This episode of the Inside the Strategy Room podcast features excerpts from an address that McKinsey senior partner Chris Bradley gave at our recent Global Business Leaders Forum. He discusses the eight practical shifts that executive teams can make to move their strategy into high gear. This is an edited transcript. You can listen to the episode on Apple Podcasts, Spotify, or Google Podcasts.

Sean Brown: From McKinsey’s Strategy and Corporate Finance Practice, I’m Sean Brown. Welcome to Inside the Strategy Room. In today’s episode we will hear from Chris Bradley, a senior partner based in our Sydney office and one of the authors of McKinsey’s recent book Strategy Beyond the Hockey Stick: People, Probabilities, and Big Moves to Beat the Odds (John Wiley & Sons, 2018). In our two earlier podcasts, Chris and his co-authors, Sven Smit and Martin Hirt, talked about how social dynamics and biases can undermine strategy development, and explained the power curve of economic profit, which shows how well—or how poorly—the strategies of the world’s largest companies are succeeding. We also heard about the most important strategic moves companies can make to rise up that power curve.

Today we’d like to share excerpts from a presentation Chris gave at our Global Business Leaders Forum in New York. Chris will take us through some of the practical changes that companies can make to their strategic planning process to unlock those bold moves.

Here’s Chris on how he and his co-authors approach the challenges faced by executive teams in the strategy room, and how they help them make the first shift.

Chris Bradley: Business books are notoriously boring. To make any story interesting, you need a villain. If your goal is to scale the power curve of economic profit and make big moves to beat the odds of strategic success, the villain is the thing that gets in your way of achieving that goal. What is it that gets in the way? It’s called the social side of strategy. This villain is a funny one. Rather than causing big catastrophes, it usually causes inertia, and the risk that your company moves slower than the market it’s in.

This is how it works. You start your strategy season with high hopes. You’re going to make the big moves. You will get on top of the trends. But when you get to the strategy room, you find it crowded with all sorts of stuff. There are negotiations, there are egos, there are last year’s plans. There are other people, and you want to look good to them. There is so much else going on than just strategy. So, we ended our book with a kind of manifesto for how you could manage your company differently.

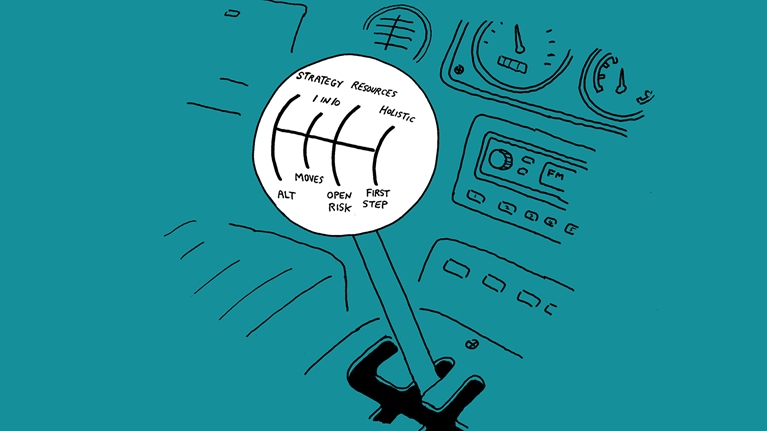

What we need to do is reengineer the way we do strategy. There are eight shifts we propose (exhibit). The first one concerns planning. It’s extraordinarily important to know what is going to happen next month, what resources need to move, and what initiatives you have to launch. The problem is, that’s a different mode of thinking from strategy. As soon as you put strategy and planning together, planning will always win. The shift we suggest making is to go from this annual planning ritual to treating strategy as a journey.

Let me make that practical: you need a two-track process. First you need an efficient way of doing your plans—that’s really important, making sure the budget lines up every year. But you need a parallel track to do strategy, and that has completely different timing. By the time you come to planning, you should already have your strategy in mind.

I’m going to bring this to life through what we call micropractices. If you want to reengineer the way a company works, you can talk in themes and theories, but it tends to come down to lots of small things you do differently. For example, some companies have, outside of their normal strategy-planning season, a set of regular meetings with an evolving agenda of big strategic topics and stimulating discussions about them to make decisions, so you get into a discipline and a cadence of strategic conversations. That’s a micropractice. It’s very rare, but increasingly we’re seeing companies move to more agile ways of working, even outside of the tech space.

