy, financial services such as insurance and financing, and maintenance all represent more than 10 percent of the total pie. You can’t use your car without them—and yet they are all disconnected from the automotive industry itself.

Automobiles also are disconnected from one another. Cars cannot be tracked and therefore cannot be guided. Traffic jams are one major result. Another is congestion pricing (fast lanes for those who can afford them). Pollution, made worse from idling and the search for parking, is another severe consequence. Car accidents, injuries, and fatalities—overwhelmingly the result of human error—occur every day. The second great inflection approaching will break down silos, with profound consequences that start with our cars, roads, and the customers who use them.

Cars

The more interconnected mobility system starts with the cars themselves. Electrification and vehicle autonomy, which are coming fast, stretch the capabilities of traditional OEMs. Less than 5 percent of vehicles sold in 2016 were equipped with EV power trains. Major OEMs have announced that they’re aiming to bring that number above 50 percent by 2021.

By 2030, EVs will be mainstream—and not just within the premium segment, as they are today. Nor, for that matter, will EVs be confined to passenger automobiles. Electric buses, trucks, and other delivery vehicles are rolling toward commercialization at an accelerated rate. (For more, see “The public–private imperative in urban mobility: A view from Canada.”) The changes won’t be “one-offs.” To the contrary, they will be magnified by shifts across entire fleets because of the lower costs of electricity as opposed to gasoline, the lower maintenance costs, and the lower overall total cost of ownership.

But that’s just the start. In 2016, only about 1 percent of vehicles sold were equipped with even partial autonomous-driving technology. As of this writing, however, eight of the ten largest OEMs plan to have highly autonomous technology road ready by 2025. Google’s Waymo has already launched a commercial taxi service made up of autonomous vehicles (AVs), in 2018; Uber plans to do so this year, and Lyft in 2021. By 2030, 80 percent of Chinese, European, and US miles will be at or approaching self-driving. That’s not just “hands off the wheel”; it’s drivers’ minds off the road. Indeed, since the function of driving will increasingly be performed by the car itself, cars will no longer need to be designed around the driver, except to the extent that, through advanced artificial intelligence, vehicles will be made to intuit what each passenger wants.

In many respects, a car will not even look like a car, at least as we know it today. As Carsten Breitfeld, CEO of China-based luxury EV OEM Byton, points out, without an internal-combustion engine, key elements of the interior (including the dashboard and the center air-conditioning console) can be shifted in radically space-saving ways (see “New carmaker on the block: Byton’s CEO on China’s car of the future”). With autonomous, connected, and shared vehicles, the changes will go much further. When a vehicle does not need to be designed around a driver, many fundamental tenets of auto design will go by the wayside. Why have a steering wheel? A driver’s seat? For that matter, will you need so much steel when safety requirements change? The design possibilities are fascinating—and the second-order effects for nonautomotive industries could be massive.

Roads

Disparate roads and highways—as well as different forms of transportation (buses, trains, airplanes, and even micromobility solutions, such as bicycles and scooters)—will increasingly converge into integrated networks. Early examples are already appearing in Singapore and Barcelona, where strategically placed sensors receive, process, and integrate enormous amounts of data to improve traffic flow, rationalize parking, and keep environs cleaner. Mobile apps such as Germany’s moovel and Finland’s Whim can now analyze a range of public- and private-transit options to identify the fastest and cheapest route from A to B and let mobile users reserve and pay for their journey. That kind of functionality will be scaled and available for consumers around the world by 2025.

Customers

Ecosystems, by definition, arrange themselves around the consumer. This makes it easier, faster, and cheaper for people to choose what they actually want. Consider, for a car, “freedom” and “machine.” Which element matters most? In a highly consumer-centric system, people can have freedom—indeed, even more freedom—without having to buy their own vehicles, search for parking, and pay for fuel (and a list of other expenses). Order pizza, get to work, take the family to the beach—when these use cases can be addressed with a swipe, the make or model of the car involved may matter less. (For more on the changing nature of automotive brands, see “Snapshots of the global mobility revolution.”)

Would you like to learn more about the McKinsey Center for Future Mobility?

What will matter—what has always mattered—is customer experience. As more people come to “consume mobility,” that experience will include:

- on-demand, pooled autonomous ridesharing as a part of the public-transportation system

- mobile games for commuters to play against one another en route, while the data generated by those games is used to help optimize traffic in real time

- more vehicles on the road moving more quickly, sped along by a municipality’s intelligent traffic-management tools

- air-quality sensors, which track specific sources of pollution and regulate traffic and construction accordingly

That’s fact, not fantasy. These examples are starting to happen in major cities around the world.

