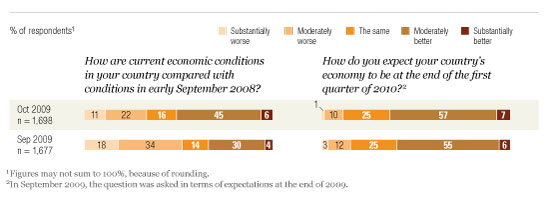

For the first time in a year, a majority of respondents—51 percent—say economic conditions in their countries are better now than they were in September 2008, according to a survey in the field during the last week of October, a volatile week for stock markets.1 A larger share of executives also expects the good news to continue, with 47 percent expecting GDP growth to return to pre–September 2008 levels in 2010 or 2011, compared with 40 percent six weeks ago. Although the global news is good, there are marked regional differences; executives in the developed countries of Asia2 are generally the most optimistic, and those in Europe are the least.

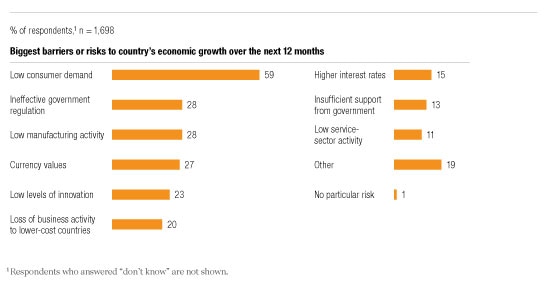

However, a majority of executives around the world share the prevailing skepticism about consumers: when asked to name the biggest threat to future economic growth and to the growth of their own companies, more cite low consumer demand than anything else. Ineffective government regulation is the next biggest economic concern, respondents indicate, followed by losing business to low-cost competitors.

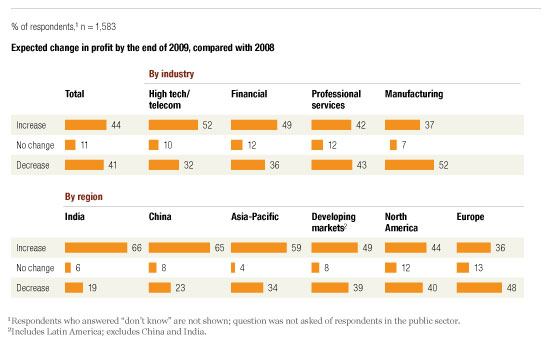

Looking ahead, respondents’ views on company profits and workforce size haven’t meaningfully changed in the past six weeks. Pluralities still expect increased profits in 2009 and no change in their workforces through the first quarter of 2010. Here, too, however, there are notable regional differences.

Where economic optimism is highest

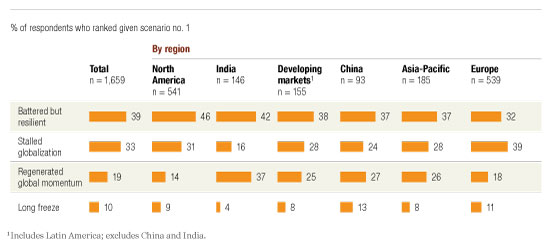

Although 51 percent of all respondents say economic conditions are better than they were last September (Exhibit 1), only 19 percent say an upturn has begun. This figure rises to a remarkable 33 percent, however, among respondents in Asia’s developed countries. And about a quarter of those—more than in any other developed region—also say the best way to describe the global economy through the end of the first quarter of 2010 is “regenerated global momentum” (Exhibit 2).

Steady improvement

More momentum in Asia

Respondents identify several potential stumbling blocks to economic growth, most often low consumer demand (Exhibit 3). Other potential barriers to growth vary by whether respondents expect their nations’ GDPs to increase or decrease. In countries where executives expect an increase in GDP, more are also worried about currency values and inflation; in countries where executives expect a decrease, they are notably more concerned about ineffective regulation.

Threats to growth

Status quo for companies

Executives’ hopes for their companies haven’t risen in tandem with their economic expectations. Compared with six weeks ago, nearly identical shares expect increased profits in 2009 (44 percent) and plan to maintain their workforces at their current sizes over the next few months (46 percent).

However, there are significant differences in the profit expectations of executives in different regions and industries (Exhibit 4). These are largely parallel to respondents’ economic expectations. For example, among respondents in developed economies, more in Asia than elsewhere foresee an increase in profits.

Mixed expectations on profits

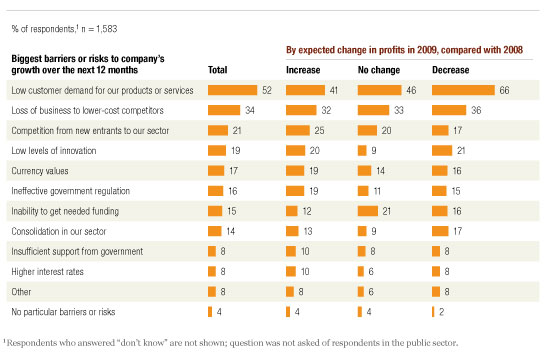

Looking ahead through the next 12 months, more than half of respondents expect their companies to continue cutting costs (although this percentage is far lower than the share of companies that have already done so). Half of all respondents expect their companies to focus on productivity growth and the introduction of new products or services—far more than have done so over the past year. However, executives are worried about customer spending: 52 percent cite low demand as the biggest barrier to their companies’ growth, and a third fear losing business to lower-cost competitors (Exhibit 5).

Worried about customer spending

Some concerns vary by profit expectations, but not as many as might be expected. A low level of innovation, for example, is important to almost equal shares of executives at companies expecting higher and lower profits.