Two forces that until recently turbo-charged US consumer spending—growing household debt and a falling savings rate—have gone into reverse. In late 2008, as households started reducing their indebtedness and saving more, consumption tumbled.

New research from the McKinsey Global Institute shows that the economic impact of further US consumer deleveraging will depend on income growth. Without it, each percentage point increase in the savings rate would reduce spending by more than $100 billion—a serious drag on any recovery. Relatively healthy income growth, on the other hand, would help households reduce their debt burden without trimming consumption as much.

The significance of any fall in consumption could be profound. US consumers have accounted for more than three-quarters of US GDP growth since 2000 and for more than one-third of global growth in private consumption since 1990. These trends were fueled by a surge in household debt,1 particularly after 2000 (Exhibit 1), and a decline in the personal savings rate—to a low of –0.7 percent, in 2005. From 2000 to 2007, US household debt grew as much, relative to income, as it had during the previous 25 years.

Household debt soars

Appreciating household assets—the “wealth effect”—enabled consumers to spend and borrow more even as they saved less. The value of US household assets rose by some $27 trillion from 2000 through 2007. Rising home values, as well as stocks and other financial assets, accounted for more than two-thirds of this gain.

This dynamic sputtered to a halt when the housing bubble burst and the financial and economic crisis ensued. Falling values for homes, stocks, and other assets have battered US households: from mid-2007 through the end of 2008, their net worth fell by roughly $13 trillion. These recent losses erased all the gains in net worth, relative to disposable income, since the early 1990s (Exhibit 2). It’s not surprising that US consumer spending fell at a 4.3 percent annual rate in the fourth quarter of 2008—a major reason for the broader economic contraction.

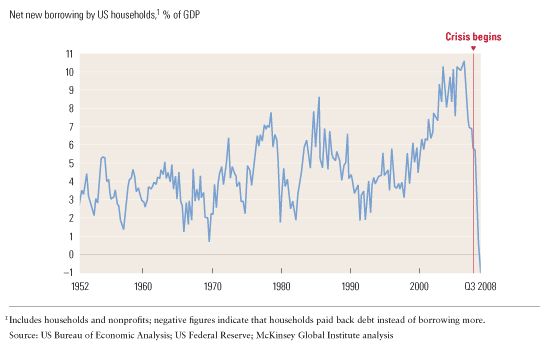

Paradise lost

The flip side of falling consumption is a rising personal savings rate, which reached 3.2 percent in the fourth quarter of 2008. Net new borrowing by households also has fallen sharply from its 2006 peak. In the fourth quarter of 2008, it turned negative for the first time since World War II (Exhibit 3).

Fallen borrowing

Several forces underlie these shifts. Some households are responding to worries about possible unemployment or underwater mortgages by paying down debt or avoiding new debt. Others have found their credit lines shut down or can’t get new credit, because banks have tightened their lending standards.

How far these trends will go is a critical economic uncertainty in the months ahead. The economic impact of today’s deleveraging will depend on how it unfolds—through income growth, higher savings, or some combination of the two.

If incomes stagnated, for example, households could deleverage only by saving more. Every percentage point reduction in the debt-to-income ratio would require nearly a one percentage point increase in the savings rate. The US personal savings rate reached 5 percent in January, 2009. If this level prevailed and incomes didn’t grow, this would reduce the household debt-to-income ratio by five percentage points—which still wouldn’t be enough to restore the levels of indebtedness prevailing in 2000, before borrowing started to accelerate.

But if incomes rose, households could both reduce their debt burden significantly over time and continue to consume. If US incomes grew by 2 percent a year, for instance, households could reduce their debt-to-income ratio by as much as they would in the scenario above—but with a personal savings rate of only 2.3 percent.

These different scenarios have serious implications for the US and global economies because, holding incomes constant, each percentage point increase in the savings rate translates into roughly $100 billion less in consumer spending¬. A 5 percent savings rate would mean $530 billion less in spending each year if US incomes fail to rise; if they rose by 2 percent a year, a 2.3 percent savings rate would mean $250 billion less spending, all else being equal.

In short, the importance of income growth is difficult to overstate. With it, households can simultaneously reduce their debt burden, rebuild savings, and boost consumption. But without significant income gains, deleveraging could undermine consumption and the global economy for years to come. One implication: policy choices that favor productivity and employment growth—critical determinants of income growth—will make deleveraging less painful. Efficiency breakthroughs in sectors, such as health care and government, that employ large numbers of people—but that have not enjoyed productivity revolutions similar to those experienced in industries like retailing and wholesaling—would make a dramatic difference.