More than 140 million Americans currently have discretion over health insurance purchases, representing a total of $785 billion in premiums or premium equivalents. Yet most are unable to revisit their current insurance status. A combination of economic anxiety, confusing insurance products, and inadequate distribution is leading to consumer paralysis. Moreover, our research suggests that millions would fail to make rational economic choices even if they understood their options better. Unlike employers that purchase health insurance for their workers, consumers approach this issue by factoring in much more than expense management. More specifically, consumers’ purchasing decisions are often emotionally based, as they are seeking peace of mind in their choices.

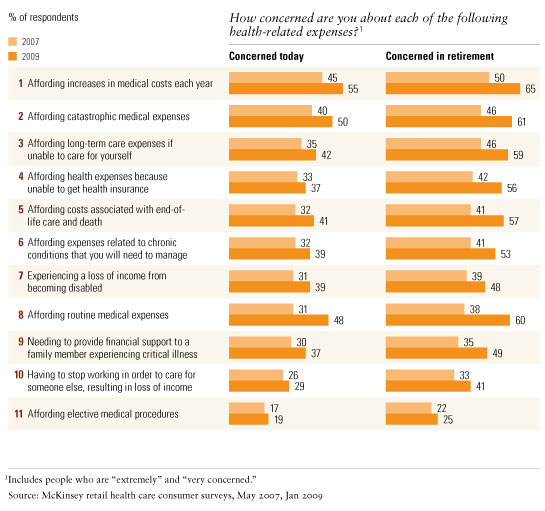

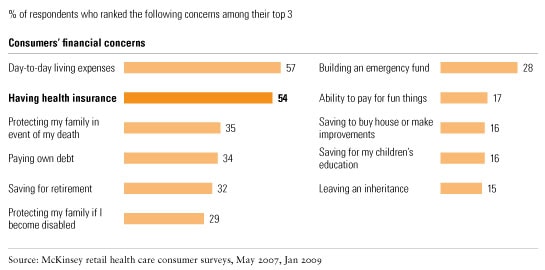

Despite rising concern and stated willingness to purchase health insurance products (up 11 percentage points since the survey we conducted in 2007), sales have not kept pace with demand—in fact they have remained steady while the amount of shopping has increased (see sidebar, “About the research”). Forty-one percent of retail health consumers report actively shopping, a proportion that has been growing rapidly. And no wonder: the number of people with health-related financial concerns has increased by more than ten percentage points (Exhibit 1), making consumers more willing to consider new trade-offs to protect themselves against health care financing exposure. For Americans, health coverage is the second-highest concern, after day-to-day living expenses (Exhibit 2).

Growing concern

Health insurance worries

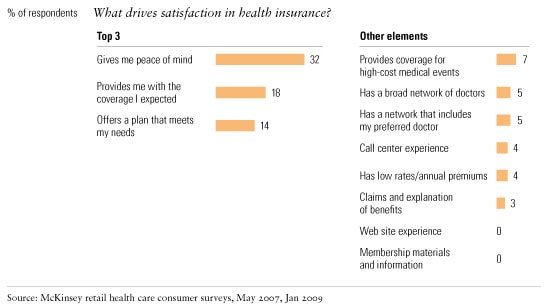

What is preventing health insurers from effectively addressing this pent-up demand? Our research suggests that a primary barrier is their belief that consumers make economically rational decisions about health benefits. It’s a misguided view. Faced with more choice, complexity, and financial exposure for their health care in an increasingly uncertain world, what consumers are really seeking is peace of mind (Exhibit 3).

The value of peace of mind

If industry participants are to convert concern into increased sales—and win in the market—they must address these emotional concerns directly. That, however, will require a flexible approach and a new mind-set, which must be embraced across the entire organization. But the benefits are clear. We estimate that closing the gap between consumer needs and product purchase could increase health insurance revenues by as much as $200 billion. What’s more, our research shows that high-performing health insurers convert three times more consumers into purchasers than lower-performing ones do. Insurers that focus on the following five areas will have a better chance of meeting the true needs of health care consumers.

