Discussions of the labor outlook in Europe are understandably overshadowed by the impact of the novel coronavirus crisis. A discussion paper by the McKinsey Global Institute, The future of work in Europe (PDF–1MB) takes a longer-term view of the situation, to 2030.

Through a detailed analysis of 1,095 local labor markets across Europe, including 285 metropolitan areas, it examines profound trends that have been playing out on the continent in recent years and will continue to do so in the future. These include the growth of automation adoption, the increasing geographic concentration of employment, the shrinkage of labor supply, and the shifting mix of sectors and occupations. Some of these trends may be accelerated by the pandemic; our research suggests that a substantial number of the occupations that are likely to be displaced by automation in the longer term are also at risk from the coronavirus crisis in the short term. We also find that the effect of automation on the balance of jobs in Europe may not be as significant as is often believed.

TABLE OF CONTENTS

- Local labor markets across Europe before the pandemic experienced a decade of growth and divergence

- European jobs at risk from COVID-19 overlap with jobs vulnerable to automation

- As Europe’s labor force shrinks, automation will affect occupations and demographic groups unevenly

- The sector and occupational mix in Europe will continue to evolve

- Job growth could become even more geographically concentrated in the decade to come

- The choices European leaders make today will determine how the future of work unfolds

Local labor markets across Europe before the pandemic experienced a decade of growth and divergence

Total employment in the 27 European Union countries plus Switzerland and the United Kingdom rose by almost 10 percent between 2003 and 2018 to record highs. Our analysis of Europe’s regional labor markets suggests that the future of work has already begun unfolding. First, the occupational mix shifted. In all regions, the most highly skilled individuals enjoyed the strongest job growth over the last decade, while middle-skill workers had fewer opportunities. COVID-19 and increased automation adoption triggered by the pandemic may accelerate this trend. Second, employment growth has been concentrated in a handful of regions. Third, labor mobility before the crisis rose as the geography of employment shifted. In contrast to the United States, labor mobility in the EU has been rising as workers in the lower-income regions migrate to the dynamic cities to fill jobs.

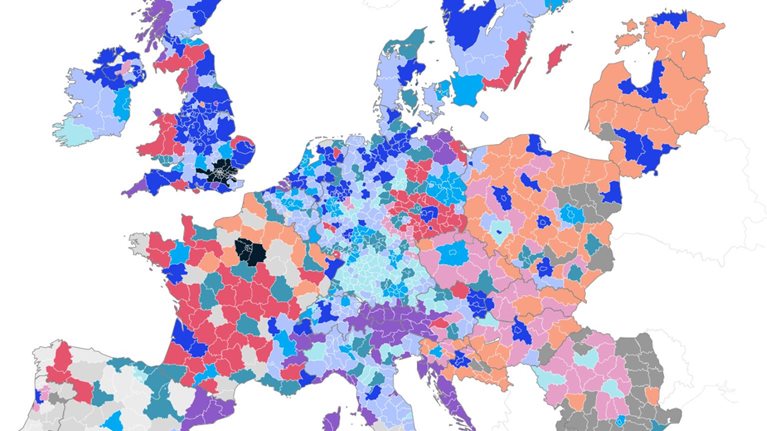

To understand the nuanced local dynamics at work and the likely impact of automation in the coming decade, we used a mathematical clustering technique to group 1,095 local labor markets across Europe into 13 clusters (Exhibit 1). These clusters fit into three sets: dynamic growth hubs, stable economies, and shrinking regions.

- Dynamic growth hubs are home to 20 percent of Europeans. This category includes two clusters with the highest GDP per capita in Europe and strong innovation capabilities. They are the megacities of London and Paris, with more than 10 million people apiece, and a young workforce with high educational attainment, and 46 superstar hubs, which have an array of high-growth industries and have been among the fastest-growing regions in Europe. They include Amsterdam, Copenhagen, Madrid, and Munich.

