In this episode of the Inside the Strategy Room podcast, McKinsey senior partners Chris Bradley, Martin Hirt, and Sven Smit speak with communications director Sean Brown about their book, Strategy Beyond the Hockey Stick. In this first of three podcasts, the co-authors discuss the power curve of economic profit and how this empirical analysis can help companies calibrate their performance aspirations and cut through the social dynamics that produce inertia. This is an edited transcript. You can listen to the episode on Apple Podcasts, Spotify, or Google Podcasts.

Podcast transcript

Sean Brown: Welcome to Inside the Strategy Room. Today we’re going to talk about something almost every company struggles with at some point: translating bold ambitions into strategies that truly improve performance. With me are McKinsey senior partners Chris Bradley, Martin Hirt, and Sven Smit. They recently wrote a book that brings big data analytics to the world of strategy: Strategy Beyond the Hockey Stick: People, Probabilities, and Big Moves to Beat the Odds.

Martin is a senior partner based in Greater China and the global co-leader of the Strategy and Corporate Finance practice. Sven is a senior partner based in the Amsterdam office and the former global leader of the practice. And Chris is a senior partner and leader in the practice based in Sydney. Gentlemen, welcome.

So, my first question is, why this topic? And why did you choose to write about it now? Sven, perhaps you could start us off.

Sven Smit: The first point I want to make is strategy is back. The times are uncertain, volatility is high, and we see that the intensity of conversation around strategy in the context of global forces is very high. Second, this is ten years after a major round of big data on strategy. There is just more data available, so we wanted to see whether new insights came out.

Martin Hirt: We got involved in a lot of advanced-analytics and artificial-intelligence topics around 2011 and 2012, and we started asking ourselves, why is it that the field of strategy seems to be the only management faculty that’s reasonably immune from big data analytics? We felt there was no real answer for this other than nobody had actually done it, so we decided to do it. And we were determined to move away from strategists’ traditional recipe, which is to put out a framework, then pull together a list of case studies of brand-name companies to “prove” that the framework is the right way to think about a strategy.

Subscribe to the Inside the Strategy Room podcast

Instead, we wanted to use empirical data to figure out what is really working and what’s not working in strategy. The starting point for us was to ask ourselves, how do you actually measure the success of a strategy? Is there a common denominator we could use that addresses at least one of the objectives that companies are pursuing?

The fundamental idea was that, just as with many other aspects of our lives and businesses, strategy is not guesswork but a matter of probability. As long as you have data, you can understand the probabilities of strategy success or failure as well. With the right amount of data—in our case, the complete financials and strategies over the past 25 years for about 2,500 of the largest companies in the world—you can start drawing pretty sound empirical conclusions.

Sean Brown: Thanks, Martin. One of the other big ideas in the book is what you call the social side of strategy. Chris, can you describe what that means and how it affects strategic planning?

Chris Bradley: Well, the process is broken, and it’s broken for very human reasons. We are learning more and more about how to get under the skin of those human reasons through research on bias and agency costs. You see, strategy decisions are irregular, long-term decisions made under a lot of uncertainty, which is exactly the opposite of what our brains were designed to do. For example, the average person is exceptionally good at driving a car, and that’s because you do it every day and you get instant feedback. Strategy, not so much. Even the most seasoned executives might have done at best four or five big strategic changes over their careers. That’s not much practice.

So, the first problem is, you have people. They are biased. They have limitations. They’re overconfident. They anchor. But then you add other people, too. And then you are in the whole world of social dynamics where you have even unintentional competition, information asymmetry, and misaligned incentives. When you put all that together, you get this complex soup.

How do you measure the success of a strategy? We wanted to use empirical data to figure out what is really working and what’s not working in strategy.

The outcome is inertia, as the norm. The social side of strategy is very, very good at keeping companies stuck where they are. And that’s why we are so interested to understand it really well: so we can resolve the inertia that stops executives from making the big moves that our evidence shows they really need to make.

Sean Brown: Sven, what kind of social dynamics do you find to be the biggest challenges?

Sven Smit: The book is called Strategy Beyond the Hockey Stick because the basic process of strategy sausage-making is a proposal process called strategic planning, where people promise a bright, hockey stick–shaped uptick in the future if they can get the money now. And their entire game is, through promises, to get some form of resource allocation. As a result, they play every single game in the book to get what they need: the pros of their argument are big, the cons are small; the strengths are big, the weaknesses are small; the competition is absent; and you are the leader. And what do you do if somebody asks a question challenging this reasoning? Your typical answer is, “That’s a great question. We have the answer on page 42 of the deck.” Because what you really do not want is to create a discussion.

Would you like to learn more about our Strategy & Corporate Finance Practice?

