Thanks to the boom in US unconventionals, the supply of natural-gas liquids (NGL) is at record levels, and growth shows no sign of slowing. Meanwhile, petrochemical demand is also strong, keeping prices stable. As a result, investment opportunities are emerging across the value chain.

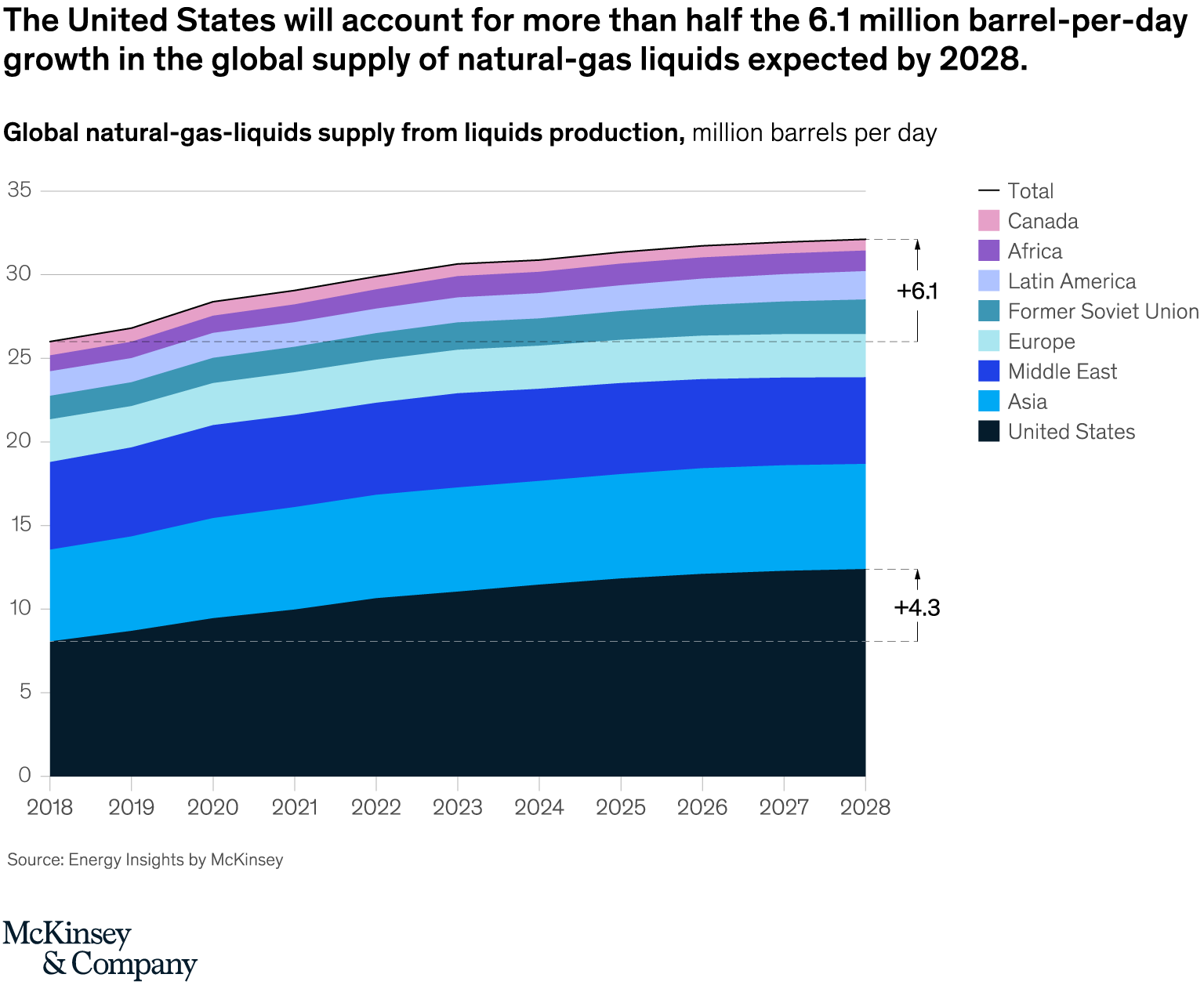

No end in sightThe boom in unconventional oil and gas development has led to a massive increase in the supply of NGL. Over the past decade, the United States has become the largest global source of new NGL supply and a major NGL exporter, with volumes reaching 1.7 million barrels per day (bpd) in 2018, most of it going to markets in Asia. McKinsey’s latest supply outlook forecasts growth of another 4.3 million bpd by 2028, most of it from the Permian Basin (Exhibit 1).1