- Stable economies are home to 50 percent of Europeans. These clusters had above-average GDP per capita and attracted new residents. They include 102 service-based economies such as Budapest, Lyon, Manchester, and Riga, which have a high share of employment in nontechnical services such as wholesale and retail trade; 78 high-tech manufacturing centers, more than 70 percent of which are in Germany, including Stuttgart and Wolfsburg, which focus on manufacturing and produce a large number of high-tech patent applications; 64 diversified metros including Bologna, Freiburg, Plymouth, and Katowice, with a mix of industry and service employment; 267 diversified non-metro areas including East Kent, Korinthia, and Austria’s Mittelburgenland; and finally, 98 tourism havens, including Portugal’s Algarve region, Cornwall, and Mallorca. All of these areas have been hit by the travel restrictions imposed to stem the spread of COVID-19.

- Shrinking regions are home to 30 percent of Europeans. The working-age population in these clusters is shrinking because of outmigration, aging, or both. Three of these regional clusters are mainly in Eastern Europe: 72 industrial bases focusing on basic manufacturing; 85 educated and emigrating areas; and 58 agriculture-based regions. Other clusters in this grouping are 81 public sector–led regions, which have a high share of employment in the public sector, healthcare, and education; 35 trailing-opportunity regions, including Andalusia and Naples, which were facing high unemployment, negative net migration, and low business dynamism; and 107 aging-population regions including Dordogne, West Cumbria, and Zwickau, which have educated workforces but also high old-age dependency ratios.

Automation and other trends have already caused occupational and skill shifts across all local labor markets

Employment in Europe has grown in knowledge-intensive sectors such as telecommunications, financial services, real estate, and education, while it has been declining in manufacturing and agriculture. Job growth before the pandemic favored workers with the highest skill levels (such as legal and health professionals) across all three sets of local economy clusters. Likewise, job growth was also positive for occupations at the low end of the skills continuum, such as cashiers and sanitation workers. However, growth in lower middle-skill occupations (such as bank tellers) stagnated across all regional labor markets.

While new jobs were added, real wage growth stagnated for many Europeans. Between 2000 and 2018, average real wages grew by only 0.9 percent per year across Europe. The nature of work has been changing, too. Part-time work rose substantially in 22 of the 29 European countries. Until the COVID-19 crisis, independent work—including freelancers, workers for temporary staffing agencies, and gig economy workers—may have contributed 20 to 30 percent of all jobs.

Explore the future of work in Europe

See data for 1,095 local economies

Job growth since 2007 has been highly concentrated in 48 dynamic regions

Job growth has been highly concentrated in the 48 cities that constitute the dynamic growth hubs. These were home to 20 percent of the 2018 EU population and 21 percent of EU employment in 2018. Since 2007, they have generated a disproportionate 43 percent of the EU’s GDP growth, 35 percent of net job growth, and 40 percent of population growth, mainly by attracting workers from other regional clusters (Exhibit 2).

By contrast, stable economies were home to roughly half of the EU population (just over 250 million people) and EU employment in 2018 and accounted for a proportionate 53 percent share of EU job growth between 2007 and 2018. Shrinking regions, home to 30 percent of Europe’s population and 27 percent of EU employment in 2018, created only 12 percent of new jobs.

Behind the differences in employment outcomes are local differences in innovation capabilities, business dynamism, and available workforce skills. The 48 megacities and superstar hubs produce 55 percent of EU high-tech patents, versus 39 percent for stable economies and just 6 percent for shrinking regions. They account for 73 percent of startups, compared with 25 percent for stable economies and 2 percent in shrinking regions. Twenty-nine of these cities are home to almost 80 percent of the 126 European companies in the Fortune Global 500.

Moreover, the 48 growth hubs are home to about 83 percent of STEM graduates, and 40 percent of the resident population has tertiary education; this compares to less than 25 percent in some clusters within the shrinking regions category.

Labor mobility rose as talent moved to the jobs

As the geography of employment shifted across Europe, people looking for work moved. Most mobility has been domestic, but mobility across borders increased, by more than 50 percent, from 0.4 percent of the total population in 2003 to 0.6 percent in 2017. The number of working-age Europeans who live and work in another European country doubled from 2003 to 2018, from fewer than eight million (2.3 percent of the total working-age population) to 16 million (4.8 percent). Superstar hubs were the main magnets for new arrivals from 2011 to 2018, adding about two million people.

