GET THE LATEST

February 24, 2025

In the time since this article was first published, McKinsey has continued to explore the topics it covers. Read on for a summary of our latest insights.

When this article was originally published in 2020, claims organizations were already under pressure to digitize, manage costs, and improve customer experience. What has changed since then is not the direction of travel, but the scale and speed of the opportunity ahead. Recent advances in artificial intelligence, particularly agentic and gen AI, have significantly expanded what is technically and economically possible in claims. While adoption remains uneven across the industry, the pace of AI experimentation and scaling is accelerating and is expected to fundamentally reshape how claims work is done over the remainder of the decade.

Against this backdrop, the core perspectives of this article remain highly relevant. Manual and routine cognitive activities continue to decline as automation expands. At the same time, demand for human capabilities—such as judgment, empathy, communication, and complex decision making—is rising. As AI frees up meaningful capacity in claims, value will increasingly come from how organizations redeploy that capacity toward higher-value work requiring deep expertise, accountability for outcomes, and empathetic engagement with customers to provide the best possible service in their moment of need. The emergence of agentic AI, with autonomous agents able to coordinate and orchestrate discrete parts of the claims process, reinforces the article’s central insight: As technology advances and adoption scales, the nature of claims work as well as the roles responsible for it are poised for fundamental changes.

The implication for claims leaders is clear. It is imperative to harness AI to redesign roles, workflows, and talent models to capture its full potential as experimentation gives way to scaled adoption. As the industry moves through the second half of the decade toward 2030, this article continues to offer a lasting framework for reimagining claims talent in an AI-enabled future.

The technology revolution is reshaping every job in claims organizations. McKinsey research estimates that by 2030 more than half of current claims activities could be replaced by automation: some existing roles will be eliminated, new digital roles will be created, and people in remaining roles will need to handle new responsibilities and build new skills. To keep up with the digital revolution, claims organizations need to prioritize the development of a talent strategy.

However, many claims leaders are not sure where to begin. The COVID-19 pandemic has only further accelerated digitization in insurance, as customers increasingly demand more options for digital interaction. Further, pressure to reduce costs because of continued profitability challenges has overwhelmed their ability to build a future-oriented talent plan. As a result, claims organizations get stuck in a holding pattern.

In “Claims 2030: Dream or reality,” we described how the claims experience will dramatically transform over the next ten years—because of rapid evolution in technology, analytic capabilities, and customer preferences—and we revealed new ways to protect the insured. To prepare for automation and the digital revolution, claims organizations must focus on talent. In doing so, organizations will be able to digitize their claims process ahead of the change and build a sustainable, competitive edge through speed and accuracy.

Claims organizations can take two actions now to design a talent strategy for the future of work:

- define the roles of the future

- grow future-ready talent

Organizations that get it right will realize significant performance improvement and ensure that technology and business work together, while those that miss the mark will likely be left behind.

Define the roles of the future

While future roles should be specific to each organization’s strategy, our research indicates that roles will fall into one of two likely categories: evolutionary and innovative. Evolutionary roles already exist in claims, though the work will be greatly improved by integrating new technology. Innovative roles are new roles that will help claims organizations explore fresh ways to protect the insured, and support the technology-driven future. These evolutionary and innovative roles illustrate how technology might shift future claims jobs, and they can help claims organizations start thinking about what future roles they will need to enable their claims strategy. These roles will also be the most common across claims, though they will differ depending on the organization.

Evolutionary roles

As claims organizations plan their talent strategies, the role of the claims handler will diverge based on claims complexity: simple claims will be handled in a streamlined and automated manner, while complex claims will be augmented with analytics and decision-making tools. The claims-quality assessor role will also adapt to include the assessment of technology and handler decision making.

