As a tumultuous year draws to a close, executives are moderately hopeful about their nations’ economies and their companies’ prospects, according to a survey in the field during the second week of December.1 Just over half of executives continue to say economic conditions are now better than they were in September 2008, and for the first time this year a majority expect customer demand for their companies’ products or services to rise in the near term. In addition, notably more are seeking—and getting—external funding than have done so in more than a year. And after reporting a striking shift in favor of short-term planning early in 2009, executives say their companies are once again able to plan for the medium and long term—but also that they remain wary, assessing more options and checking progress more frequently than they did before the crisis.

This survey also included some questions on currency volatility and reserve currencies. Nearly a third say that exchange rates today have an “extremely” or “very significant” effect on their profits. Further, executives expect greater future volatility in exchange rates as well as significant changes to global exchange rate arrangements in the coming years—only 18 percent expect that the US dollar will still be the dominant reserve currency in 2025.2

Moderated hope

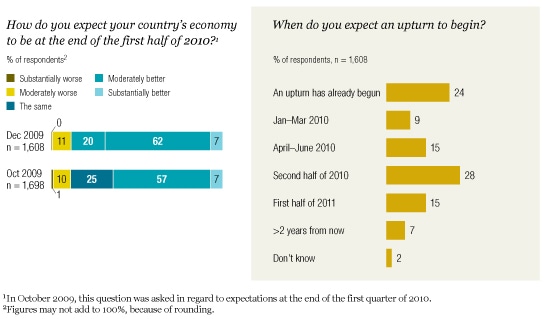

The share of executives with largely positive views on their nations’ economies has continued to grow slightly over the past six weeks: just over half say economic conditions are better than they were in September 2008 and nearly 70 percent say they expect economic conditions to be better still at the end of the first half of 2010 (Exhibit 1). Further, for the first time, more than half of all executives (57 percent) expect their countries’ 2009 GDP to increase—a jump of 8 percentage points in six weeks, perhaps reflecting a view that the end of the year is now close enough for them to express some certainty.

Respondents are also moderately hopeful about their companies’ prospects. For the first time this year, more than half (54 percent) expect customer demand to increase in the near term, compared with 39 percent in April 2009.3 However, the share expecting a profit increase—46 percent—is almost identical to those who expressed a similar view six weeks ago, indicating that executives see continued pressure on pricing and costs. Indeed, cost control remains the single most frequently chosen action that companies plan to take over the next 12 months to cope with changing economic conditions, with 65 percent saying they expect to undertake it.

Expectations for the workforce remain stable, and just over a quarter of respondents expect an increase in the near term. Expectations for additional decreases are likeliest among respondents at companies headquartered in the eurozone (39 percent) and those in manufacturing (34 percent).

A brighter near-term outlook

More robust funding and planning

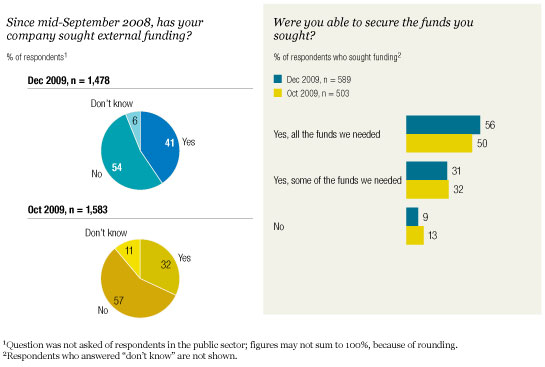

For the first time in more than a year, the share of respondents saying their companies have sought external funds has changed significantly, increasing to 41 percent in this survey, from 32 percent in October—a figure consistent with findings over the past year. Further, more were able to get the funds they sought (Exhibit 2). These findings may indicate a rising, and apparently well-founded, hope among executives that funds will be available to them.