Educate consumers

Although consumers are anxious, few understand the severity, or probability, of the risks they face. Health insurers can benefit from educating consumers by helping them translate concern into action, thereby expanding the market. For example, 73 percent of consumers who purchased individual insurance felt that they understood their health insurance options, compared with 51 percent of the uninsured.

Most consumers are unaware of how much major medical procedures actually cost: three out of four consumers report having “no idea” how much they cost. Additionally, few consumers accurately assess the probability of certain health-related risks. Most overestimate the risks of salient but relatively low-probability events (fatal accidents, for example) and underestimate the risk of more common health events (such as heart attacks).

Educating consumers is an essential part of motivating them to address their concerns. Messaging, for example, really matters. Cost–benefit information alone fails to address emotional anxieties. Consumers often respond much more effectively to anecdotes than to a recitation of facts. For example, concern over health care financing increases significantly when a friend or family member experiences a financial crisis—often more than it would given a similar personal experience.

To educate, insurers should make better use of their traditional channels, whether it’s a captive sales force or independent agents. They will also need to explore emerging social-networking and Web 2.0 approaches. For example, sites such as PatientsLikeMe.com are showing how insurers can use these new technologies to get closer to consumers. It is possible to imagine such a site, or similar ones, extending beyond disease-specific networking to consumer suggestions on what health insurance to buy.

Create a flexible purchase experience

When buying insurance, consumers typically frame their approach around effective shopping experiences in other markets, yet health insurers continue to create barriers to purchase by offering a confusing and overwhelming experience. Once consumers decide to consider insurance options, a quick, simple, and personalized experience increases their propensity to purchase. Our research shows that three elements are critical in delivering this kind of purchase experience.

Engage at the right time

Consumers tend to make decisions when confronted with a change to the status quo. A job change or loss, retirement, and eligibility for Medicare are the most common motivators for consumers to purchase or switch health insurance. Similarly, consumers who have recently experienced a medical event are 13 percent more likely to shop for insurance and 27 percent more likely to make a purchase—and much more likely to purchase supplemental products. In fact, consumers highly concerned about their health-related financial exposure purchase 60 percent more products than the average consumer; nearly two-thirds of concerned consumers own five or more products, compared with less than half that for the average consumer. Insurers should tailor the purchase experience around these life events and address consumers’ emotional needs directly.

Consumers are also more open to addressing multiple concerns at the moment that they decide to purchase. In retail banking, for example, more than 70 percent of sales happen the day a customer opens an account. In a similar fashion, health insurers should be ready to deliver a full suite of products at the moment the consumer is looking to buy. Today, only 15 percent of individually insured people purchase an additional product (for example, pharmacy, dental, or vision coverage) when they first purchase health insurance. Offering consumers multiproduct, multiline sales—a seamless, integrated sale that involves a single application and multiproduct underwriting—at the moment when they decide to address a risk can increase the chance of success. Multiline sales also minimize redundant coverage across disparate products.

Be personal

Consumers want their needs addressed during the sales experience. Seventy-seven percent of those who purchased health insurance felt that the distributor provided options to meet their needs, compared with only 46 percent for those who ended up not making a purchase decision. Similarly, 81 percent of consumers who purchased health insurance felt that the distributor had a good understanding of their situation during the purchasing process, compared with 44 percent for those who did not make a purchase. Customers who have their questions answered and who feel that the distributor was less self-interested are more inclined to purchase. When approaching the purchasing experience, insurers should make sure they address consumers’ emotional needs directly and provide solutions that are specific to them.

Keep it quick and simple

When faced with complexity or too many choices, consumers often fail to act. For example, 74 percent of those who purchased health insurance were satisfied with the ease of the process, compared with 47 percent of those who shopped but didn’t purchase. Few consumers can comprehend the detailed information presented to them—in fact, a third of those who found the purchase process confusing cited “too much information” as the main barrier to purchasing. Health insurers should make it easier for consumers to make choices by offering simple, understandable information. Unfortunately, there are few examples of best practice in the health insurance industry in this realm, although many exist in other industries (such as auto insurance).