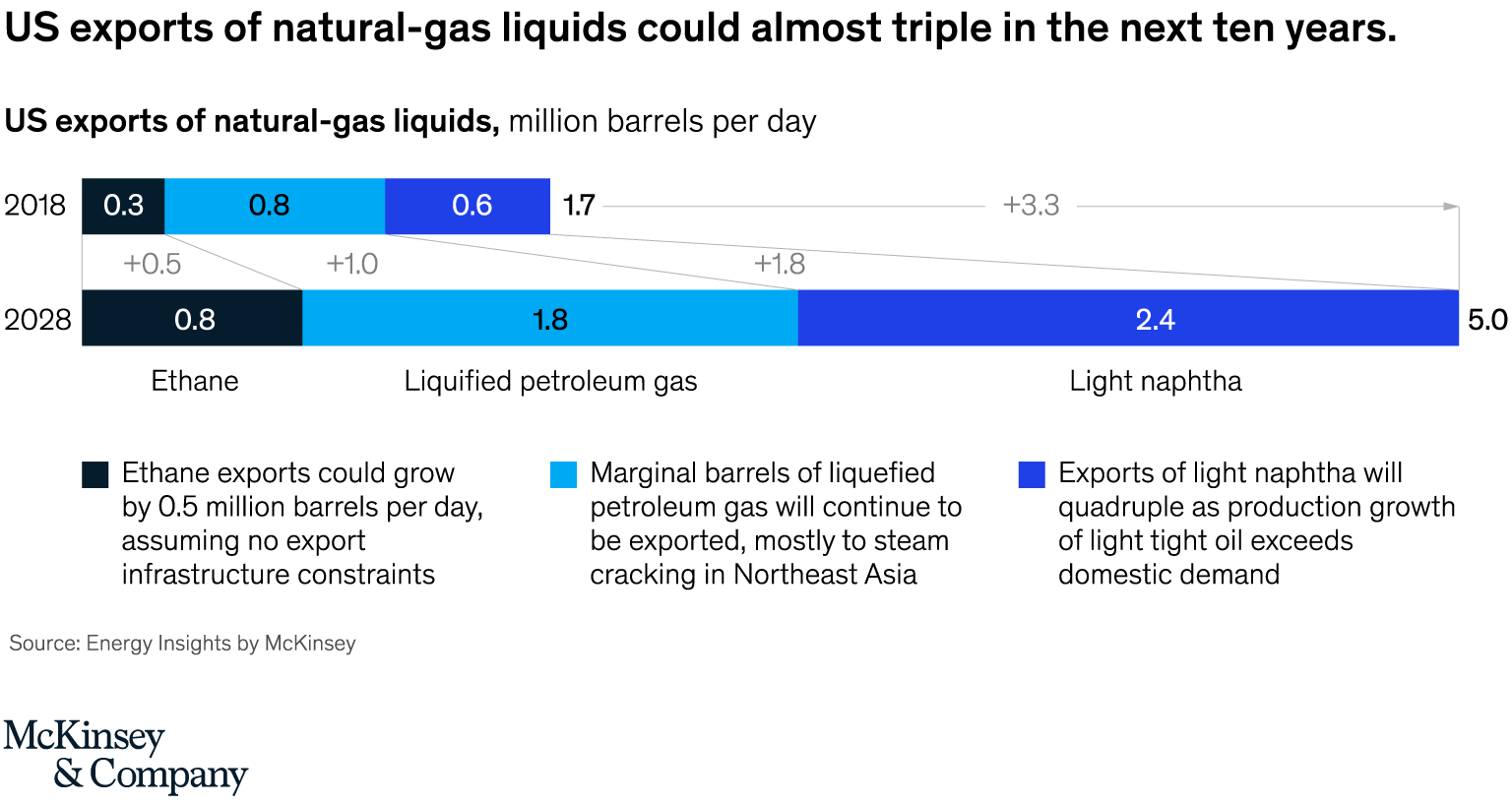

Despite the aggressive expansion of US fractionation capacity, we expect this growth to drive up US exports by 3.3 million bpd by 2028 (Exhibit 2). At present, 1.6 million bpd of new fractionation capacity is under development, most of it focused on the Gulf Coast. We can expect about 0.9 million bpd of new domestic petrochemical demand to come from new cracking capacity. But most of the supply growth will go into the export market, especially Gulf Coast volumes heading to east Asia.

Overall, the 4.3 million bpd of US NGL-supply growth will be consumed by 3.3 million bpd of exports and 1.2 million bpd of domestic demand growth, while demand from naphtha blending for gasoline will decline by 0.2 million bpd.

