For the past ten years, the rise of software as a service (SaaS) has reshaped the enterprise-software industry. During that period, the disruptors that pioneered the model and the incumbents that transitioned to it created tremendous shareholder value. Between 2011 and 2018, the global software industry’s market cap grew at twice the rate of the overall market. Yet that growth came with a cost: industry profitability tumbled, falling by half over the decade.1

The next ten years will not be any less tumultuous. As SaaS matures, the customer’s expectations around ease of use and ease of doing business will continue to rise. Platforms as a service (PaaS) from the Big Three cloud vendors (Amazon Web Services, Google Cloud, and Microsoft Azure) are gaining share and commoditizing software. And with financial markets reeling from the COVID-19 pandemic, investors are looking more closely at bottom-line health.

Addressing these demands will require software vendors to adopt a new playbook. Success will take a renewed strategic focus, a willingness to expand “as-a-service” offerings beyond subscription pricing, and a greater emphasis on profitable growth (see the sidebar, “Software’s new playbook”).

Customers want SaaS products and an SaaS experience

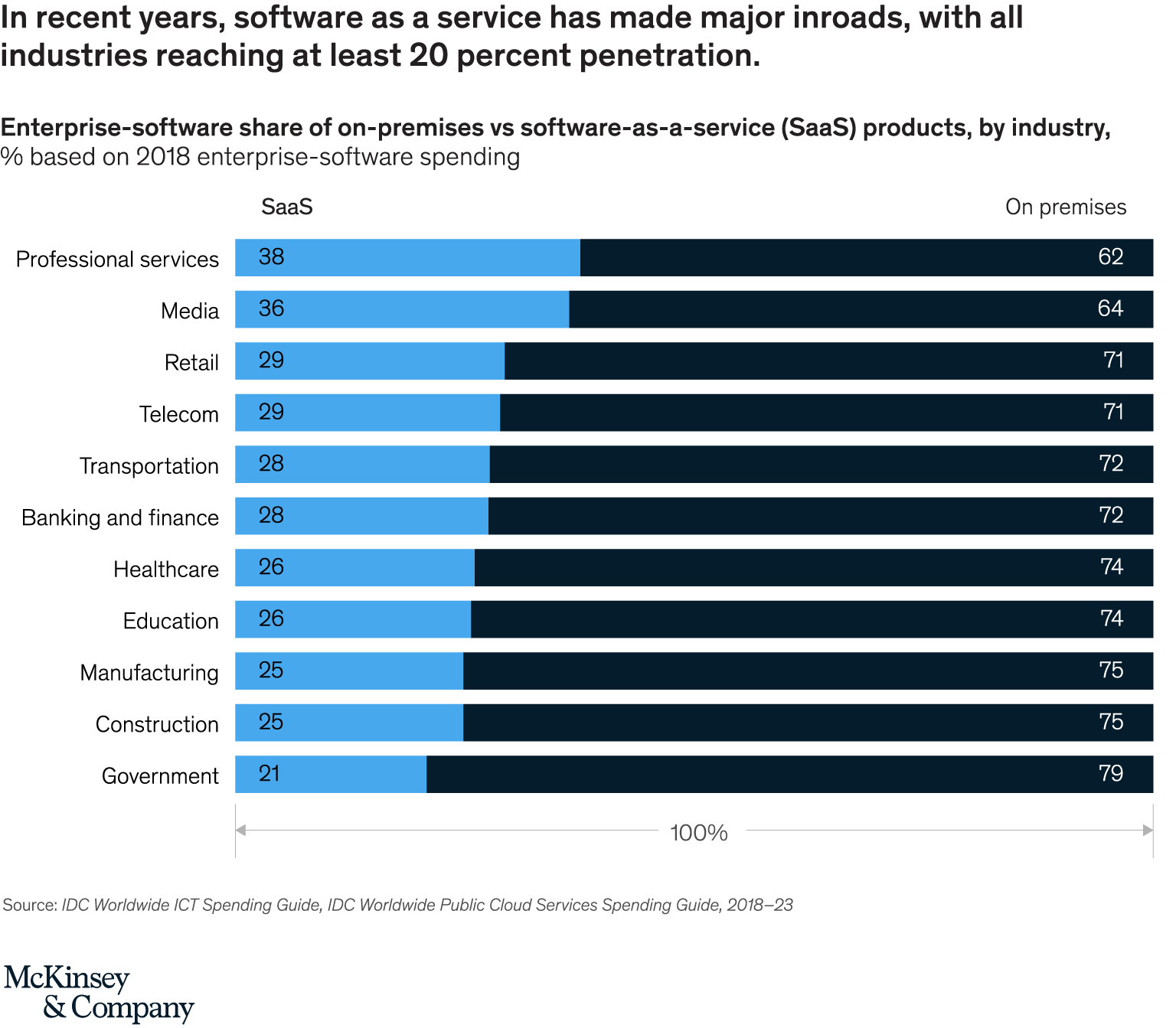

SaaS has become the default software-delivery model—and at breakneck speed (Exhibit 1). In 2010, SaaS offerings commanded just 6 percent of enterprise-software revenues. By 2018, that share had grown to 29 percent, or $150 billion globally. Yet that figure understates the true size of the market. When revenues from companies still transitioning to SaaS are counted, the total as-a-service share rises to 75 percent of all enterprise-software revenues, or more than $380 billion. Those numbers mean that companies with no SaaS offerings now represent only one-quarter of total industry revenues.

In a sign of the market’s maturity, late adopters have come on board. More than one-fifth of all government software spending now goes to SaaS. Even categories such as CAD, whose highly expert customer base would normally resist sweeping product changes, are making the transition.

Would you like to learn more about our Technology, Media & Telecommunications Practice?

Vendors that have not yet begun their SaaS transformation must do so now. The “next normal” established during the COVID-19 pandemic will accelerate the footprint of SaaS, given the growth of remote working, the rapid deployment of digital solutions, and the lower up-front costs.