Competitive dynamics

In the past, OEMs competed primarily with one another. In the years ahead, consumers will focus more on different mobility operators, intensifying competition between OEMs and other mobility providers on dimensions such as utility of the interior, quality of the service, and sophistication of the connected-car experience.

Those new competitive dynamics will take place in the context of drastic changes in the economics of mobility. Today, OEMs are making about one cent in profit per mile driven. New mobility services have the chance to up this by a factor of ten to 25. Automotive companies are also very well positioned to capture monetization opportunities from car data. Our research finds that, so far, automobile consumers around the world are highly willing to share their data when they experience value in return.

That said, it won’t be easy to gain a defensible position across the critical technologies of autonomy, connectivity, electrification, and shared mobility. By our analysis, a company would have to invest nearly $75 billion, much of it going toward electrification and autonomy, to do so. While the new technologies will doubtless generate enormous value, no one can say where the economic profit will flow—and when. At any inflection point, value shifts quickly and unpredictably, and consumers tend to capture more of it.

This is especially so in the digital age. Encyclopedias, newspapers, camera film—when products turn into services, people pay a lot less. In fact, they may not pay at all. In the United States alone, the internet provides consumers about $100 billion of free welfare gain every year. It’s quite possible that a similar dynamic will play out as mobility becomes less about the car and more about a service. As happened with the mass adoption of both the internet and smart mobile devices, the life changes will seem almost imperceptible at first—then overwhelming, and inevitable.

Societal shifts

An inflection point is not an end point. It’s a redirection—the launch of a new trajectory. We can already see the pace of change begin to quicken. EVs, outside of the premium segment, have become commercially relevant only within the past three to five years. As late as early 2013, few were searching for “Uber” on Google.1 Carsharing was novel, too. Developments such as these will further speed up the change dynamics, both because adoption is driven by B2B and B2G enterprises rather than B2C businesses and because “ticket size” is much smaller.

The sum of individual decision making—choosing to pay fractions for a trip instead of many thousands for a car—will have enormous effects in the aggregate. Just as mobility’s first great inflection point reshaped society in ways initially unimaginable, the changes this time will reach far beyond the cars we drive (and increasingly, the vehicles in which we are driven). Those effects could include:

- Where people live. If things break right, commutes will be faster (for more, see “The road to seamless urban mobility”). Suburbanization will increase in many areas, a consequence of the first great inflection point once again in vogue.2 At the same time, because in-city congestion will be more manageable and parking less of an issue, urbanization—especially among younger people—will rise even faster.

- How people live. Riders will be safer and will have more free time, both during their journeys and as a result of the cumulative hours saved from digitally connected roads driven by AVs that are optimally paced, optimally spaced, and free from human error. Commutes will no longer be an exercise in frustration. In fact, work itself will change. As more people become able to start their workdays in the car, commuting time will increasingly count toward the eight-hour workday—enabling people to spend more time on other things, or more time working. Our colleagues estimate that the time saved by commuters worldwide could add up to a staggering one billion hours—every day. That’s twice the working hours it took to build the Great Pyramid of Giza.

- How people consume. The separate steps between contemplating a purchase and actualizing it will be compressed into a few swipes. Mobility has always had enormous implications for retail (the first pizza delivery was made in the 19th century). Just as Amazon has had the effect of increasing volumes shipped, a more integrated mobility ecosystem will make near- and far-distance purchases easier and faster. It will also make them cheaper: our colleagues in McKinsey’s Consumer Packaged Goods Practice estimate that fully autonomous vehicles could reduce grocery-delivery costs by 50 percent. With OEMs, ridesharing providers, and others investing significantly in solving the “last mile”—or “last 50 feet”—link of mobility, customer satisfaction will greatly increase. Consumers will come to use AVs to shop for everything from groceries at the local supermarket to accessories at the Apple Store downtown.

- What life looks like. When London experienced its precar “Great Horse Manure Crisis,” in 1894, there were 50,000 horses in London; find one there today, and you have found a tourist attraction. Just as the car transformed what the world looked like after the first great inflection point, our world will change, too. Slowly at first, but then much more rapidly, we will see gas stations, parking lots, and traffic jams become things of the past. Fumes and emissions will diminish. “Big digs” for mass transportation will be scaled down as well, since on-demand AVs can be at least as efficient. Air and ground shipping could converge if delivery drones and droids become mainstream. All in all, life should be greener, cleaner, safer, and, we expect, better.

