In 1987, the Nobel Prize–winning economist Robert Solow famously said, “You can see the computer age everywhere but in the productivity statistics.” The same discrepancy is visible today: equity markets have revalued AI-exposed stocks in anticipation of efficiency gains and creative destruction, and US data suggests an AI-driven productivity boost. However, in the UK, this uplift is not yet evident in UK productivity data. Despite the intense attention AI has attracted, most UK businesses are not yet adopting—or even planning to adopt—AI to improve productivity. And where AI is deployed without a clear focus on benefits realisation, productivity gains are often lost through leakage. However, leading firms are already translating AI’s potential into business performance, increasing pressure on laggards to adapt. Through competition, these gains can eventually show up across the economy. Firms that recognise this—and act purposefully—are likely to shape the next chapter of UK productivity growth.

The productivity potential of AI is real

As early as 2023, just months after the release of ChatGPT, McKinsey Global Institute estimated that, in technical terms, 60–70% of all hours worked globally could be automated using existing technology. Since then, AI — including large language models and agentic systems — has advanced rapidly in capability and scopei.

Carefully controlled studies show measurable productivity gains for workers assisted by AI: software developers produced around 26% more completed tasksii; call-centre agents resolved 14% more customer issues per houriii; and mid-level professionals spent around 40% less time on routine writing and analysisiv. In marketing, human-AI teams were 73% more productive and produced higher-quality copy than human-only teamsv. In product development, individuals using AI matched the performance of two-person teams working without AIvi — illustrating AI’s potential to accelerate innovation, a critical driver of productivity growth.

These findings broadly align with individuals’ and managers’ perceptions. In a recent UK surveyvii, nearly 60% of respondents said they considered AI to be a productivity opportunity, and among those businesses that use AI, 75% said they had seen an improvementviii. Emerging academic research at the firm level finds productivity gains of around 4% from AI adoption, with effects varying depending on how AI is deployedix. McKinsey’s State of AI 2025 survey similarly found that a small subset of firms—AI high performers, representing around 6% of respondents—attribute significant value (around 5% of earnings before interest and tax) to their use of AI.

But AI is not yet showing up in UK productivity statistics

After years of post-financial-crisis and post-pandemic stagnation, there are some signs that UK labour productivity growth may be picking up. Between the third quarter of 2024 and 2025, official statistics put UK’s labour productivity growth at 1.1%. Experimental Office for National Statistics (ONS) real-time information (RTI), based on administrative payroll data, suggests an even stronger pickup, with output per hour rising by 3.0% year-on-yearx.

Any productivity acceleration remains tentativexi. But an improvement would be consistent with several underlying developments: improving management practices among UK businessesxii; relatively strong business investment since late 2021xiii, albeit concentrated in a small number of sectors; a recent uptick in business dynamismxiv; and a cyclical rebound following the post-pandemic period of flat productivity growth.

Is productivity growth also reflecting the effects of AI adoption? Based on the available evidence, that seems unlikely—at least so far.