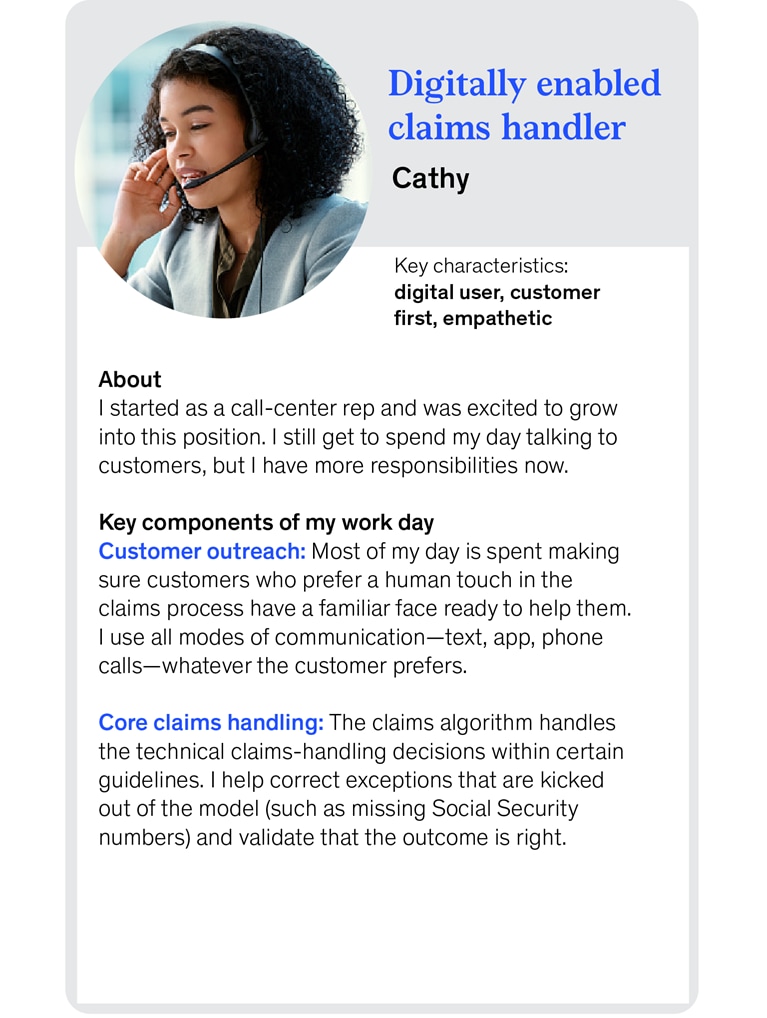

Digitally enabled claims handler. For simple claims, automation will handle the end-to-end technical adjudication, allowing digitally enabled claims handlers to shift the focus of their customer interaction from rote information gathering to providing proactive support and advice. While the world is becoming increasingly digital, many customers will likely still demand human interaction when filing a claim. In the future, the digital claims system will help drive proactive customer engagement by spotting opportunities for human intervention and making referrals—which could be based on a customer’s profile—to digitally enabled claims handlers.

