The specter of deleveraging has been haunting the global economy since the credit crunch reached crisis proportions in 2008. The fear: an unwinding of unsustainable debt burdens will drag down growth rates for years to come. So far, reality has been more benign, with economic growth recovering sooner than expected in some countries, even though the financial sector is still cleaning up its balance sheets and consumer demand remains weak.

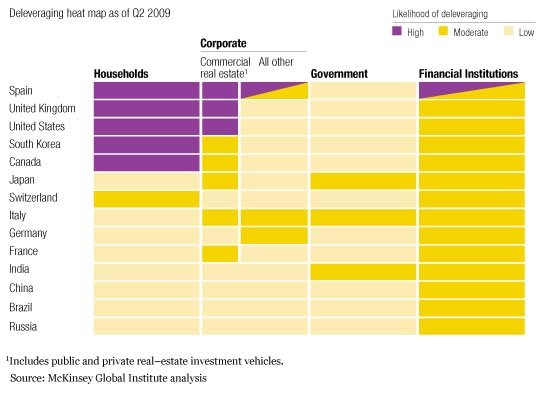

New research from the McKinsey Global Institute (MGI), though, suggests that the deleveraging process may just be getting under way and is likely to exert a significant drag on GDP growth.1 Our study of debt and leverage2 in ten mature and four emerging economies3 indicates that some sectors of the economies of five countries—Canada, South Korea, Spain, the United Kingdom, and the United States—will very probably experience deleveraging.

What’s more, our analysis of deleveraging episodes since 1930 shows that virtually every major financial crisis after World War II was followed by a prolonged period in which the ratio of total debt to GDP declined significantly. The one exception was Japan, whose bursting asset bubbles in the early 1990s touched off a financial crisis followed by many years when rising government debt offset deleveraging by the private sector. The “lost decade” of sluggish GDP growth that followed is a cautionary tale for policy makers hoping to somehow avoid the painful process of deleveraging.

Business executives too will face challenges: they may have to adapt to an environment in which credit is tighter and costlier and consumer spending could be slower than trend over the medium term in countries where household debt has built up. Our findings underscore the likelihood that growth will be stronger in emerging markets, which are far less leveraged, than in mature ones. To cope, companies should build the potential impact of “pockets” of deleveraging into their market outlooks.

Where deleveraging is likely today

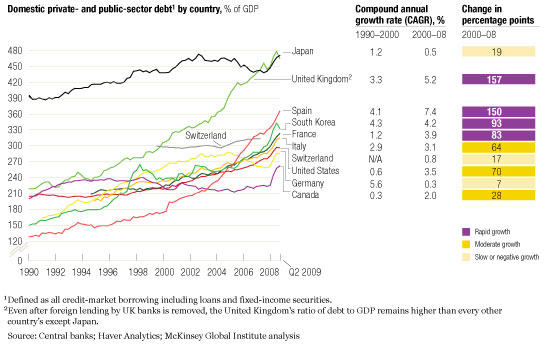

Debt grew rapidly after 2000 in most mature economies. Although the United States is often assumed to be the most profligate borrower, by 2008 several countries—including France, South Korea, Spain, and the United Kingdom—had higher levels of debt as a percentage of GDP (Exhibit 1). Of course, such aggregate measures of leverage are not by themselves a reliable guide to the sustainability of debt. Swiss households, for example, have sustainably managed very high levels of leverage for a long time because they possess high levels of financial assets that can be drawn on to repay debt and because Swiss banks have conservative lending requirements.

Growing debt

So to gauge the likelihood of a deleveraging, we took a more granular view, studying how debt and leverage have grown over time in individual sectors of 14 major economies. We assessed the sustainability of debt by considering factors such as the level and recent growth of leverage and the borrowers’ debt service capacity and vulnerability to income and interest rate shocks.

Our analysis suggests that ten sectors have a high likelihood of deleveraging (Exhibit 2). In eight of the ten, very high levels of debt are linked to real-estate booms: the household sectors of Spain, the United States, and, to a lesser extent, of Canada and South Korea, as well as the commercial-real-estate sectors of Spain, the United Kingdom, and the United States. The remaining two are parts of Spain’s financial and non-real-estate corporate sectors.4

Getting out of debt

Overall, the corporate sectors in most countries entered the crisis with lower levels of leverage than they had at the start of the decade, with the exceptions of the commercial-real-estate subsector and companies acquired through leveraged buyouts. Both of those pockets of leverage have over $1 trillion of debt, which will need to be refinanced in coming years, suggesting difficulties ahead.

