The bigger a company gets, the harder it is to keep up with investors’ expectations for growth. Mergers and acquisitions are essential, but how big do deals need to be—and how frequent? Because a single deal that might double the market capitalization of a small company will scarcely register for a large one, many big companies pursue ever-larger deals—or a whole lot of smaller ones. Does either of those strategies more often lead to success?

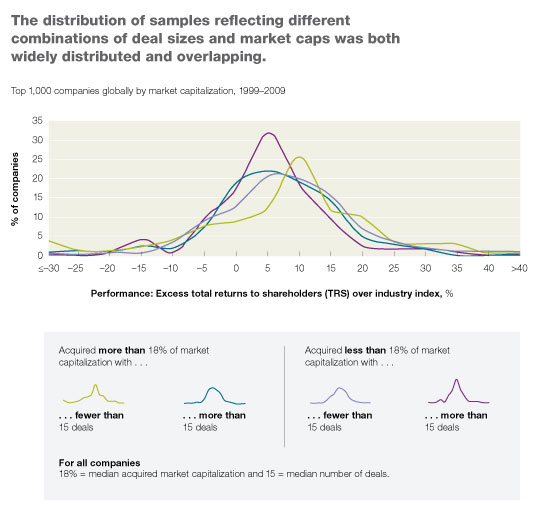

Apparently not. Patterns of deal size and frequency have made little difference in performance as measured by excess total returns to shareholders (TRS) among the world’s top 1,000 companies1 by market capitalization. It seems not to matter much whether companies completed one large deal, many small deals, or few deals. In statistical parlance, the distribution of samples reflecting different combinations of deal sizes and market caps was both widely distributed and overlapping. From a value-creation perspective, this finding means that the size and number of deals matter less than the discipline with which they are identified, priced, integrated, and managed.

Related Articles