Comprehensively addressing the consumers’ health-related financial exposures (health, disability, long-term care) can involve bringing together multiple companies or distributors, further increasing complexity and confusion. To simplify the decision-making process, insurers should present consumers with multiple product options—for example, a recommendation together with one or two comparable alternatives.

Consumers who do purchase or switch health insurers report that the purchase process was fast. The likelihood of individual purchase correlates strongly with the turnaround time for the application. For example, 55 percent made a purchase when the process lasted only a few minutes, compared with 21 percent for a Web transaction that took place over a 24-hour period. Most consumers are also unlikely to shop multiple channels—more than half only use one source of information, although it varies by segment—so rapid access and ability to transact quickly across a range of channels is important. End-to-end improvements of the acquisition process based on lean improvements and front-end automation can help make the process more customer-centric.

Earn the consumers’ trust

Overwhelmingly, consumers cite trustworthiness as the most important factor in considering or staying with a health insurer. Insurers must develop a reputation that offers peace of mind by consistently delivering on their brand promises. Brand awareness is important, particularly since the average consumer considers only two companies when shopping. But trust is critical to driving sales: consumers are two to three times more likely to consider insurers with a strong brand reputation.

Develop a trust-based reputation

Delivering peace of mind is similarly important in retention and capturing the cross-sell opportunity. In the face of inertia and complexity, 71 percent of consumers prefer to stay with their current insurer. Yet this depends on whether their health insurer delivers on its promise: consumers who leave insurers are 13 percent less satisfied with them than consumers who chose to stay.

Although insurers can buy brand awareness, brand reputation must be earned. Whether they offer great service or low cost, insurers should clearly articulate what they are promising and then consistently deliver it. This requires building a flexible service operations model that delivers consistent service at a reasonable price. Since consumers are ultimately seeking peace of mind, the key is to avoid “negative moments of truth.” Our survey shows the level of risk resulting from negative service events is much greater than the benefits of positive ones.

Consistently delivering on a brand promise can quickly radiate and engender loyalty. Indeed, friends and relatives are the third most important source of information for shoppers, and highly satisfied consumers recommended their insurers three times more often than dissatisfied ones do. Similarly, 90 percent of those who trust their insurer would stay with it even if faced with a 10 percent price increase at renewal.

The power of recommendations

Few consumers recognize how important recommendations are when selecting a product, but they can be powerful determinants of choice. When shopping for health insurance, consumers accept recommendations 58 to 88 percent of the time, depending on the channel.

It’s not surprising that both the frequency with which a recommendation is offered in each channel and the impact varies widely. Recommendations generated by a Web site, for example, are delivered only 53 percent of the time and accepted by consumers only 58 percent of the time when they are delivered. Agents, on the other hand, make recommendations 78 percent of the time, and their recommendations are accepted 88 percent of the time. Given the complicated and emotional nature of the decision and the consumers’ desire for personalized advice, agents’ recommendations continue to be the most persuasive ones.

Although the Web continues to grow in importance as a source of information for consumers—more than half of consumers search online before making a purchase—it does not fare well as a stand-alone channel. Indeed, the Web delivers immediate information, including quotes, but it does not offer a purchase experience that meets the consumers’ emotional needs. Consumers who are considering purchasing health insurance actually make a purchase only 38 percent of the time on the Web, while 65 percent do so when going through in-person channels. Hence, online sales remain low—just 14 percent of consumers report purchasing on the Web. Further, only 1 to 2 percent of consumers purchasing through an agent would have preferred to purchase through another channel, while 9 to 13 percent of consumers who purchased online would have preferred to purchase through another channel—primarily in person.

Improving online sales will require clear recommendations, easier comparisons among options, consumer reviews, and more personalization. Insurers might take cues from Amazon.com, which provides recommendations based on a consumer’s unique searches. The Web provides a wealth of new opportunities for increasing the effectiveness of recommendations, such as endorsements or links to networking sites that discuss health insurance. Nearly a quarter of consumers say they would feel more secure with their purchase if they knew others in their situation had also purchased that plan, and 19 percent reported using social-networking sites to discuss their health-related needs.