To succeed with SaaS, however, vendors must do more than offer a subscription-pricing model on a product hosted in the cloud. They need to match the streamlined, customer-friendly as-a-service product-delivery experience with a similarly streamlined and customer-friendly end-to-end journey. Right now, the customer experience of many SaaS vendors often feels disjointed. All too frequently, for instance, legacy billing processes and order forms riddled with confusing product terminology make it hard for customers to know what they’re paying for. Leading players address these inconsistencies by evaluating the whole business in the as-a-service context and redesigning core processes to make them more intuitive and responsive (Exhibit 2).

For example, one software vendor launched a customer-success organization as part of its move to a subscription product. It also redesigned its quote-to-cash processes to simplify customer purchases and renewals. This holistic approach contributed to an almost 100 percent increase of its stock price over the eight quarters following the SaaS launch. Our own case experience shows that software vendors that embed an as-a-service focus across key functions can improve total customer lifetime value by 25 percent through reduced churn and increased upselling and cross-selling.

Vendors may need to specialize at the top of the stack and to partner elsewhere

In the 2020s, the headline disruption for many software companies will be the growth of PaaS. Between 2016 and 2018, PaaS revenues grew at nearly twice the rate of SaaS—44 percent a year versus 26 percent, respectively. Much of that growth came at the bottom of the software stack. The Big Three cloud vendors, with their vast scale and resources, have developed PaaS services that now rival those of the leading software vendors. The reach and financial muscle of the cloud giants allow them to innovate more quickly and to build and maintain these services at lower cost. Within the submarkets for systems infrastructure software (SIS) and application development and delivery (AD&D), the Big Three cloud vendors have seen their revenues grow by a compound annual rate of roughly 65 percent between 2014 and 2018, compared with just 4 to 5 percent for SaaS vendors (Exhibit 3).

The rise of PaaS has changed what it takes to be a successful enterprise-software vendor. As PaaS services become more sophisticated, software application vendors have a tougher time justifying a price premium for products that could be delivered with a thin user interface on top of generic PaaS services. With PaaS tools giving attackers and customers themselves the means to develop new applications quickly, software vendors that do not innovate in kind will face increased risk.