Strategy plans are often elaborate management ballets perfectly choreographed to do only one thing, and that’s get to a yes.

Something fascinating happens when they go agile. They discover, “Oh, our planning processes actually don’t work anymore because we are now in this 90-day cycle.” I think agile is an exciting place for strategists to find inspiration because of this idea of having a story updated every 90 days that then cascades down into all the squads and tribes.

So, the idea with the first of the eight shifts is, how do I continually go from big goals to little goals in a much more robust way. This is strategy as a journey.

Sean Brown: The second shift Chris identified was about encouraging the strategy team to debate real alternatives rather than simply seeking to get a yes to the proposal on the table. Here is Chris again.

Chris Bradley: Strategy plans are often an elaborate management ballet that seems perfectly choreographed to do only one thing, and that’s get to a yes. That’s because what do you walk into the room with? A proposal. And if you walk into a room with a proposal, a good outcome is acceptance of your proposal—and usually it’s the last page that matters, which is where you ask for the resources you need.

This is just entirely the wrong place to start strategic planning. You need to debate real alternatives. Let me bring this to life with a bit of research I came across about how private-equity firms make investment decisions. An experiment put teams in two rooms. One evaluated investment decisions one at a time and the other compared two simultaneously. What they found was that there was a 30 percent difference in decisions between the two. Later, when they did a randomized trial, they found that the team with two alternatives to consider always made the better decision. The fact packs were the same, but the room weighing two alternatives did a better job of digging into the footnotes. That’s because the investment case always has the problems in it but usually they are summarized in the footnotes or the appendix. Having two alternatives to choose from just made it safer to dig into the cons.

In that sense, what I would argue is, this idea of working from a single proposal or the one-off plan introduces a 30 percent error into what you are doing. See, in the world of getting to a yes, everyone has high market share. There’s a famous story that Jack Welch, when he took over GE, said that every business had to be number one or number two in its segment. Of course that happened, by people playing the denominator game—everyone’s market got really small and so they became number one or number two instantly. He said then, “No, no, no. Now you have to define your market so that you have less than 10 percent market share.” He found a way to get through the problem with the proposals. But the reality is, most companies don’t work like this. They are not comparing alternative plans. Their strategies are framed more around promises and financial goals than they are around choices.

Sean Brown: In Strategy Beyond the Hockey Stick, the authors emphasize the importance of making big, bold commitments to initiatives that can really elevate the company’s performance. But it’s hard for most companies to move resources around in a big way. Next, Chris addressed ways to get resources moving dynamically toward businesses with the greatest potential.

Chris Bradley: The harsh reality of the way we do strategic planning now is, there is a pot of money and we all compete for it. But when we did our research on companies that rose up the power curve, we found that it usually was not the whole company improving but one or two out of ten business units that disproportionately went up. It’s just a small part of the company that explosively grows.

That’s easy to logically understand, but when you’re in the strategy room and trying to be one of those winners, you may create a lot of losers. And you can see how, with the social side of strategy, that really becomes a problem. If you ask ten business-unit leaders in the room, “Which of you runs the bottom five units?” you will get a uniform answer: none of them is in the bottom five. But if you ask them which is the one business the company should disproportionately back, they usually know which it is.

So, what we want to do is go from spreading resources evenly like peanut butter, which is the enemy, to picking one-in-tens with breakout potential. That means we must deal with some tough stuff. An example is the Dutch semiconductor firm NXP. They went from around $2 billion market cap to $25 billion, and at the source of that were tough choices. They moved 70 percent of their R&D to backing just two of the 13 trajectories they had. But to do that, you create 11 losers. So how do we make winners out of losers? Reckitt Benckiser is an innovative consumer-goods company, and they are also quite innovative in their management practices. They have taken the concept of granularity and taken it to the extreme whereby they’re running 200 markets and 106 brands. That’s a big matrix. But what’s really interesting is that they have chosen 19 brands in 16 markets that they call “power cells.” These get disproportionately more resources.