Still, changes are rarely seamless, and big changes can be especially bumpy. Net-net, the benefits will decisively outweigh the costs. The harder question ultimately is not whether these changes will happen (they will) or when they will start (in many cases, they already have) but what the best ways to manage the transition are.

The shift to a mobility ecosystem will doubtless hit some speed bumps. Some of these we can probably foresee and, ideally, prepare for, such as cyberattacks on transportation systems or accidents resulting from systemic failures. Additional risks—more likely earlier in the inflection—include the perception of major failures and the unfortunate tendency for a wired-in, social-media world to sensationalize small incidents beyond reasonable proportion. The loss of millions of jobs for truck drivers and taxi drivers is unquestionably a cost, even as the transformation will create a range of new employment opportunities with potential for higher earnings and greater value creation, such as AV and EV technicians, and even trained attendants for disabled and elderly persons traveling by AV (for more, see sidebar “Redefining what it means to be a ‘car person,’” in “Mobility’s second great inflection point”).

Finally, beyond any futurist’s vision are the “unknown unknowns.” Is there such a thing as being too connected? How will geopolitics realign if oil is no longer the prize? What comes next in our collective imagination when stylish rides are replaced by more utilitarian use cases? Sooner or later—and probably sooner—we will find out.

A call to action

As the second great inflection takes hold, many businesses that do not consider cars to be close to their core industry will find themselves confronting an increasingly far-reaching mobility ecosystem.

There are some obvious first-order effects, starting with how business gets done. Logistics costs will be reduced—in certain cases, dramatically (our colleagues estimate that autonomy in delivery could reduce costs by upward of 40 percent). Long-haul routes will be shortened, too, as 3-D printing reduces the need for some long-distance shipments. Shippers can transport to fulfillment centers or urban drop-off zones, and smaller, purpose-built AVs will be able to handle things from there. Moreover, businesses will be able to become more agile—a capability that they will need in order to meet the demands of their customers, who will expect more products more quickly.

But the implications of the second great inflection point extend much further. Within a decade, the developments we’ve been describing will start having strategic ramifications for a wide array of companies. Here are some early priorities for everyone:

1. Adjust your sideview mirrors

Clear industry borders and siloed business sectors won’t stay that way for long in the new mobility ecosystem. For leaders outside of the automotive, transportation, or energy sectors, those changes can spell both threats and opportunities. Threats, because new competitors and attackers can appear from wildly unexpected directions: just consider the impact that advanced digital mapping had on publishers such as Rand McNally or, for that matter, the consequences that a growing market for EVs can have on the prices of laptop computers (the batteries of both rely on lithium, which tripled in price over a recent ten-month period). And opportunities, because the expanding mobility ecosystem can bring new customers and markets.

Can auto insurance—and insurers—keep up with the changing nature of mobility?

The coming mobility shift will have disruptive implications for auto insurers. Self-driving features should lead to safer cars, fewer accidents, and, ultimately, to lower premiums. It’s also possible that fewer people will own cars, with on-demand services making ownership an option, not a requirement, for more people. Those passengers may need different, short-term policies, not year-long comprehensive coverage. And over time, driverless cars could place more of the safety onus on manufacturers than on “drivers.”

