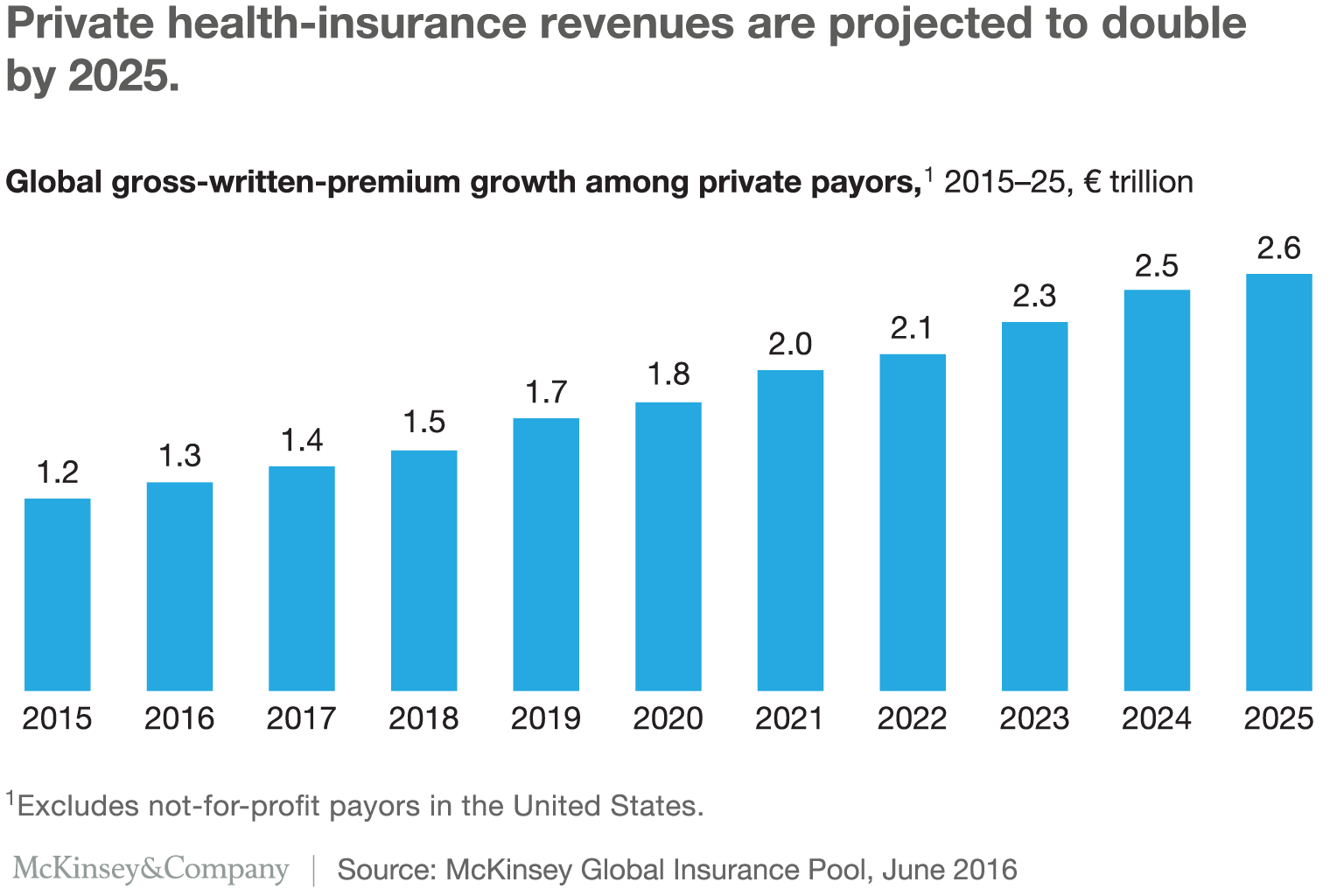

Revenues in the global market for private health insurance—already €1.3 trillion—are expected to double by 2025 (Exhibit 1). The demand for healthcare services, and hence health insurance, is increasing because of population aging and the growing prevalence of chronic disease, as well as rising incomes in the developing world. At the same time, pressure on public finances is prompting many governments to impose healthcare-spending cuts or seek out private payors as intermediaries to better manage spending and outcomes. Capturing the opportunity requires understanding and responding to four fundamental forces that are disrupting the private health-insurance market.

The four forces

Four fundamental forces with the power to reshape the industry’s structure and performance—risk, technological innovation, consumerism, and regulation—are in play. As we make clear in the longer report from which this article is drawn, Global private payors: A trillion-euro growth industry, all four of these forces are currently disrupting the private health-insurance industry.

Stay current on your favorite topics

For example, the nature of the medical risks covered by health insurance has changed in wealthy countries and, increasingly, in many developing countries. Today, a high proportion of expenditures are for chronic conditions, not random, unpredictable, catastrophic events (for example, accidents and infectious diseases), which has made insurance in its traditional sense obsolete. The rapid progress being made in digitization and advanced analytics is making it possible for payors to implement innovative payment models and customize care delivery for many patients. Greater information transparency and rising out-of-pocket costs are prompting many consumers to take a more active role in determining the health services they receive.

Would you like to learn more about our Healthcare Systems & Services Practice?

Regulatory reforms are playing out in different ways in different countries. In the Netherlands and United States, for example, regulatory changes have upended previously stable health-insurance markets. Liberalization is opening up opportunities in countries in Eastern Europe and Latin America. In countries in Asia, the Middle East, and North Africa, government initiatives are offering incentives to private payors to help reduce overall healthcare spending while improving access to care.

Capturing the opportunity

The size of the opportunity is likely to attract new entrants. Thus, an incumbent payor that wants to survive the disruption and capitalize on market growth should answer three questions.

The first concerns where to play—which geographies and business segments should it focus on? There is no single right answer. We anticipate market growth in most regions (Exhibit 2), but our projections suggest that the countries likely to have the highest growth in gross written premiums are not necessarily those with the highest potential for future profitability. Each payor must therefore base its decision on a deep understanding of each potential market, including its population, disease burden, provider landscape, funding mechanisms, and regulatory environment, as well as its own competencies.

The second question addresses how to play—which business model is required to win? A range of options—from indemnity insurance to comprehensive managed care, and many other options in between—can be considered, each of which has implications for acquisitions, partnerships, and investments. When answering this question, the payor should keep its focus on the future. Given the industry’s disruption, the business models needed in a few years’ time could be quite different than those that worked in the past, and thus the payor will need to be able to innovate its model rapidly and often.

How to tame rising US healthcare costs

The third question focuses on how the global portfolio should be governed—how should the company be organized to go after the opportunities? The mix of markets and business models a private payor chooses should directly inform the governance model used to pursue growth, margins, and sustainability. Careful balance is needed, though, to ensure that the company can maintain sufficient dexterity to respond to local conditions without losing sight of synergies (particularly in new competencies, such as analytics, digital, consumer engagement, and care management) that could benefit the organization in multiple regions.

For both incumbents and new entrants, the global private health-insurance industry offers attractive long-term growth potential. Success is likely to go to those with a deep understanding of the forces buffeting the industry, a strong strategy, and the ability to innovate rapidly.