European jobs at risk from COVID-19 overlap with jobs vulnerable to automation

As the economy cautiously reopens after the shutdown, we have estimated that up to 59 million European jobs, or 26 percent of the total, are at risk in the short term through reductions in hours or pay, temporary furloughs, or permanent layoffs. The impact will be unevenly distributed, with significant differences among sectors and occupations and, as a consequence, among demographic groups and local labor markets.

Three occupational groups account for about half of all jobs at risk in Europe: customer service and sales, food services, and building occupations. The jobs most at risk from pandemic job losses overlap to some extent with those most vulnerable to displacement through automation. Around 24 million jobs, almost 50 percent of the number of jobs displaced through automation, are at risk of displacement though both COVID-19 and automation (Exhibit 3).

The overlap varies between sectors. For example, almost 70 percent of jobs that could be displaced due to automation in the wholesale and retail sectors are also at risk due to COVID-19 (Exhibit 4). A similar overlap may hold true of demographic groups most at risk, especially with respect to educational attainment. About 80 percent of jobs at risk (46 million) are held by people who do not have a tertiary degree, according to our estimates; overall, employees without a tertiary qualification are almost twice as likely as those with a university degree to have jobs at risk.

The employment impact of COVID-19 may hasten the workforce transitions to new jobs with different skills for many. The crisis could also accelerate existing inequalities within European countries, between better-educated and less well educated workers and regions, as well as among young people.

As Europe’s labor force shrinks, automation will affect occupations and demographic groups unevenly

In the aftermath of the 2008 financial crisis, unemployment rose sharply in Europe and only started to recover five years later, after a double-dip recession. Employment grew strongly in subsequent years until the 2020 health crisis. Assuming a similar long-term recovery after the pandemic, one key aspect of the employment story we find in our research relates to the supply of labor rather than demand for it among firms. While automation adoption will grow over the next decade, a shrinking labor force on the continent means that, by 2030, finding sufficient workers with the required skills to fill the jobs that exist and are being created in Europe may be challenging.

Europe’s declining labor force poses a potential challenge to employers over the next decade

Prior research by MGI estimated that about half of all work activities globally have the technical potential to be automated by adapting currently demonstrated technologies, with considerable differences by country. However, the pace and extent of automation will depend on the business case for adoption, wage levels, regulatory and consumer acceptance, technical capabilities, and other factors.

We ran multiple scenarios regarding the pace of automation in Europe prior to the pandemic. Under the midpoint scenario, about 22 percent of workforce activities across the EU (equivalent to 53 million jobs) could be automated by 2030—although this could be higher if the pandemic accelerates the pace of automation adoption. We assume that by 2030, the coronavirus crisis will be behind us and new jobs created would fully or partially compensate for this automation-related job loss. Even if there is a net decline in jobs, filling available positions would nonetheless be challenging for European employers. If the continent were able to recover only to pre-pandemic job numbers by 2030, employment rates would still have to increase by three percentage points in order to fill the likely jobs available. Even with a decline of 9.4 million jobs (about 4 percent respectively at an annual compound growth rate of –0.3 percent) from the pre-pandemic levels, employment rates would stay stable.

The shrinking labor pool is a key reason. Europe’s working-age population is expected to decrease by about 13.5 million, or 4 percent, by the decade’s end. The decline will be especially large in Germany (almost 8 percent, or about 4.0 million people), Italy (almost 7 percent, about 2.5 million people), and Poland (9 percent, about 2.3 million people). A shrinking workweek might add further pressure. Since 2000, the average hours worked each week per capita have decreased by more than one (or almost 3 percent), to 37.1 hours.

The sector and occupational mix in Europe will continue to evolve

Automation is not the only force shaping the workplace. Europe’s mix of sectors is rebalancing as manufacturing and agriculture continue to recede while services gain more relative weight. Now automation is amplifying the shift toward more knowledge-intensive sectors, such as education, information and communications technology, and human health and social work.

Based on our modeling, three sectors are likely to account for more than 70 percent of Europe’s potential job growth through 2030. The strongest net gains are in human health and social work, where 4.5 million jobs could be added. This is followed by professional, scientific, and technical services, which could add 2.6 million jobs, and education, which could gain 2.0 million jobs.