Enterprise software: An industry in transformation

Software vendors need to defend their share of the profit pool by taking a clear look at where they have the best and most defendable opportunities to differentiate themselves. Rather than going head-to-head with the Big Three, one strategy is to specialize and tailor solutions to the needs of targeted verticals and use cases. This strategy proved successful in the early 2010s, when SaaS disruptors first entered the market. The legacy-software vendors that were closest to the customer and had a high degree of industry and domain expertise protected their market share and maintained their enterprise value-to-revenue multiples while customers that stressed differentiation on the basis of their technology were more vulnerable (Exhibit 4).

Another strategy is to provide a cloud-agnostic experience for customers. Fearing cloud lock-in, some software customers are actively searching for AD&D and SIS tools that can work across their cloud deployments. Software vendors that meet this need quickly could unlock a value pool that the Big Three cannot touch. Still, in order to maintain this position, they will have to invest heavily to keep up with the Big Three’s pace of innnovation.

A third option for vendors is to strike strategic partnerships; for example, when Nuance Communications developed its Dragon Ambient eXperience (DAX) offering, it chose to partner with Microsoft. Nuance historically developed speech and AI applications in-house and continues to do so. However, complementary technical expertise and data-governance policies led Nuance to partner with Microsoft on DAX. By doing so, Nuance felt it could gain the benefit of investment at scale to advance state-of-the-art developments addressing clinician burnout.

This technology partnership, along with Nuance’s strong healthcare expertise and data-stewardship practices, would provide the most significant long-term opportunities for differentiation and accelerate DAX’s time to market. “The right partnership improves your agility to scale for value, to maximize competitive advantages, and to accelerate growth,” Nuance CEO Mark Benjamin told us. “The huge upside potential in our core healthcare and enterprise markets necessarily attracts large, cash-rich competitors. To truly differentiate, they need to build, buy, or partner for domain expertise. That’s why we looked to partner under the right business construct and made a competitor a partner.”

With investors focused on profitability, vendors need to optimize margins

Since dot-com days, the conventional wisdom in software was that growth is king and profitability is secondary. This mindset has shaped management behavior and investor attitudes. In recent years, however, market sentiment has begun to shift. Revenue growth used to carry a premium of up to 2.5 times free cash flow, but that gap has narrowed. Since 2015, SaaS natives have seen their growth premiums over free cash flow shrink to 1.7x. Meanwhile, legacy software companies no longer receive a premium for growth over free cash flow (Exhibit 5). The focus on cash flow will only intensify in the COVID-19 era.

Margin-focused initiatives must receive the right attention. Software leaders need to look function by function and identify areas where even modest restructuring can improve efficiency and the customer experience. Within sales, for example, many software accounts historically covered by field sales could be shifted to inside roles, a transition that new remote-working norms could accelerate. Our research shows that 80 percent of software buyers prefer remote sales over face-to-face interactions. If sales personnel spend less time on the road traveling to customer sites and meetings, they can spend more time with customers. Our data show that moving to an inside-sales model could reduce the cost of sales by as much as 60 to 80 percent per customer. Recognizing that potential, some software organizations have begun shifting accounts as large as $200,000 to an inside-sales-coverage model.

Businesses should also take a hard look at their product portfolios and winnow long-tail offerings that have little to no chance of ever making it big. To identify underperformers, companies must go beyond top-line numbers and get a complete picture of a product’s true profitability. Capturing the expense of maintaining a product in the sales bag, preparing financial analyses, processing invoices, and undertaking other administrative tasks can surface the hidden costs of complexity and help leaders make more informed asset-allocation decisions. Our research shows that software vendors that actively manage their portfolios and regularly divest underperforming products achieve enterprise-value-to-revenue multiples twice those of passive portfolio managers.

The disruption over the past decade proved that many legacy software players are remarkably resilient. Vendors will need to call on that resilience to weather the challenges ahead. By revisiting their strategic playbooks, investing in defendable and high-growth opportunities, and embedding smarter and more cost-effective ways of working across the organization, software vendors can secure a foothold and pave the way for a profitable next decade.