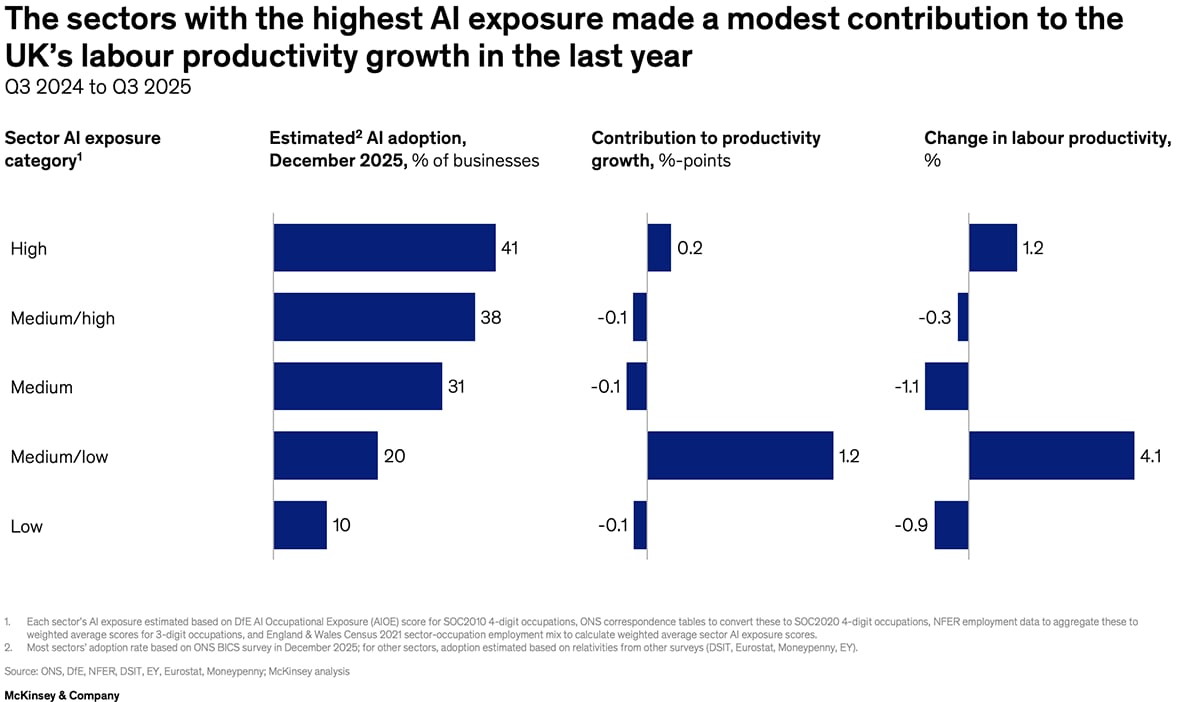

Over the past year, the largest contributions to UK productivity growth came from sectors with relatively low AI exposure and adoption (Exhibit 1), notably retail and wholesale, and business support services such as temporary staffing, cleaning, and facilities management. Highly AI-exposed sectors made a modest positive contribution—around 0.2 percentage points—with strong productivity growth in information and communication (ICT) and professional services offset by a negative contribution from finance and insurance.

The ICT sector’s strong contribution might, at first glance, be taken as evidence of an AI effect. AI tools have indeed made a huge difference to work in software development, computer programming, data processing, and related services. However, a comparison with longer-term trends gives a more ambiguous picture. Productivity growth in ICT over the past year was a healthy 4.6%, but still below the pre-pandemic baseline (trend growth from Q4 2014 to Q4 2019) of 6.5%.