Subscribe to the Inside the Strategy Room podcast

If you think about the level of visibility that such practices imply for resource allocation, it’s much different from what you get when you just roll up a bunch of business-unit (BU) plans—an order of magnitude of difference. Also the leadership style is very different, because instead of talking to each BU president and accepting their plan as a package deal, you actually have portfolio visibility at three or four levels down the organization.

Sean Brown: The next shift Chris explained is the transition from simply negotiating budgets to discussing the big moves a company needs to make.

Chris Bradley: Strategic planning is often just a cover for the real game, which is the three-year plan. Once you have anchored your strategic plan on the numbers, you’ve lost the plot because now you’re negotiating. What do you do about that? We go from budgets to moves, and what I mean by that is, don’t start with the numbers you’re going to achieve; start with the moves you’re going to make.

The enemy here is the base case, which is usually an extrapolation enabled by Excel, because when you click on a cell and you get the little crosshair and you drag it across, it’s easy just to extrapolate. The problem with it is that you extrapolate away the fact that the management team before you worked very hard to get those results—that’s not a base case. But you lay your strategic initiatives on top of it anyway, and then usually there is a gap in your waterfall chart to budget that says “stretch.”

That doesn’t work. What we propose instead is to ask, what is the momentum case of the business? In other words, if you just kept your current policies and capabilities, with no new initiative or investment, what would happen to the business? Some businesses do OK; they may have a lot of tailwind. For most businesses, however, the momentum case will be frightening. If you take your pedal off the metal, most companies will fade out pretty fast. So, if you’re a retailer and you stop refurbishing your stores, your comparable sales will fall quickly, and when your comp sales fall, that will very quickly leverage into your bottom line. It’s frightening, but that’s the right basis, because then you can calibrate. “OK, if that’s my momentum case, how much do I need to do to get to my aspiration? And what will get me there?” It focuses the discussion on the moves you need to make.

The most important thing to start with is, know your business really well. Often, we think the hard part of strategy is that we have to guess the future. I think the hard part of strategy is busting your own myths. The most important question a strategist can ask is, why do we make the money? I think of it like being on a dirt road in the Australian outback and you look in your rearview mirror. It’s very hard to see where you’ve been because a lot of dust has been kicked up. For the social side of strategy, this ambiguity about the past ends up being really useful, because you can say that when you did well, it was management prowess, and when things were tough, it was because of the weather. Remember, in the strategy room, it’s important to look good.

Rather than negotiating a financial promise, put some calibration around your moves. There is an increasing trend of basing investments purely on artificial intelligence, which judges an investment story based on many variables, then spits out a probability. That’s a good way of also getting the approving of budgets out of the way. And then AI [artificial intelligence] will tell you, based on how much you are investing and your technology and the sector you’re in, what your budget should be—as an outcome, not as an input.

If you want to drive strategic change in your company, you should be its chief liquidity officer. You can’t move resources that aren’t liquid. In other words, you cannot reallocate if you don’t also de-allocate.

Sean Brown: Once the company has decided on which moves to make, the next challenge is following through and allocating sufficient resources to those priorities. That’s not easy. Chris talked about how to free up those resources. He then explained how managers can overcome sandbagging and risk aversion.

Chris Bradley: There is often a rude awakening. While we’ve all agreed that we will move resources to businesses B and C, on Monday morning we discover that we don’t have any resources to move. The reality is, most companies can’t responsibly move those levels of resources on a dime. In a recent survey my colleague Tim Koller did, only 30 percent of managers agreed that their budgets were aligned with the three-to-five-year plan. That’s a lot of dissonance.

So how do you create liquid resources? If you want to really drive strategic change in your company, you should be its chief liquidity officer. You can’t move resources that aren’t liquid. In other words, you cannot reallocate if you don’t also de-allocate. By the way, in a survey we did, this was the shift that respondents admitted they struggle with the most. Only 5 percent agreed that resources at their companies are freed up ahead of time to create a kitty of contestable funds in the annual budget.

A root cause of this is that managers are not charged an opportunity cost. I work a lot in retail, and I’m always bugging CEOs to measure their buyers on return on space, because otherwise they will never give shelves back to you. If they are measured on sales, they will always want more space. I’m sure you can apply the same principle in other businesses.