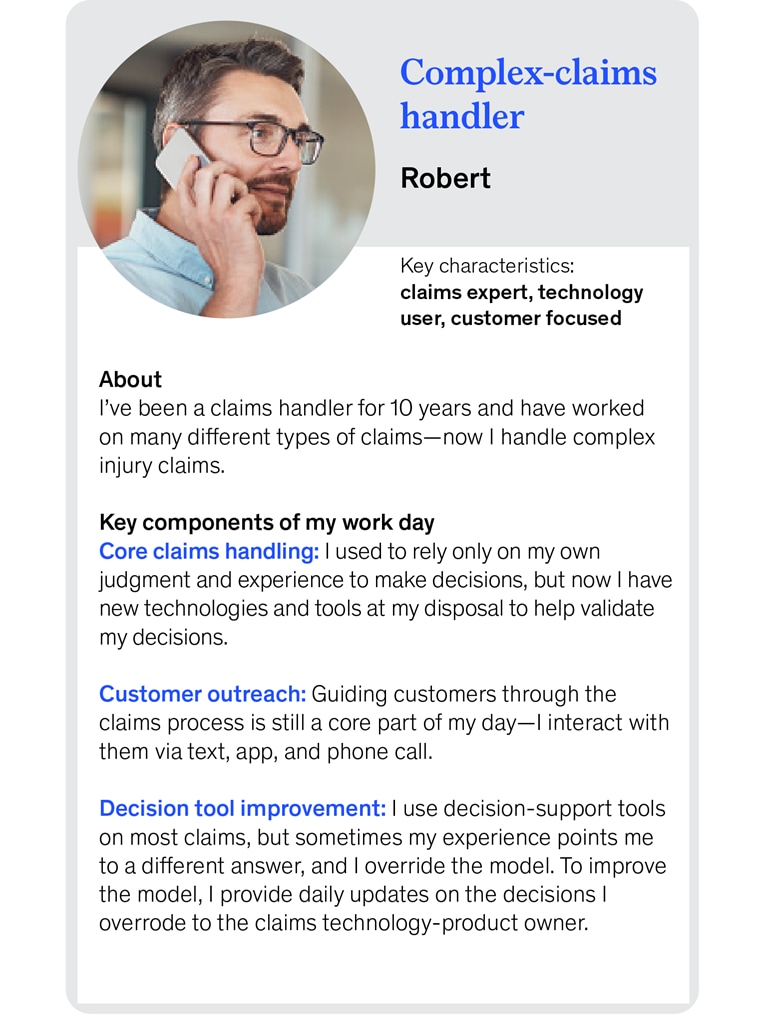

Complex-claims handler. For the foreseeable future, complex claims, such as injury claims and those involving litigation, will continue to require human judgment. However, new technologies such as those that can ingest and synthesize medical records will provide critical information to complex-claims handlers, enabling them to make more accurate decisions and close even the most difficult claims with increasing speed and accuracy. For this process to work, handlers will take on new responsibilities, such as clarifying the information they need to make decisions, and determining how to best integrate the information into their workflow. Over time, however, decision making will become automated by machine-learning models. To support this shift, handlers will be responsible for codifying how they make complex-claims decisions, to inform machine learning.

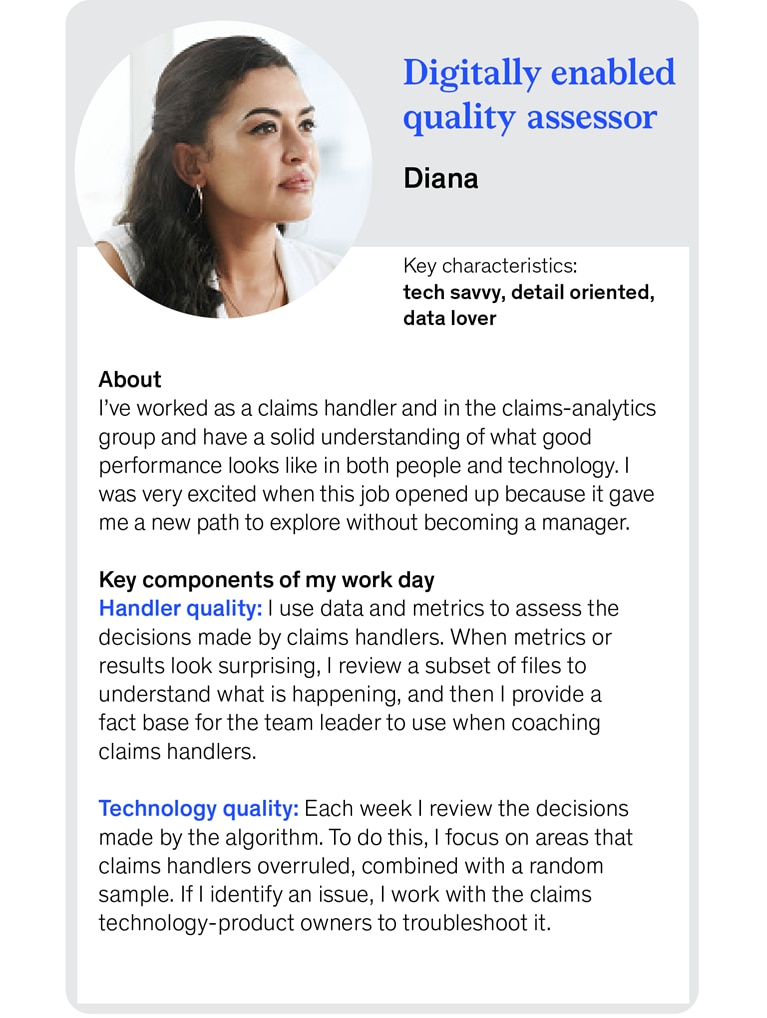

Digitally enabled quality assessor. A quality assessor’s main objective is to ensure the quality of claim outcomes. Over time, the scope of their role will expand from assessing only the judgments from claims handlers to include technology assessment. Assessors will become the standard bearers for what it means to properly process a claim; they will define the quantitative target for successful automation and validate that both handlers and adjudication algorithms can achieve it. Digitally enabled quality assessors will also help identify ways to improve nascent algorithms that may miss targets.