Refine product choices

The consumers’ health care financing needs vary widely by life stage, but there are distinct segments within a life stage as well. Insurers must gain a more nuanced understanding of consumers, the risks they face, and how their concerns change over time—and then align their products accordingly.

Aligning with consumers’ exposures

Consumers aged 18 to 29 typically care more about dental and maternity coverage, while those aged 50 to 64 are often more concerned about coverage for major diseases and prescription drugs. A base product across these segments could be a stripped-down plan with salient features, such as catastrophic and preventive coverage, and could then be personalized to accommodate each customer’s unique needs.

A custom-built product design system—where services are added onto a basic plan based on the consumer’s specific needs—would allow insurers to bundle distinct product and service offerings in ways that meet the consumers’ real and perceived risks. Understanding and catering to those needs can enable companies to offer the right additional components to the base product at the moment when consumers are prepared to make a purchase.

Product design should also reflect consumers’ sensitivities to choice and cost trade-offs. For example, 57 percent of people with individual health insurance would be willing to give up some coverage choice in return for a premium discount of $40 a month. But fewer than 42 percent would be willing to accept a narrowing of retail pharmacy choices for a similar discount.

On the other hand, consumers are willing to pay for add-on features they perceive to be of value. For example, 35 percent of individually insured consumers would be willing to pay $10 a month for more time with their physicians. High-income consumers are willing to pay for disease management and remote support. These kinds of segment-tailored packages, which speak directly to consumers’ real and perceived concerns, should be sold as add-ons rather than as the standard features they are on many health plans. Since consumers are less sensitive about the prices of add-ons than with the price of the base product, this approach could have important pricing and margin implications.

Develop payment options

More than half of consumers are concerned about routine medical expenses today, and more than 60 percent are concerned about what those expenses will be when they are retired. Yet while health care premiums rank high among household expenses that must be paid, out-of-pocket health care expenses do not. This translates into poor collection rates and rising bad debt within the system—exacerbated by the current economic crisis—and a backlash in the retail market. Health insurers should address this pain point for consumers (and providers) by embedding simple payment solutions within product design.

Our research shows that most consumers are willing and able to pay their health care bills. On a per-visit basis, 83 percent of insured consumers are willing and able to pay less than $500, while 75 percent of insured consumers can absorb an annual expense of less than $1,000—enough to cover the bulk of routine health care. Even 40 percent of the uninsured, when presented with simple financing options, are willing and financially able to absorb annual liabilities of less than $1,000.

Health insurers should address concerns about paying health care bills with creative new products. Half of individually insured consumers, for example, would be willing to prepay their medical bills with credit or debit cards if they got a good-faith estimate in advance, and about half are willing to prepay without restrictions on the amount if they know the cost upfront. By integrating financing and credit options within individual product design—and simplifying the process with unambiguous patient statements—health insurers can capture new opportunities while addressing a major source of anxiety for consumers.

Engage consumers in managing their health

Consumers worry about their health care and the consequences of poor health. Yet concern does not translate into action: only 30 percent of people significantly worried about their health exercise regularly, abstain from smoking, and get routine physicals, and only 35 percent report having improved their health in the previous year.

It is difficult for people to close this gap. For example, consumers tend to favor immediate gratification (eating a doughnut) over future gains (staying fit)—whose benefits can sometimes be uncertain. But in a retail market, inspiring consumers to protect their own health is essential to delivering more affordable products, expanding margins, broadening the pool of attractive market segments, and improving the lifetime value of members.

Translate consumers’ health concerns into action

To transform consumer concern into action, health insurers can take several steps. First, they should intervene at the right time. Consumers tend to assess their situations in relative terms. Nearly two-thirds of consumers who are overweight or have other chronic or high-risk conditions, for example, rank their health as “good” or “excellent.” When their frame of reference changes, however, people become more willing to do something about their health. Immediately after a health event, consumers are significantly more open to addressing future risks and paying for services that address their health concerns. Consumers who have recently experienced a health event are 30 percent more likely to pay for advice and guidance on how to treat their condition, for instance. Behavioral science reveals that this window closes, however, as people become accustomed to their new situations.