Here is another idea. Everyone has heard of zero-based budgeting, but it’s completely unrealistic. I can’t zero-base my bank branch network tomorrow because it’s already there. But what about 87-percent-based budgeting, or 93-percent-based budgeting? In other words, create a norm where you force contestability over that last bit of resources. A big part of this is about de-anchoring next year’s budget from being this year’s budget.

Let me introduce another problem. My colleague Dan Lovallo is a professor who works in applying psychology on biases to management topics. A simple test he did at an investment bank showed that if you applied the CEO’s risk tolerance to all the investment decisions made at lower levels rather than the more junior decision makers’ risk tolerance, the decisions would have had a 32 percent better outcome. So, there is this tax of risk aversion, and it makes sense: if you’re the CEO, you feel pretty diversified because there are probably 20 or 30 bets sitting in your portfolio, so you can afford a few fails. But you are asking your business-unit leaders to take undiversified risk, and then get killed on their key performance indicators when they don’t hit the numbers. It should be little surprise then that a lot of the risk gets edited out of the system.

The shift I want to encourage here is to go from this sandbagging to open risk portfolios. In other words, go from your strategy being lots of mini hockey sticks that you add together to one big hockey stick that has many risk trade-offs made at the enterprise level. There is a simple way of doing that: don’t have cross-subsidization by creating attacker units that report separately. That’s super-important in a world of digital disruption. Companies often try to protect their earnings core from growth businesses. One way to undo the package deal is to separate those different types of businesses.

Sean Brown: Chris then went on to explain how CEOs can promote the mind-set that will encourage business-unit leaders to take the risks that will help the overall company reach its aspiration.

Eight shifts that will take your strategy into high gear

Chris Bradley: We get what we incentivize. We ask our managers to hit their budgets 90 percent of the time and then criticize them for being too risk-averse. We love scenario analysis at strategy planning time, but who has ever seen that scenario analysis brought out again at performance review time?

One thing I propose is throwing out balanced scorecards. They are not very good because you end up having 20 goals, each at 5 percent, and therefore no individual one matters. Unbalanced scorecards are much better, because then the total potential bonus is driven by financial outcomes, but it may be reduced by how you got to that outcome. We have to reengineer how we evaluate people, particularly in risky contexts. Rather than “you are your numbers,” take a holistic performance view.

How do we make sure noble failures get rewarded and dumb luck does not? It’s interesting that in our survey, by far the most respondents said they believe their companies, when evaluating performance, penalize noble failures and don’t recognize the risks someone took. There is some missed wiring in the way the incentive system works, so it’s little surprise that we are not getting these big moves to happen. One innovation private equity brought in is basing incentives on having more skin in the game over a longer period of time.

Sean Brown: The final shift Chris discussed is the move from long-range planning to forcing the first step. He described how you can’t finish the strategy meeting until you have figured out what you will do tomorrow to start putting it into action.

Chris Bradley: I’ll describe this last shift with a story that’s relayed by my co-author Sven Smit. He was with insurance executives and everyone had just listened to this truly inspiring presentation about the paperless future of insurance. The CEO asked an inconvenient question: “I love this presentation, but how much paper are we budgeted to use next year?” And there was a bit of shuffling of feet, and I think someone had to go out of the room to find the number. The answer turned out to be 5 percent more paper. The CEO said, “I love the paperless future, but maybe next year can we do minus 5 percent paper use? Can we start there?”

So, a lot of this is about setting the most radical goal that’s achievable in a six-month period. That should be the first challenge.

I want to take the pressure down a bit here. These shifts are hard to do. If you get good at even a few of them, you are straightaway putting yourself into some seriously rare territory. There is a reason, aside from the fact that markets are competitive, that companies aren’t making big moves. It’s because the social side of strategy overwhelms them. Maybe make some of these shifts, think boldly, be aspirational, and do it not just by having fancier presentations and nicer-sounding initiatives but by really getting inside the social side of strategy in your company.

Sean Brown: Thank you for joining us for Inside the Strategy Room today. You can learn more about these shifts to the strategy-development process in “Eight shifts that will take your strategy into high gear.” You can also do the Eight Shifts Diagnostic to see how well your executive team is performing on each of the eight shifts and how your performance compares to other companies. And, of course, you can find more information in the book, Strategy Beyond the Hockey Stick: People, Probabilities, and Big Moves to Beat the Odds.

Related Articles

Eight shifts that will take your strategy into high gear