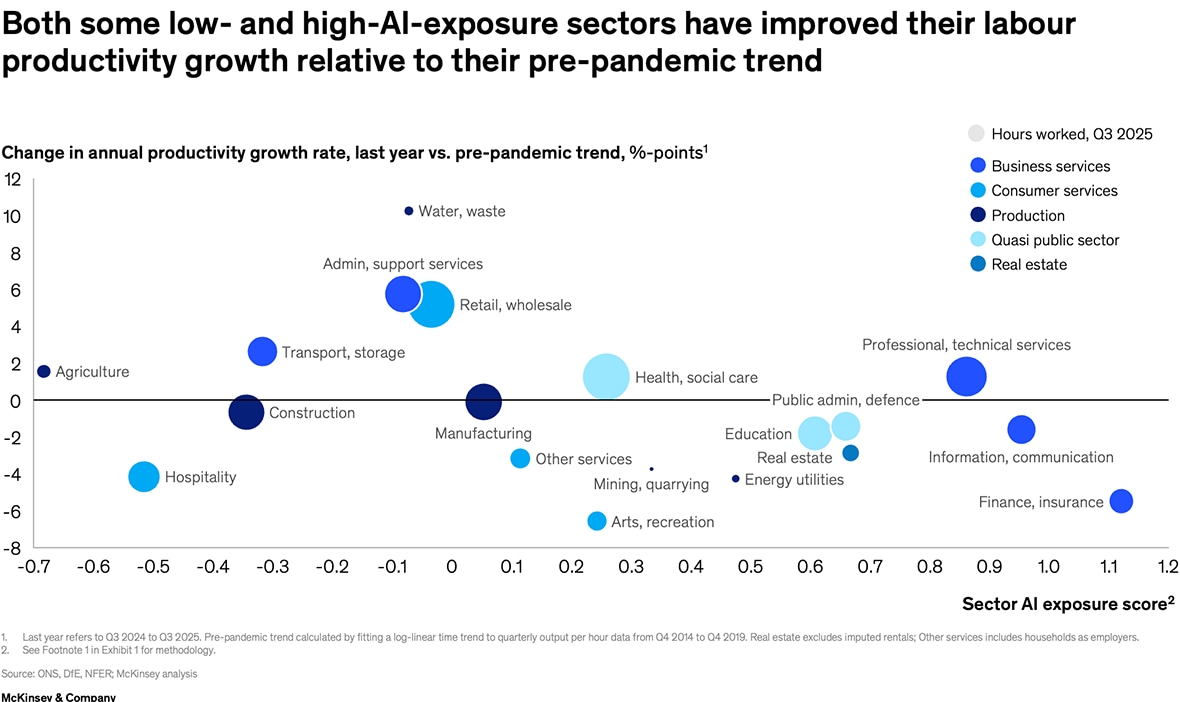

Comparing each sector’s productivity growth over the past year with its pre-pandemic trend shows no meaningful correlation between AI exposure and changes in productivity growth rates (Exhibit 2). Sectors with productivity accelerations include both low AI-exposure sectors—such as water and waste, business support services, and retail and wholesale—and high AI-exposure sectors, such as professional services. The same analysis at a more granular level, or over different time periods, shows a similarly mixed pattern.

Low adoption and high leakage explain the discrepancy

Three factors help explain the gap between AI’s productivity potential and measured productivity. First, most businesses—employing the majority of people in the UK—have not yet adopted AI in an active or intentional way, as distinct from passively consuming it. Second, even where AI adoption has occurred, a significant share of its potential leaks out at each stage of aggregation, from tasks and individuals through to firms, markets, and the economy as a whole. Third, not explored in detail here, is measurement: in many applications AI raises quality more than it saves time, and quality improvements are imperfectly captured in official statisticsxv.

A recent Department for Science and Technology survey usefully distinguishes between “passive consumers” and “active users” of AIxvi. Passive consumption refers to using AI-powered products—such as predictive text or online recommendations—without a conscious decision to use AI. Most of us have been using AI in this way for over a decade, embedded in services such as internet search, fraud detection, and real-time journey planning. Active use, by contrast, involves the deliberate deployment of tools such as generative AI chatbots, image generators, AI copilots embedded in enterprise software, and autonomous AI agents.