What history teaches about deleveraging

To understand what deleveraging might look like going forward, we analyzed 45 significant, historical deleveraging episodes: those in which the ratio of total debt to GDP declined for at least three consecutive years and fell by 10 percent or more. The deleveraging episodes ranged from the US Great Depression (1929–43) to Argentina’s current troubles (2000–present).

In 32 of the episodes, the deleveraging process commenced after a financial crisis and followed one of four paths. Three typically occur under economic conditions that are not currently present, so they are unlikely now: high inflation, which causes deleveraging by increasing nominal GDP growth; massive default, which typically follows currency crises; and rapid economic expansion fueled by war or oil booms. The fourth—a prolonged period of austerity, or “belt tightening”—is not only the most common path, fitting 16 of the 32 deleveraging episodes that took place after a financial crisis, but also the one that seems most relevant today.

Deleveraging through belt tightening—exemplified by the US economy during the Depression years from 1934 to 1938 and by South Korea and Malaysia after the Asian financial crisis in 1997—is usually a long and difficult process that reduces the ratio of debt to GDP by about 25 percent. Credit growth in most cases slowed dramatically: in the mature economies in our sample, it averaged 17 percent annually in the ten years prior to the crisis but fell to just 4 percent during deleveraging. Real GDP typically declined in the first two to three years of deleveraging but then rebounded and grew strongly for the next four to five years while deleveraging continued (Exhibit 3).

A slow start

This time could be different

While the historical record is helpful, several elements of today’s environment suggest that deleveraging may start later and take longer. First, aging populations in much of the world are causing labor force participation rates to fall, which will make it more difficult than usual to jump-start and sustain GDP growth. Another complication is that the financial crisis of 2008 was global in scale, affecting the world’s biggest economies—not just one or a few, as in most previous crises. Therefore, it would be very difficult for all of today’s affected countries to boost net exports simultaneously, as many did in the past to support GDP expansion when credit growth was slowing and households were saving more.

Add to that problem the prospect of sharply increasing government debt relative to GDP in several major economies. According to Global Insight, US government debt will grow to 105 percent of GDP by 2012, from 60 percent in 2008; UK government debt to 91 percent, from 52 percent; and Spanish government debt to 74 percent, from 47 percent. This development could more than offset any deleveraging by the private sector. One implication is that Spain, the United Kingdom, and the United States might postpone deleveraging until after the crisis passes and growth in government debt has been reined in. It’s also likely that debt-to-GDP ratios will decline more slowly and over a longer period than the historical average, creating severe headwinds on economic growth, though we do not forecast GDP.

How policy makers and business leaders can respond

Policy makers today face an acute challenge going forward. On the one hand, public policies that stimulate GDP growth will be invaluable for countries experiencing deleveraging, because such policies help an economy “grow into” its current level of debt rather than pay it off. Households and businesses can therefore save more without reducing consumption and investment as sharply as they would otherwise have to do. On the other hand, faced with rising public debt, policy makers must also carefully consider when to reduce government support of aggregate demand. Japan’s experience in 1997 highlights the danger of winding down stimulus programs prematurely, potentially stifling a recovery. But it also illustrates the dangers of letting public debt grow unchecked. Getting the timing right will be critical.

Regulators are now discussing ways to improve the stability of the financial system. Our analysis strongly suggests the need for monitoring leverage at a very granular level in the real economy, since overleveraged borrowers in a few sectors were at the heart of the crisis. The data, which could then inform the banks’ risk models and regulatory policies on bank capital, should be compiled at an international level, given the growth in cross-border lending and the insights that can be gleaned from cross-country comparisons. Our analysis also provides support, in principle, for a more active approach to monitoring systemic risk in the financial system.5 We suggest caution about moves to raise bank capital ratios too quickly and too high, however, given the risk of exacerbating the pressures facing major economies as they deleverage.

Corporate executives, meanwhile, must learn to manage under continuing uncertainty. Business models that rely on low-cost debt will not be economically feasible, but companies with capital will find ample opportunities to expand market share or make new acquisitions. Consumer-facing businesses have already seen a shift in spending toward value-oriented goods, and this new pattern may persist until households repair their balance sheets. Scenario planning will be of the essence. We encourage business leaders to develop a range of scenarios that reflect different degrees and speeds of deleveraging rather than predicate strategies on a single view of what might unfold.

As of this writing, the deleveraging process has barely begun. Each week brings news of another country or company straining under the burden of too much debt. Deleveraging is likely to be a significant component of the post-crisis recovery, and this will dampen growth. Nevertheless, by learning lessons from past experiences of deleveraging, today’s policy makers and business leaders may be better placed to steer a course through these challenging waters.