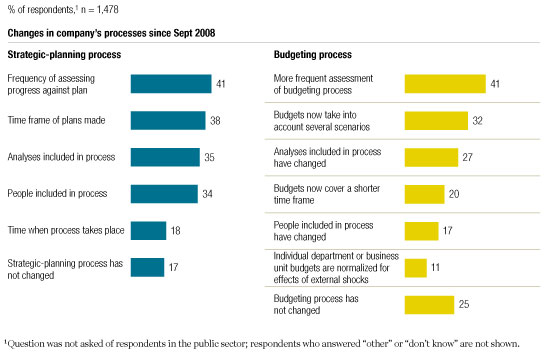

Most companies have made several changes to their strategic-planning and budgeting processes since September 2008. Taken together, these findings indicate greater comfort with planning for the future than we saw a few months ago, but also ongoing wariness. In general, companies are making strategic plans for lengthier periods now than they were in March 2009: then 13 percent were planning no more than one quarter ahead, a figure that has now dropped to 6 percent, while the share of companies planning for three years or more in advance is now at 38 percent, a rise from 24 percent. (Nonetheless, 20 percent of respondents say their budgets cover shorter time frames than they did before the crisis, while 15 percent say the same of their strategic plans.)

Seeking and finding more funding

In both processes, the most common change is assessing progress more frequently (Exhibit 3). Some companies are also building more flexibility into their planning, with 12 percent of those who report that their planning time frames have changed saying their strategic plans now cover more time frames than they did before the crisis, and a third saying their budgets now take several scenarios into account.

Frequency matters

In regard to who’s part of the planning, a slim majority of respondents (52 percent) say the share of executives involved in planning hasn’t changed since September 2008; just over a third report a change. In each case, roughly equal shares say half or more of their companies’ senior executives are involved in bringing issues to the attention of strategic planners (36 percent) and in making decisions (40 percent).

Volatile currencies

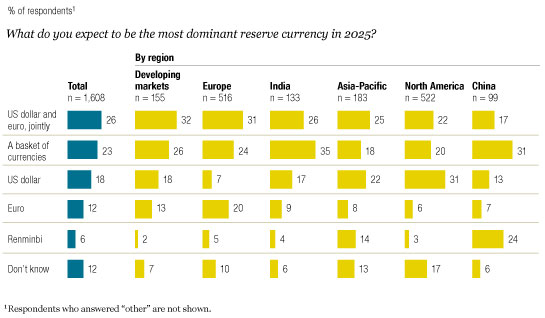

Turning to the questions on currency and exchange rates, one of the most striking findings is that only 18 percent of respondents expect the US dollar to be the dominant reserve currency in 2025; even among respondents in North America the figure rises only to 31 percent (Exhibit 4). The frontrunner, selected by just over a quarter of all respondents, is the dollar and the euro jointly, followed by a basket of currencies such as the International Monetary Fund’s Special Drawing Rights (SDRs).

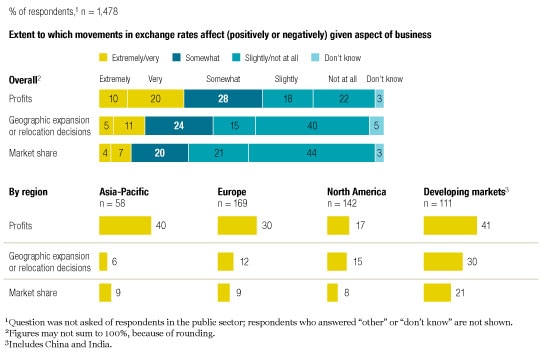

The survey indicates that both the level of exchange rates and exchange rate volatility have a large and growing effect on company profits and investment decision making. Thirty percent, for example, report that exchange rates have an “extremely” or “very significant” effect on company profits (Exhibit 5), while 21 percent of respondents report that exchange rate uncertainty has reduced their planned investment over the next two years (most report no effect). Further, 44 percent of respondents believe that the effect of exchange rates on their companies has increased over the past five years and 43 percent expect exchange rate volatility to increase over the next two years; only 21 percent expect exchange rate volatility to decline. Taken together, these results suggest that exchange rates have—and are likely to continue to have—a material effect on company competitiveness.

No currency stands alone

Effects of exchange rate movements

There is significant variation in these results. A full 50 percent of manufacturing companies, which are more likely to be in trade-exposed activities, report an “extremely” or “very significant” effect on profits. And while only 17 percent of North American companies reported an “extremely” or “very significant” impact on profits from exchange rates, 42 percent of respondents in developing markets report such a relationship.