Health insurers must engage the consumer while this window is open. By tracking the real-time occurrence of health events, for example, health insurers can better target members for enrollment in health-management programs. Retention is also important: more than three out of four consumers shop for new products upon experiencing a health event, and more than half purchase a new plan. Addressing the consumers’ health concerns at the time of an event could prevent this kind of membership loss.

Second, the way options are presented to consumers can have dramatic impact on their responses. We found that obese consumers, for example, are almost 30 percent more likely to be “extremely concerned” when told that they are “about twice as likely to die next year” (which focuses on the here-and-now implications of their behaviors) than when told that they are “considered obese by national health guidelines.” By appropriately framing risks—and solutions—to consumers, payors can help motivate behavior changes.

Third, in the face of difficult decisions, consumers typically turn to familiar sources of advice. Although consumers seek information from a wider variety of health information sources today, they are still most likely to take their physicians’ advice. For example, 92 percent of respondents directly followed the advice of their primary care physician at the point of care, citing trust as the main reason for not seeking alternative opinions. Yet there may be an untapped demand for additional guidance. Indeed, many consumers are open to other points of influence: 48 percent would be willing to get a second opinion if they received a call from a nurse at their insurance company. Insurers need to recognize the complicated and emotional nature of the choices consumers must make and actively work with trusted points of influence—physicians in particular—to drive healthy behavior.

Innovating to change behavior

Health insurers typically provide information and purely financial incentives, such as cash rewards, to help sustain behavior change. But the right incentives targeted at customer biases could motivate consumers to adopt and maintain healthier lifestyles.

Insurers who recognize the motivators of consumer activity can use even low-cost incentives to encourage interest in healthier behavior and leverage them to drive better outcomes. For example, consumers are attracted to probabilistic rewards such as lotteries. When well designed, such incentives can change behavior more effectively than direct cash payments: consumers tend to be overoptimistic about winning, and lotteries offer the right level of variable reinforcement that helps consumers sustain motivation over time.

We recently tested these kinds of behaviorally based incentives using a “regret lottery” design. The goal was to get employees to complete a health risk assessment. Employees were divided into small teams and then enrolled in a weekly lottery. Members of the winning team received a large prize, but only if they had completed the assessment. Winners were widely publicized, playing off of individuals’ anticipated regret at missing their chance of winning the big prize the week their team was selected.

The result was 69 percent completion of health risk assessments in the regret lottery pilot, compared with 43 percent for those that received direct-cash incentives. And, because the expected payout of the lottery condition was equivalent to the cash incentive, the regret lottery was a more effective use of incentive dollars—it would have been significantly more expensive to achieve the same penetration rate using the direct-cash incentive since in the lottery condition only a handful of individuals won each week.

Health insurers should use such insights to change behaviors. Six out of ten high-health-risk consumers, for example, express interest in lotteries—significantly more than direct-cash incentives—as an incentive for engaging in healthy behavior. Similarly, most consumers want to be rewarded for achieving results: about 60 percent of individually insured consumers are interested in discounts for achieving health goals. Many are also willing to accept penalties for failure: 40 percent are interested in products that penalize failure to meet those goals. This suggests that incentive programs such as deposit contracts—where consumers commit themselves to changing their behavior by paying money up front, earn rewards for sticking with the program, and agree to penalties if they don’t comply—can help inspire consumers to change behavior.

For leading health insurers accustomed to competing mainly in an employer environment, gaining deeper insights into the needs and biases embedded in the typical consumer’s behavior will be essential for creating and distributing effective products, earning the consumers’ trust, providing a more satisfying shopping experience, and, ultimately, helping consumers better manage their health. In short, the successful insurers will be those whose business systems can deliver effectively the peace of mind health care consumers desire.