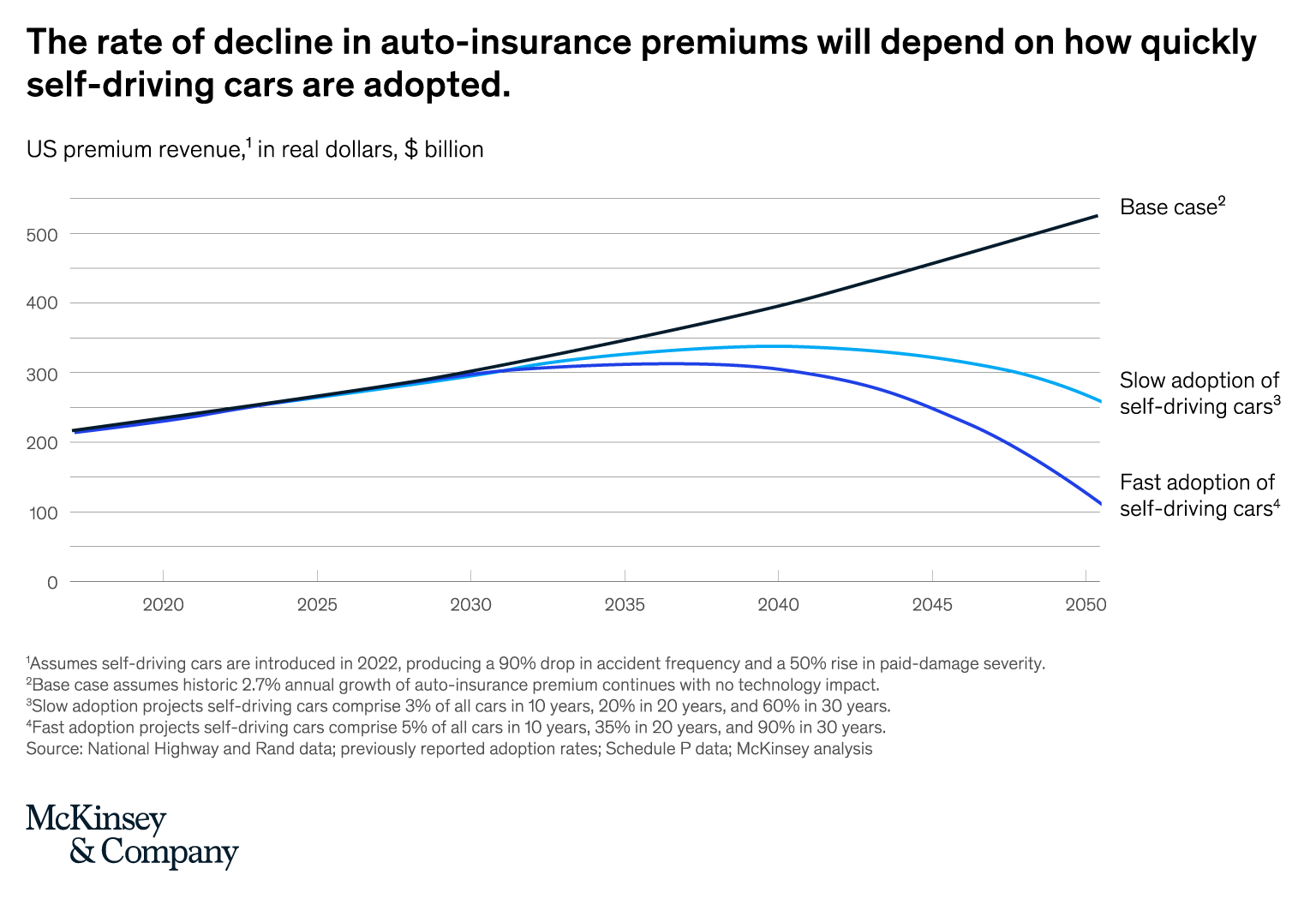

While the precise timing and extent of these changes is still hazy, it seems all but certain that auto insurers’ traditional premium pools will decline in the future. The exhibit below illustrates the impact of different autonomous-vehicle adoption-rate assumptions on premiums—which, in any scenario, are unlikely to be dramatically affected for a decade or so, but then could weaken rapidly.

So even as insurers strive, in the near term, to make their businesses hum amidst relative stability, they must simultaneously create options and reallocate resources to boost the odds of thriving when the inevitable inflection takes place. Consider, for example, insurers’ ownership of car-safety data. While currently a source of strength, it could prove tenuous as automotive OEMs build more real-time connections between cars and consumers—suggesting a need for increasingly sophisticated data strategies. Many insurers also have near-term opportunities to digitize and automate their businesses, thereby creating savings that can be redeployed to fund improved understanding of likely trends and consumer behaviors in the emerging mobility ecosystem. And now is the time to start exploring and investing in the products and partnerships of the future. One possibility: working with fleet providers to offer “part-time” insurance that consumers can buy via apps on their phone when they hail a ride. Another example would be partnering with OEMs to own the risk of manufacturer fault.

The opportunity—a broadening of the insurer’s role—is significant, and so are the dangers. The race is on to define a path connecting today’s realities with tomorrow’s uncertainties.