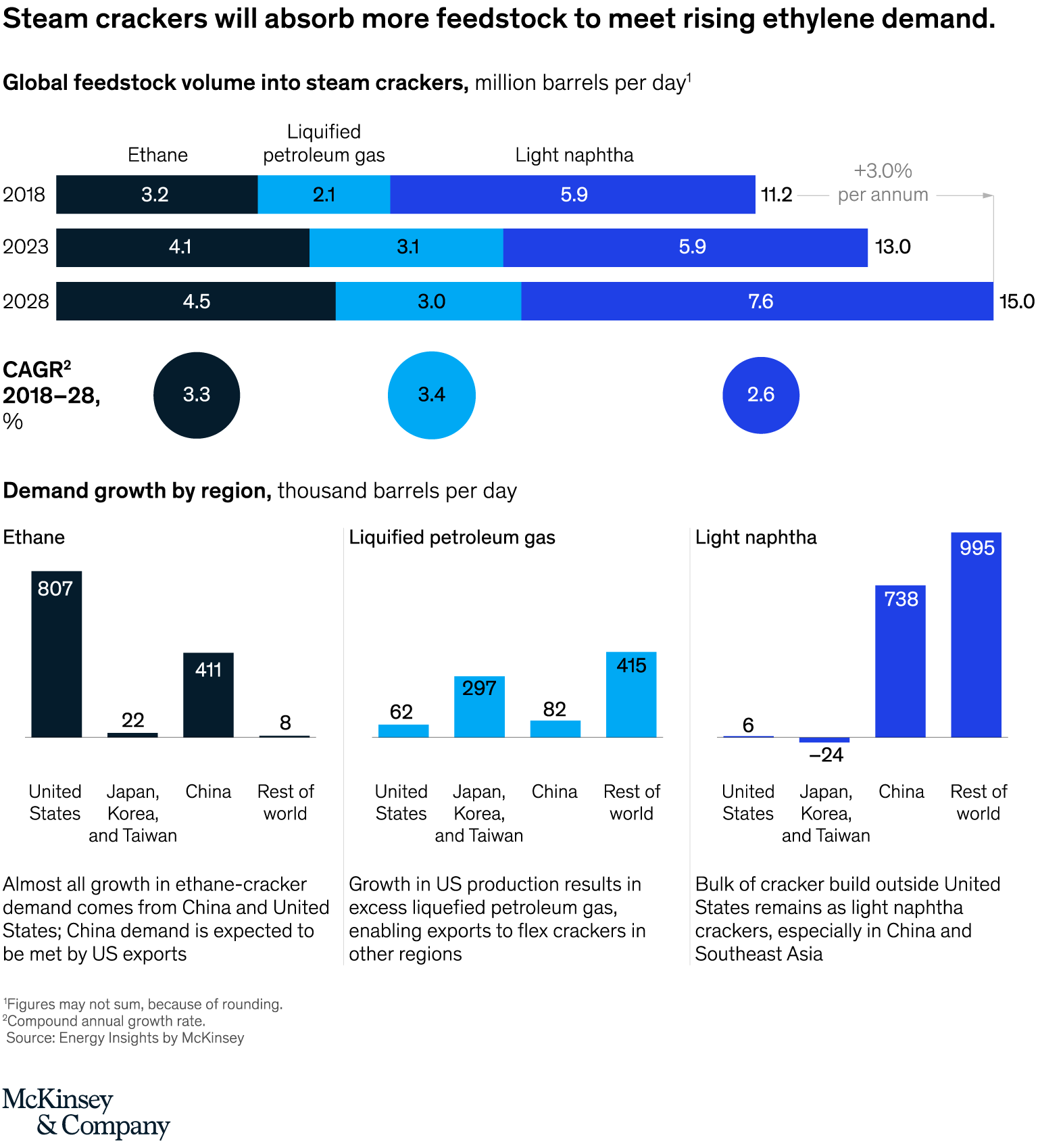

Asia keeps soaking it upAs supply has boomed, the demand for liquefied petroleum gas and naphtha has kept pace, and it will continue to do so. Over the next decade, 3.9 million bpd of new cracker capacity will be added to fuel the growing global demand for olefins-based plastics, most of which comes from China, Korea, Taiwan, Japan, and Southeast Asia. The increasingly close match between North American supply and Asian demand is evident in the large and steady flows of product from one region to the other.

Despite this dramatic volume growth, pricing has remained fairly stable. Most of the incremental liquefied-petroleum-gas volume is absorbed by crackers, with naphtha taken as needed to fill the remaining capacity (Exhibit 3). This has created a balancing mechanism that relies on the flexibility of the gigantic Asian gasoline pool to absorb varying volumes of light naphtha, providing not only market equilibrium but also a pricing mechanism for naphtha that reflects its value as a low-octane gasoline blendstock. In turn, this value provides a basis for propane and butane pricing as competitive feedstocks to crackers.

The outlook of tremendous growth in supply and demand has prompted concerns in the industry that pricing stability could be disrupted in future. However, our forecast indicates that supply and demand will continue to grow at similar rates up to at least 2035. In addition, the room for the gasoline pool to absorb varying volumes of light naphtha under current price mechanisms will far exceed the uncertainty in the balance between supply and demand.

But this is not a Goldilocks-like story where everything is “just right.” With such strong growth, some bottlenecks and price disconnects will be inevitable. We believe they are most likely to emerge in the logistics chain connecting supply and demand.

Keep your eyes on the roadThe road from US production to Asian cracker consumption is a long one, and each step presents risks as well as opportunities. Here is our advice:

- Upstream players should look to secure infrastructure capacity and potential long-term supply agreements for offtake, both in the United States and abroad.

- Midstream players should track local and supply demand trends to anticipate infrastructure needs and invest in capacity to serve challenged volumes. This should include investments to bring Permian Basin crude to the international market—for instance, via an emergency secondary fractionation and export hub west of Houston.

- Petrochemicals players should look to shift cracker feedstocks based on midterm trends in the relative pricing of ethane, propane, and butane.

* * *

With supply and demand for NGL booming, the prospects for the next decade look bright. But players should watch out for bottlenecks and price disconnects in the logistics chain connecting US production with Asian cracker consumption.

Tim Fitzgibbon is a senior expert in McKinsey’s Houston office, where Autumn Hong is an associate partner and Arturo Pizano is a consultant.

1. For a summary of the report, see “Global gas and LNG outlook to 2035,” September 2019, McKinsey.com.