I always jokingly compare strategic plans with marriage proposals. In a marriage proposal, somebody promises a bright future, but nobody talks about the real-world data, which suggests a marriage has about a 50 percent chance of lasting 12 years. That kind of data is what strategy proposals should also have, because they are full of probabilities. But the social dynamic of pride—standing out to your colleagues, getting the resources you want—prevents people from internalizing the data. And that tension is the genesis of this book: the tension between the real data of what makes good strategy and the games that are being played in the strategy room.

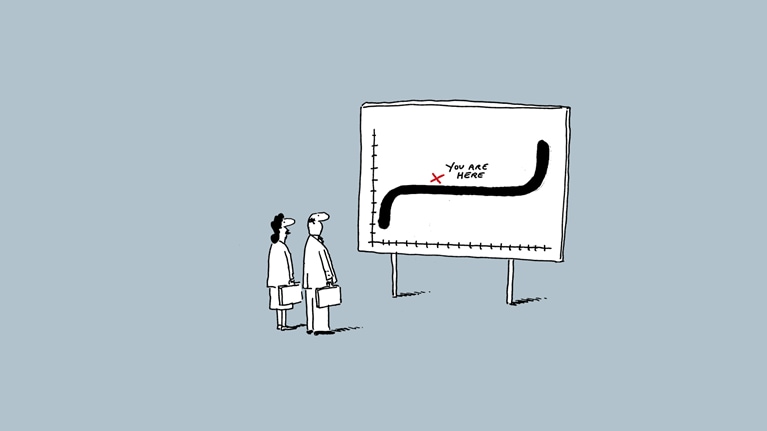

Sean Brown: Chris, in the book there’s a passage colorfully titled “Hockey stick dreams and hairy-back realities.” Tell us what that means and what leads to that unattractive reality.

Chris Bradley: The ugliest but, unfortunately, one of the most common charts in strategy is what we call the hairy back, which is what it looks like when a bunch of unsuccessful hockey-stick strategies pile up on each other. Each year you see the hockey-stick forecast and then the reality, and then the next year’s hockey stick forecast and the reality. And it looks remarkably like a hairy back.

Now, why does this happen? It’s because of two competing biases. The first one is overconfidence about our baseline. And the second is timidity. We have this boldness in our forecasting but timidity in making plans, because making big, bold plans is difficult. You are moving a lot of people’s cheese, if you know what I mean. So, if you have a hockey stick that is based on a bold forecast and a timid plan, you will end up with a hairy back.

What we say instead is, “No, no, no. Have a really clear-eyed forecast. Understand your momentum case. Know what the forces at work are. Understand how much the context shaped your performance. And then, make a plan that is calibrated to the reality of your context and of the performance you want.” By highlighting the social side of strategy, we are saying that it is not about the quality of the analysis or how many pages were in the deck—it’s about changing the frame of the conversation.

Sean Brown: Can you share some examples?

Chris Bradley: Well, as soon as you start discussing where to compete, you are talking about movement and change. People like being good in their niche. They are comfortable doing what they’re doing. Not only that but resources are normally locked into the status quo. It’s not hard to imagine why. Our research has found that the correlation between the capital budget from one year to the next is 90 percent. In other words, the people who have the capital get the capital. So, if strategy is about decisions where to compete but the actual experience of companies is inertia, that keeps them stuck where they are. That’s where the social side of strategy plays an important role.

People’s entire game is, through promises, to get some form of resource allocation. As a result, they play every single game in the book to get what they need.

One way we cast this is to think about it like a negotiation of targets. You have this fiendish trade-off, because on the one hand you want to garner resources and appear bold and visionary by having a high target, and on the other hand you want a low target because you want achievability. You want to have a good scorecard at the end. You want to achieve your bonus-able targets, and frankly, it’s going to be easier with a low target. That’s the perspective from the proposer’s view.

From the person getting the strategy pitched to them, it’s also fiendishly difficult because you are concerned that the proposer is sandbagging. You yourself want to make sure you are motivating the highest possible performance but also that it’s realistic.

Sean Brown: Martin, earlier you talked about the notion of frameworks versus hard data and the importance of data in formulating successful strategy. What was the breakthrough idea in terms of applying these empirics?

Martin Hirt: Well, we wanted to first understand where economic profit is in the world, how it is distributed. We chose economic profit because it combines two factors that we know drive shareholder value: growth, represented by invested capital, and the return on that invested capital. Also, economic profit is reasonably under the control of management. It represents the increase in economic value as evidence for the company improving relative to other companies in the market, and therefore as evidence of a good strategy.

We looked at the largest companies in the world and determined their average economic profit over a five-year period and did that over different time increments. That gave us a distribution of economic profit in the world. And we found that this distribution followed a strong power law, meaning it’s very uneven. The top 20 percent of companies—the top quintile—accumulate more than 90 percent of the economic profit. The three middle quintiles, or 60 percent of the companies we looked at, are hovering largely around the zero line. The economic profit distribution has the shape of very steep bookends and a broad, flat middle around the zero.