The first order of business is to figure out your role in the new mobility ecosystem. Ask yourself and your team where your business might fit in this new landscape—and who else might be entering the picture (for more, see sidebar, “Can auto insurance—and insurers—keep up with the changing nature of mobility?”). Focus on your core sources of value and key customer relationships. How can these be used to your advantage in a multidimensional game? The onus to scenario-plan can’t be on the C-suite alone. Encourage those closer to the front lines to do the same. Expect some internal resistance—“our business has always been this way.” It’s hard to get your team to think and act creatively to prepare for the threats and opportunities of the coming inflection point, and simply passing along the information won’t cut it. Embolden your employees to imagine what they would do differently under different circumstances. Incentivize them to get in front.

2. Objects are closer than they appear

Does it seem like just yesterday that you saw your first iPhone? So near in time—and yet such an epochally different world. Keep that frame of reference in mind as you prepare for mobility’s second great inflection point. Relatively speaking, it won’t be long before AVs deliver at a click, commuting patterns change, and car travel becomes “always on” and “wired in.” To a surprising degree, we know the future; we just don’t know—and are more likely to under- than overestimate—how soon it will arrive. Take advantage. Test out pilots where you can gain knowledge in connected businesses (there’s no lesson better than first-hand experience); track your progress with actionable timelines and incentives; and acquire and develop talent prepared for the coming changes.

3. Merge ahead

How Progressive CEO Tricia Griffith is preparing for the future of mobility

We certainly can’t predict the future, but we’re actively tracking and continuously studying not just autonomous technology but the wide range of new technologies that are being developed, to understand how they’ll impact our customers and insurance-loss costs. We also are closely tracking the evolution of mobility trends such as subscription services. While it’s not yet clear how quickly these emerging models will displace traditional vehicle ownership, we’re taking steps to position our business to learn about these changes. For example, we are a leading commercial insurer of Uber for their ridesharing platform.

One advantage we enjoy is lots of data. Through Snapshot, our data-collection engine, we’ve amassed more than 25 billion miles of trip data, which has shown us that driving-behavior data is the most predictive variable we have for auto-insurance pricing. Additionally, we work with original-equipment manufacturers, third-party intermediaries, and a variety of other key stakeholders to ensure we gain immediate insight into what’s next in the industry—so we can project out accordingly and stay ahead of the curve. That includes integration between Snapshot and GM’s OnStar program, and participating in the University of Michigan’s Mcity, which is an autonomous- and connected-car R&D initiative. All that helps us to learn about new technologies, new methods of data collection, new driving behaviors, and their potential impact on the insurance industry.

Both the fluidity of ecosystem dynamics and the agility needed to meet customer needs rapidly mean that your competitors—present and potential—may be active in different business models and multiple technologies. No single player will have the resources or capabilities to capture, defend, and win in manufacturing, designing, mechanical engineering, software development, artificial intelligence, and all the other areas associated with the mobility changes. Meeting your customers’ needs will require serious collaboration, which many companies aren’t prepared for. Start by identifying the “white spaces” you need to fill, the partners that can best help with those gaps, and the “gives” and “gets” genuinely required. Most of all, think strategically about how to best position yourself—and with whom.

4. Share the road

Social factors have always been a significant part of the mobility equation. Henry Ford prioritized an affordable wage and created a base of loyal car-buying employees, which had a multiplier effect on sales. Environmental responsibility turns EVs into premium brands. And Waze built its business by building a community. As the second great inflection point approaches, social considerations and public–private cooperation will take on outsized importance. Consider safety protocols, for example: no single player will be able to set the safety standards alone; nor can a government simply dictate them without a deep understanding of player capabilities. Or pooling and robo-shuttles for people and goods: governments and communities will determine mundane but mission-critical details, such as designated pickup, drop-off, and parking spaces. To win in the second great inflection point, develop a well-considered perspective on present and future regulations. And more: Think about how your success ties into the benefit of others. Ecosystems are inherently interconnected. Those that bear societal considerations in mind will be the most connected of all.

As mobility becomes cheaper, more convenient, more attuned to human and business experience, cleaner, and safer, business and society will be transformed. We’ve seen seismic change of that order unleashed when Henry Ford popularized mass production and Alfred Sloan took the organizational construct to new levels. The 20th-century disruption was swift and certain—not just for carmakers but for businesses around the world. Yet few saw those changes approaching. Now, about 100 years later, we’re at the precipice of a second great inflection point. While much uncertainty remains, the transformation is, in many respects, already here. It’s clear that those who aren’t prepared will risk failing one of the 21st century’s early tests.

CGI illustrations created expressly for McKinsey by Peter Crowther