The occupational mix is also changing due to automation. Many of the largest occupational categories in Europe today have the highest potential for displacement. These include office support roles and production jobs, which employ about 30 million and 25 million workers, respectively. Low-wage customer service and sales roles, such as cashiers and clerks, are also likely to decline as many tasks are automated. Just ten of the more than 400 occupations we examined—including shop sales assistants, administrative secretaries, and stock clerks—account for nearly 20 percent of likely displacements (Exhibit 5).

Many of the growing occupations in our model require a higher level of skills. We estimate that STEM-related occupations and business and legal professional roles could grow by more than 20 percent in the coming decade. Creative and arts management roles could increase by more than 30 percent, although this is a small category, with just over five million workers. Just 15 occupations account for almost 30 percent of potential future net job growth in our model. They include such diverse occupations as software developers, nursing professionals, and marketing professionals.

Even within a given occupation, day-to-day work activities will change as machines take over some proportion of current tasks. Workers may need different skills as a result. Our model shows activities that require mainly physical and manual skills declining by 18 percent by 2030 across Europe, and those requiring basic cognitive skills declining by 28 percent. In contrast, activities that require technological skills will grow in all industries, creating even more demand for workers with STEM skills (increasing 39 percent), who are already in short supply. At the same time, we foresee 30 percent growth in demand for socioemotional skills. Human workers will increasingly concentrate in roles that require interaction, caregiving, teaching and training, and managing others—activities for which machines are not good substitutes.

In our analysis, education is significantly correlated with the likelihood of being displaced by automation. In the midpoint automation adoption scenario, people with only secondary education are three times as likely as people with more education to be in roles with high potential for automation.

Job growth could become even more geographically concentrated in the decade to come

Our findings suggest that automation and the occupational and skill shifts that accompany it would accelerate the concentration of potential net job growth, absent other changes. Unless COVID-19 causes changes in preferences of workers and companies for less dense communities, the same 48 megacities and superstar hubs that contributed 35 percent of the EU’s job growth in the past decade could capture more than 50 percent through 2030.

Our model suggests potential net growth rates of 15 percent in the two megacities and 9 percent for the superstar hubs in the midpoint automation scenario. Realizing this growth will require an influx of new workers and the right skills.

The clusters in the stable economies group could see modest job growth of less than 5 percent over the next decade. Our model shows them contributing about 40 percent of EU job growth through 2030—about ten percentage points below the share they produced between 2007 and 2018.

Within the shrinking regions category, few local labor markets are likely to see employment growth. Our analysis suggests that they will collectively account for less than 10 percent of expected EU job growth through 2030.

As a result of these trends, the share of Europeans living in regions where jobs are declining could double over the decade, to about 40 percent. One wild card in these estimates is the sudden shift to remote work that took place during the pandemic, as roughly one-third of the workforce began working from home. If this becomes a more permanent feature of working life, it could mean that some workers will not necessarily need to move to dynamic cities to take on the jobs being created there.

As automation adoption continues in the decade ahead, our scenarios suggest that almost all of today’s 235 million European workers will face at least some degree of change as their occupations evolve. Occupational and geographic mismatches are likely to emerge as a major challenge over the next decade (Exhibit 6).

Up to 21 million may have to leave declining occupations. We estimate that 94 million workers (about 40 percent of the 2018 workforce) may not need to switch occupations but will nevertheless have to acquire new skills because more than 20 percent of what they do today can be handled by technology.

In an analysis of online profiles we conducted with LinkedIn, we observe that workers typically move into new roles that are “adjacent” to their current ones (that is, they require overlapping or complementary skills). Individuals who enter growing occupations tend to move there from other growing occupations with very high skill adjacencies, whereas those in occupations that are declining because of automation tend to switch to other declining roles. For example, we found that 78 percent of people who moved into four highly sought-after occupations—software engineer, recruiter, talent acquisition specialist, and digital marketing specialist—came from other growing occupations. For four declining occupations we evaluated—food server, administrative assistant, salesperson, and accountant—we found that 57 percent of the observed transitions ended with individuals taking another job that is declining.