These findings provided a few very interesting insights. One was that in order to get into the zone of participating in substantial economic value creation, a company has to get into the top quintile. And the other one is that 60 percent of all companies are working incredibly hard just to keep up with a rising water level.

Chris Bradley: If we go back a little bit further, around 2009 and 2010, we developed this framework called the ten timeless tests of strategy. Instead of saying, what is the best way to develop the next thing in strategy? we asked ourselves a question we thought was relevant to more executives: I’m getting bombarded with strategies—how do I tell the good ones from the bad?

Now, the first big test of strategy is: Does your strategy beat the market? And by that, what we really mean is, did you generate economic profit, which is the evidence that you overcame perfect markets? Because—and perhaps this is a scary flashback to your economics textbooks—in perfect markets there is no economic profit. The residual of market imperfections, or what we call competitive advantages, is economic profit.

If that’s the test of strategy, how many companies are actually winning? And we kind of stumbled onto this power curve, which is one of the central empirical concepts of the book. It shows that when you do look at economic profit, you see that actually markets work really well about 60 percent of the time in keeping economic profits remarkably close to zero.

So, we were armed with the best thing you can have if you are trying to come up with a new idea, which is an interesting new question: “What does it take to go from that middle three quintiles, where economic profit is basically zero, up into the top quintile where there are massive economic profits? And how often does it happen?”

Sean Brown: Did you look at how the power curve of economic profit has evolved over time? In other words, has it gotten steeper at the bookends? Closer to zero in the flat middle?

Martin Hirt: There are two moves we detect over time. The first one is that the absolute amount of economic profit generated by these companies has increased over the 25 years that we studied. Obviously, the absolute level of economic profit achieved is slightly cycle-dependent. So, between 2007 and 2010, there was a dip in the absolute levels of economic profit achieved by companies around the world, but over 25 years the absolute amount has increased.

The other is that the curve has gotten steeper. Economic profit has accrued more disproportionately to the very successful at-scale players—and in recent years in particular, to platform players. Today, five out of the top ten listed companies in the US by market cap are platform players.

Sean Brown: You say you looked at corporate performance during different time periods. What kind of mobility did find among the companies you studied? Did many manage to rise on the power curve?

Martin Hirt: One aspect in this context that is actually very important to consider is how hard it is to move up on the power curve. Moving from the three middle quintiles to the top quintile over a ten-year period has a less than 10 percent chance of success. So, fewer than one in ten companies makes it.

That analysis also holds true on a business-unit level, meaning that typically, in a portfolio of businesses a company has, only one in ten business units will move. Now, the interesting result that our later analysis delivered was that, when you look at companies that move from the middle to the top—those that truly have hockey stick performances—there, typically exactly one business unit moved. It’s not that they got all businesses to perform better. It’s not that they peanut-buttered their resources across everything and just hoped for the best. No: they concentrated their investments on one business, or very few businesses if they were not 100 percent sure, and then, in 90 percent of all cases, just one business really moved and that lifted the whole company.

Sean Brown: Sven, the book has been out for a little while now and you have been sharing the ideas in it with clients. Can you tell our listeners some of the most surprising reactions that you’ve gotten?

Sven Smit: We sometimes get the surprised reaction that McKinsey can be funny, because the book has funny cartoons. But the second thing is, people say, “We love your analytics. They are really insightful and they make a huge difference. Maybe you have found something that is kind of a benchmark approach to calibrating whether moves are big enough.”

Have a really clear-eyed forecast. Understand your momentum case. And then, make a plan that is calibrated to the reality of your context and the performance you want.

Also, people like that we address the social games, because that is the world they live in. Even if they have the answer analytically, they need to navigate this social game all the time, and that we might have a few ideas on how to navigate the social game differently really gets the eyes blinking.

Sean Brown: Last question, for Chris. Where are you going next with the research?

Chris Bradley: The next step for us is to work out what an agile company looks like when it comes to strategy, in terms of fluidity of resources, in terms of pursuing shared goals, and in terms of making enterprise-consistent risk trade-offs. We think technology is going be part of the solution, by the way, as with any kind of big change in management processes, and we are developing our first digital platform to figure out how to do strategic planning and bring some of these ideas together.

Strategy Beyond the Hockey Stick: People, Probabilities, and Big Moves to Beat the Odds

Sean Brown: Thanks for joining us today.

During our next Inside the Strategy Room podcast, we will continue our conversation with Chris, Martin, and Sven. They will share the factors that their research revealed to have the biggest impact on boosting corporate performance, and how big a strategic move needs to be to move a company up the power curve.

Related Articles

Strategy to beat the odds