Innovative roles

Beyond assessing how current roles will evolve in the future, claims organizations will also need to invest in building new roles and capabilities.

While there are many flavors these roles might take, claims leaders should focus first on two innovative roles: the claims technology-product owner and the claims-prevention specialist.

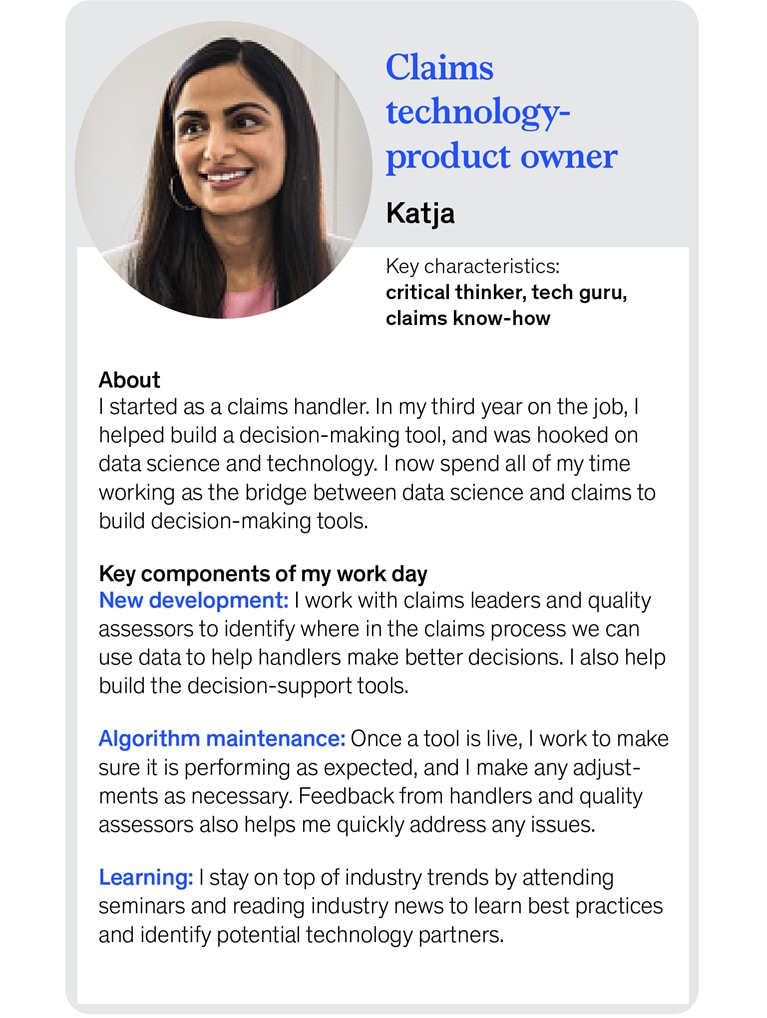

Claims technology-product owner.As automation evolves from process-centric automation to artificial intelligence that eventually replaces judgment-based work, algorithms will increasingly make decisions across key points in the claims process, from assessing coverage to assessing damage. While digitally enabled claims handlers and quality assessors will help validate algorithm output, claims technology-product owners will infuse technology and data science into the claims process. They will do this by designing, implementing, and maintaining algorithms using their robust knowledge of claims patterns and causes of loss. Individuals in this role will need deep claims-process experience, good pattern recognition, and fluency in technology.