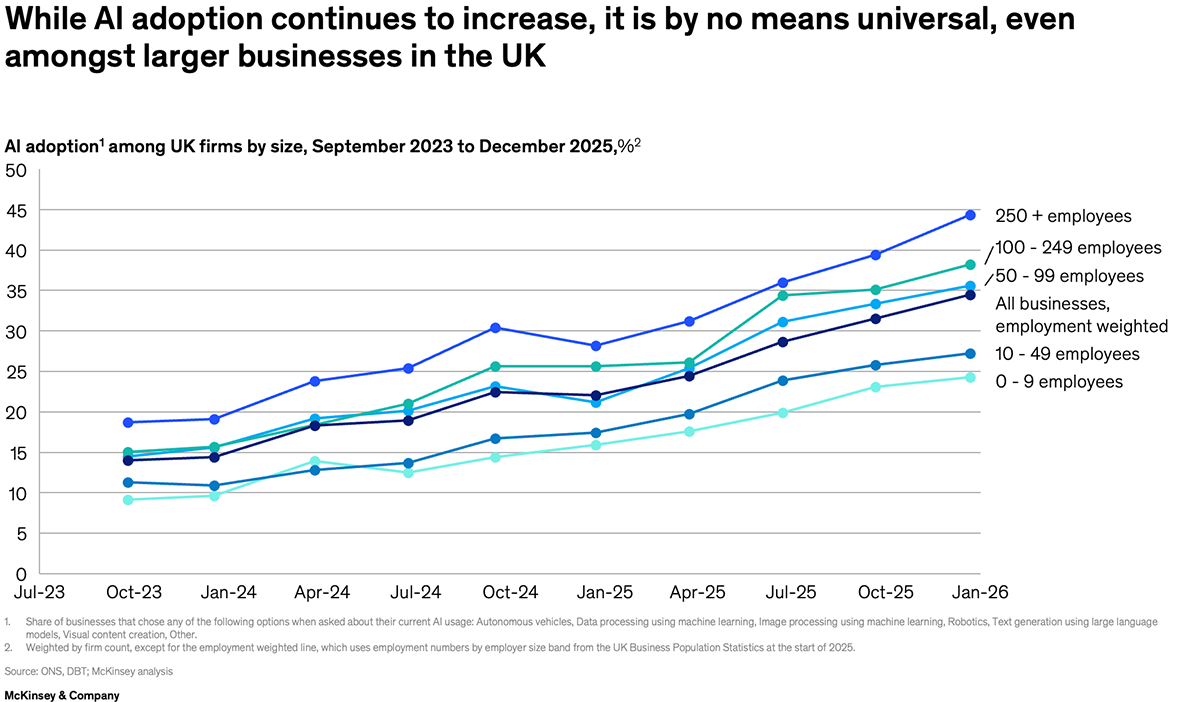

A related surveyxvii illustrates how limited active adoption remains. Fewer than a third of respondents said they were currently using AI in their business, and 60% said they were not planning to use AI at all. These findings align with ONS data showing that in December 2025, around 25% of businesses had adopted AI (using a slightly narrower definition). While both results reflect the predominance of small firms in the UK, Exhibit 3 shows that adoption is far from universal even among larger firms or on an employment-weighted basis.

Even where companies have adopted AI, its productivity promise often remains unfulfilled. Capturing gains requires upfront investment in data, IT, software, skills, and organisational change — and many firms remain in a phase where exploration and implementation costs currently exceed realised benefits.

This phenomenon is often described as a delayed payoff from new technologies. But crucially, later gains are not automatic. Without purposeful changes to how work is organised and resources are allocated — and without securing broad managerial and frontline buy-in to new ways of working — productivity benefits can dissipate through leakage at every level of aggregation. Illustrative examples inlcude:

• At the task and individual level, a software developer who saves time using AI-assisted coding may reallocate their time towards other, potentially less productive, activities rather than generating more or higher-quality output;

• At the individual-to-team level, radiologists who could deliver the same diagnostic outcomes in half the time by working with AI rather than each otherxviii may find it difficult to change working patterns, or face resistance to change;

• At the team level, a small customer service unit may boost productivity with AI but still fall short of saving enough resources to reduce headcount or may be reluctant to reduce workers’ hours due concerns about equity or morale;

• At the function level, finance or compliance teams may keep humans in the loop at every stage for risk-management reasons, even where the downside risks of fully delegating specific workflows to AI are tightly contained;

• At the firm level, a company trialling AI across multiple areas may realise many small benefits but fail to adjust budgets or resource allocation to cash in on the efficiencies;

• At the market level, a business that improves its competitive position through AI may struggle to win market share quickly, due to switching costs, brand loyalty, customer risk aversion, or market conventions;

• At the economy level, productivity gains in fast-improving sectors may be offset by labour shifting toward slower-productivity-growth, more labour-intensive sectors, dampening measured aggregate productivity growthxix.

These examples point to four sources of leakage: behavioural and cultural barriers that dissipate productivity improvements; coordination failures that prevent effective workflow redesign; reallocation inertia that blocks budget, staffing, and investment shifts; and competitive frictions that delay market-level gains. Together, they explain why AI’s productivity impact can remain latent — and why firm-level gains may not translate into economy-wide growth.

The mismatch creates a competitive opportunity

The gap between AI’s technical potential and measured productivity is not just a paradox; it is a competitive opportunity— particularly for firms willing to rewire the entire business, rather than simply automate isolated tasks.

When most firms struggle to convert AI-enabled innovation, quality, speed, and efficiency into performance and growth, those that succeed can pull ahead quickly. The advantage does not come from access to better models — which are increasingly commoditised — but from organisational and cultural changes anchored in visible ownership and sustained commitment from senior leadership. These include redesigning workflows, shifting decision rights, reallocating resources, updating performance metrics, and acting on opportunities rather than letting them dissipate.

