Many leaders set unrealistic growth targets. Often, they don’t properly consider how fast their underlying markets are growing and thus how much market share must be grabbed to meet ambitious goals. Or they ignore the likelihood that their competitors are doing many of the same things to grow. They also underestimate the ongoing need to find new products to replace revenue declines from current offerings as they mature.

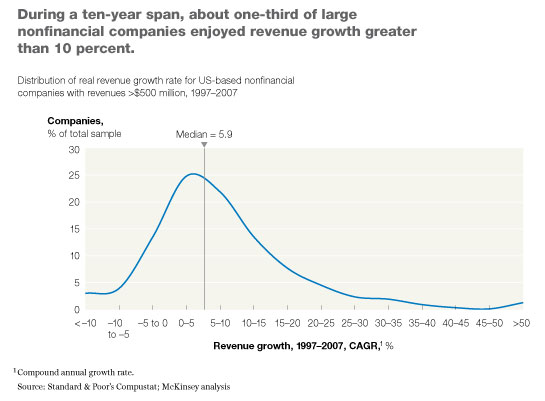

A historical look at corporate performance puts the growth challenge into perspective. The first exhibit shows the real revenue growth distribution for large nonfinancial companies from 1997 to 2007. (We ended the analysis in 2007 to avoid distortion resulting from the severity of the recession that began that year.) The median revenue growth rate was 5.9 percent. About one-third of these companies increased their revenues at rates faster than 10 percent. But that one-third figure probably overestimates organic growth, since it includes the effects of acquisitions.

Over a longer time horizon, other difficulties come into view. The second exhibit presents real 1965–2008 revenue growth for the 500 largest nonfinancial companies in the United States. The median was 5.4 percent a year. Although the rate fluctuated from 1 percent to 9 percent according to the economy’s health, there was no upward or downward trend and thus no rising tide to lift growth over the longer haul.

During this same period (1965–2008), median GDP growth in the United States was 3.2 percent, meaningfully lower than the corporate revenue growth rate. How did companies grow, in the aggregate, faster than the economy did? The biggest factor is that US companies have been globalizing, so their revenues from countries outside the United States—48 percent of the total in 2008—have been growing much faster than their US revenues. Many companies are counting on global growth, particularly in emerging markets, to go on driving them forward. But a rising number of companies around the world are competing for a share of that momentum.

Finally, it’s worth bearing in mind just how many casualties the growth game has. Beginning in the mid-1970s, a quarter of all the large companies we studied actually shrank in real terms in a given year. That’s sobering, since most companies today are publicly projecting healthy growth over the next five years. In fact, many of these mature companies will get smaller in real terms. In related research, we find that a startling 44 percent of all companies that grew at rates faster than 15 percent from 1994 to 1997 were growing at rates lower than 5 percent ten years later.

Although the importance of growth is undeniable, large companies should have a realistic view of the challenges they face and the implications of aggressive targets. Pursuing above-average growth rates—8 percent, say, rather than the 5 percent gains of a company’s underlying markets—means that a $10 billion company must add $11.6 billion (rather than $6.3 billion) in revenue per year by the tenth year to meet its goal. While that is undoubtedly realistic for some companies in some industries at some times, the headlong pursuit of fast growth can also yield bad decisions. Over the long haul, it can overshadow the benefits of patience and discipline: patience to nurture new growth platforms over many years and discipline to uncover the types of growth that will create the most value.

Related Articles