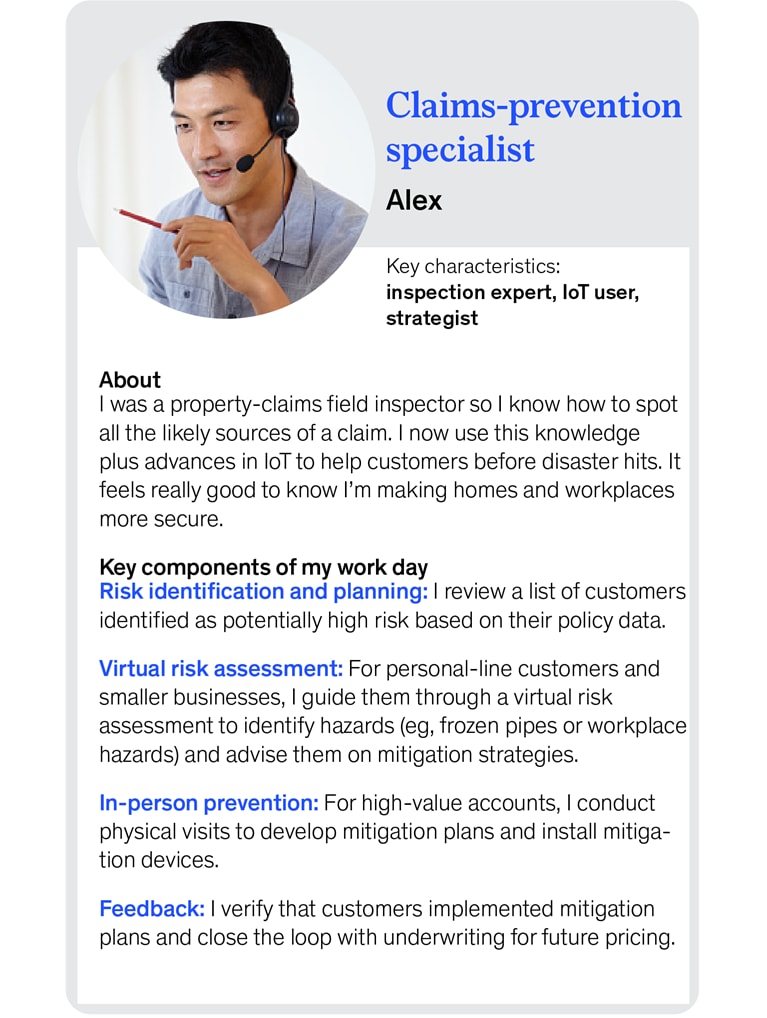

Claims-prevention specialist. Loss prevention is becoming increasingly important for claims organizations. Today, many are experimenting with prevention tools, such as “telematic” devices and IoT sensors. In the future, prevention specialists will benefit from telematics and precision analytics to help identify high-risk customer scenarios. Specialists can then conduct targeted and personalized outreach to mitigate the risks. They will also cement the link between underwriting and claims, providing additional input on incorporating policy risk into the pricing model. This feedback loop will enable insurers to provide better recommendations to customers on how they can lower their risk and maintain a healthy policy at the point of sale.

To start defining roles for their organization, claims leaders should reassess their strategic priorities and create a talent and capabilities road map that includes automation, digital tools, and machine learning. Leaders can then map the specific activities that will change by role—such as shifting investigation from physical to virtual—to understand how job responsibilities and the ways of working will change. Once claims leaders have a full view of how work will be done, they can develop new role profiles to capture new responsibilities (such as validating algorithm decisions on coverage) and create a plan for role transition.

Claims leaders will need to work role by role, and they can start either by defining a portfolio of new roles in a single line of business they understand well, or by identifying cross-cutting roles where future activities are already clear (such as claims handlers working in high-automation environments). With future roles in mind, claims leaders can begin by assessing their current skills, and then use their findings to develop programs that can help to transition individuals to future roles (see sidebar, “Identify the skill gap of future roles”).

Grow future-ready talent

Many claims leaders default to external hiring to acquire talent. While hiring externally can be a valuable approach (and one that leaders will likely need to leverage), many of the skills claims organizations will need are well within the reach of current claims handlers—and some may even have a base level of skills in critical areas, such as technical knowledge. Leaders can take three actions to prepare their existing workforce.