One illustrative call-centre example found that moving to an “AI enabled” system—where AI supports humans—reduced case-resolution time by 5-10%. By contrast, an “AI agent enabled” model, in which the process was consciously redesigned around AI agent autonomy, cut resolution times by 60-90% and allowed 80% of basic incidents to be resolved automatically. Rather than keeping humans “in the loop” by default, leading firms classify decisions by risk and complexity—retaining human oversight for high-stakes or ambiguous cases, while positioning humans “above the loop” for routine, low-risk decisions.

The productivity advantage is likely to be especially pronounced for AI-native start-ups and scale-ups, which can design processes, products, and organisational structures around AI from the outset. Without legacy systems or entrenched ways of working, they can embed AI directly into core operations, bringing the marginal cost of many activities close to the cost of compute. These firms can therefore profoundly challenge incumbents on cost, speed, quality, or entirely new value propositions. But incumbents are not excluded from this opportunity: those that adopt early and tackle leakage head-on can also reshape their cost structures and competitive positions.

Over time, the resulting pressure—through new entry, expansion, and market dynamics—will drive creative destruction. As higher-productivity businesses gain share and less productive ones are forced to adapt or exit, improvements will spread from leading firms to the wider economy. McKinsey Global Institute research shows that in the US between 2011 and 2019, frontier firms scaling and gaining share added 0.6%-points to productivity growth, while the exit of unproductive firms contributed a further 0.5%-points. Overall, dynamic reallocation accounted for 0.9 of 2.1%-points of productivity growth. Over the same period, UK productivity growth among the sample of firms was zero.

The process of creative destruction is neither smooth nor guaranteed. Structural constraints, including the continued expansion of labour-intensive services with lower inherent productivity, may mute or delay economy-wide gains. But history suggests that when a general-purpose technology is combined with organisational innovation and competitive pressure, its impact eventually becomes visible in aggregate outcomes.

In that sense, today’s productivity paradox should be seen as a transition phase. Firms that recognise this—and act purposefully—are likely to shape the next chapter of UK productivity growth.

i https://hai.stanford.edu/ai-index/2025-ai-index-report

ii https://economics.mit.edu/sites/default/files/inline-files/draft_copilot_experiments.pdf

iii https://www.nber.org/papers/w31161

iv https://pubmed.ncbi.nlm.nih.gov/37440646/

v https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5187466

vi https://www.nber.org/papers/w33641

vii https://www.gov.uk/government/publications/ai-skills-for-life-and-work-employer-survey-findings/ai-skills-for-life-and-work-employer-survey-findings--2

viii https://www.gov.uk/government/publications/ai-adoption-research/ai-adoption-research#impact-of-ai-1

ix https://www.productivity.ac.uk/research/artificial-intelligence-and-firm-level-productivity-early-evidence-from-a-small-open-economy/

x https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/labourproductivity/articles/ukproductivityintroduction/octobertodecember2025andjulytoseptember2025

xi Note: At the whole economy level, productivity growth from Q4 2024 to Q4 2025 in ONS’s “productivity flash estimate” was negative, at -0.5%, while experimental statistics using payrolls data showed an improvement of 1.6%

xii https://www.ons.gov.uk/economy/economicoutputandproductivity/productivitymeasures/bulletins/managementpracticesintheuk/2016to2023

xiii https://www.ons.gov.uk/economy/grossdomesticproductgdp/bulletins/businessinvestment/octobertodecember2025provisionalresults

xiv https://www.resolutionfoundation.org/app/uploads/2026/01/Mountain-climbing-updated.pdf

xv https://assets.publishing.service.gov.uk/media/5a7f603440f0b62305b86c45/2904936_Bean_Review_Web_Accessible.pdf

xvi https://www.gov.uk/government/publications/ai-skills-for-life-and-work-general-public-survey-findings/ai-skills-for-life-and-work-general-public-survey-findings

xvii https://www.gov.uk/government/publications/ai-skills-for-life-and-work-employer-survey-findings/ai-skills-for-life-and-work-employer-survey-findings--2

xviii https://www.thelancet.com/journals/lancet/article/PIIS0140-6736(25)02464-X/abstract

xix https://www.nber.org/system/files/working_papers/w23928/w23928.pdf