However, our research also identified several examples of promising pathways. Demand for shop sales assistants is declining. But with additional training, some of the 9.7 million workers in these roles pre-pandemic could draw on their overlapping experience in interacting with people to meet the growing demand for nurses or personal care assistants, for example.

Mobility could solve part of Europe’s job-matching challenge

The concentration of job growth heightens the importance of labor mobility. In megacities and superstar hubs, our estimates suggest that less than 60 percent of expected job growth can be filled by existing residents. Filling the remaining 2.5 million openings in these dynamic growth hubs will require millions more migrants (equivalent to 4.4 percent of the current population). Remote work—widely adopted during the pandemic—could account for at least some of these positions, alongside commuting and physical moves.

Filling low- to middle-skill occupations will be especially difficult in cities where the cost of living is highest. In Paris, for example, nursing associates (one of the fastest-growing occupations) have an average wage that is less than two-thirds of the average cost of living for a three-person household.

The choices European leaders make today will determine how the future of work unfolds

Each of the more than 1,000 local labor markets we analyzed will need to set its own priorities to address today’s issues and tomorrow’s eventualities. Here we highlight four issues common to many regions.

Europe needs to create more training and career pathways

Every country in Europe needs to ensure that its educational system is preparing students to succeed, with particular emphasis on the abilities required for in-demand jobs, such as STEM skills. Creating partnerships between educators and employers could help in the design of career-relevant curricula. Employers will be the natural providers of training opportunities for many, and policy makers can consider providing incentives to companies that invest in workforce development. But individuals who have to find new positions will need access to training programs outside their current workplace. Meeting the scale of this need will require mobilizing Europe’s existing educational system, networks of labor agencies, training infrastructure, and new digital technologies.

Access to jobs in dynamic growth hubs needs to be expanded

To fulfill their growth potential, Europe’s dynamic growth cities will need to keep attracting an influx of new workers at roughly the same rate as in the past. Investing in transit infrastructure around major metropolitan areas to expand what constitutes a viable commute is one way to increase mobility. Addressing the affordable housing shortage in these fast-growing urban areas would enable people who do want to move for better opportunities to do so. Geographic mobility alone may not solve this issue. If workers cannot move to the jobs, the jobs may need to move to them. With remote work on the rise, employers can also hire remote workers or turn to freelancers and outsourcing to expand their talent pool.

Shrinking labor markets need targeted economic development strategies

For policy makers, the prospect of even more polarized job, GDP, and population growth carries the risk of exacerbating social tensions and inequality. Many questions about industrial policy, skills development, urban development, and mobility will need to be debated, and some involve difficult trade-offs. Policy makers will need to decide whether and how to invest public money or attract private funds into areas in relative decline to revitalize their economies. EU programs such as Horizon 2020 and the Cohesion Policy can be sources of funding and collaboration. A common strategy pursued by local governments is providing economic incentives to entice companies to relocate. Subsidies may be part of the tool kit, but they need to respect competition policy, be backed by a rigorous business case, and advance a more holistic economic development plan. Regions that are losing workers may have to boost investment in local educational institutions or provide financial incentives to attract skilled outsiders.

Europe needs to keep raising labor-market participation

Once the economy recovers from the COVID-19 crisis, it may be necessary to raise labor participation to deal with the decreasing working-age population. To boost employment rates, national governments may have to consider broad labor-market and pension reforms. One logical place to start is getting more willing workers off the sidelines, focusing on demographic groups where there is room for growth, including workers over age 55 and women. The female labor force participation remains significantly below that of men, in part because women in Western Europe still do two-thirds of all unpaid care work. Employers can attract and retain women by offering more flexible schedules, part-time work, and remote-work options. Governments can also provide tax incentives for second earners in a family and ensure that public childcare and eldercare programs are widely available.

Governments and companies need to focus on long-term labor market trends as they prepare for the post-pandemic era. With accelerated automation adoption, demographics could work in Europe’s favor. Helping individuals connect with new opportunities and prepare for the jobs of tomorrow will challenge every community across the continent.

Related Articles

Explore the future of work in Europe