Assess current skills

Claims leaders that take stock of current skills and pivot from role-based to skill-based talent planning are realizing benefits. On the macro level, these leaders are identifying systemic development priorities and are optimizing overall development spending. On the micro level, leaders are uncovering hidden talent, achieving a greater impact through personalized development (both for individuals and for target populations such as women and people of color), and building more effective teams by staffing team members with complementary skills.

Most companies, however, have not yet built a robust baseline of individual skills, in part because legacy HR systems do not track skills well, and also because the information is hard to obtain, as it requires continuous evaluation and transparency. Enhanced employee-communication channels, external sources, and people analytics, however, are bringing this important data set within reach. Claims leaders can capture critical data in three ways:

Conduct self-assessments. Although this is the most basic approach, asking claims employees to self-assess their skills can be quite effective. Employees are used to providing information to help manage their professional development, and with analytics to steer focus on the skills that matter, companies can be more surgical about the amount of data they collect.

Would you like to learn more about our Financial Services Practice?

Employ document extraction. Using text analytics and natural-language processing, the data-science community has developed ways to extract skill information from résumés, job descriptions, performance reviews, and other sources.

Collect external data. With widespread use of professional-networking websites and increasing amounts of data on individuals, data aggregators can provide detailed employee profiles that companies can use to complement their internal data and provide a more comprehensive view of an individual’s work experiences. With employee consent, claims leaders can supplement their internal data using public information the employee has already shared on the web.

Like most data efforts, there are limitations, but starting and improving beats waiting and getting left behind. In a digital era in which the skills of claims employees will continuously evolve, having a granular view of skills will be a competitive advantage in getting the best people into the right roles. This approach has an added benefit: clearly knowing which groups of workers in the current organization are most likely to have the future skills needed will help guide the selection of external candidates if additional talent is needed.

Activate on-the-job learning to build needed skills

In addition to traditional methods, insurance leaders are starting to experiment with new ways to build skills in their workforce. Some companies are creating structures to help deploy employees into roles with higher demand that require skills of the future—particularly digital skills. One North American insurer established a talent accelerator, managed by a small hub team, that provided colleagues with targeted training to expand their skills and enable them to transition into new roles in different parts of the organization. As colleagues rotate through the accelerator, they spend significant time building skills toward a specific role of the future—for which past performance and an assessment suggested they have adjacent skills. Following that rotation, they are staffed onto project teams where they gain real work experience.

Launch a nimble reskilling and upskilling program

Across sectors, companies such as Amazon, AT&T, and JPMorgan Chase are already making massive investments in reskilling and upskilling, highlighting the strategic imperative of preparing workers alongside the digital transformation.1 The good news is that the size of these investments has increased the number of workers who are building future-ready skills on the job. Critically, claims organizations monitor the ways in which the skills employees need change over time as the adoption of automation progresses, and they must develop reskilling programs that are nimble enough to evolve ahead of the curve.

One important aspect of reskilling is building soft and socioemotional skills, which are of increasing importance for claims. Our research indicates that developing these skills—and continuously fine-tuning them—can be nuanced, and can involve deep changes in behavior. Similar to on-the-job learning for technical skills, some companies have implemented blended-learning journeys to develop soft skills that immerse employees in different points of view, such as those of customers, colleagues, and the employees themselves, showcasing in real time the desired behaviors for specific situations. Companies can also use reward mechanisms, such as skill certificates or badges, to mirror the recognition given to employees for more easily observed technical skills, such as digital fluency or data tagging.

Investing in reskilling can be both financially and culturally attractive. According to McKinsey analysis, the cost of releasing an existing employee and hiring a replacement is typically two to three times the cost of reskilling—without accounting for the time and challenge of onboarding new people. Moreover, engaging claims workers in building automation can reduce fears of technology and job loss and better prepare them for the future. A commitment to developing employees can build substantial goodwill for claims leaders.

The next ten years will be an exciting time for claims organizations. Leaders have a chance to reimagine their workforce, a chance to discover new ways of using technology and automation to improve the customer experience, and a chance to improve performance across the claims journey.

To capitalize on these opportunities, claims leaders must act now to develop a future-ready talent strategy. Doing so will help them better navigate the transition to a digital claims organization as well as help their existing workforce develop the skills they need to succeed.