Insurers have a productivity challenge. Recent McKinsey research found the insurance industry has struggled for years to achieve productivity gains at scale, particularly compared with other industries. In addition, the spread in operating costs between the highest and lowest performers in both P&C and life has substantially increased over the past decade.

While four categories of levers—functional excellence, structural simplification, business transformation, and enterprise agility—can support productivity efforts, insurers typically focus on the first two. And indeed, those levers form the foundation of efficient and effective operations, so they can hardly be leapfrogged.

However, more potential can be realized. As technological advancement and customer expectations evolve dramatically, traditional industry borders are falling away. Ecosystems—interconnected sets of services in a single integrated experience—have emerged across industries, as have platforms that connect offerings from cross-industry players.

For insurers, tapping into an ecosystem offers the opportunity to embed their insurance products into seamless customer journeys. In today’s interconnected world, embracing ecosystems is of paramount importance to address the customer in the moment of need, whether it be fostering direct customer relationships or integrating with organizations that own the customer interface.

How ecosystems support an overall productivity strategy

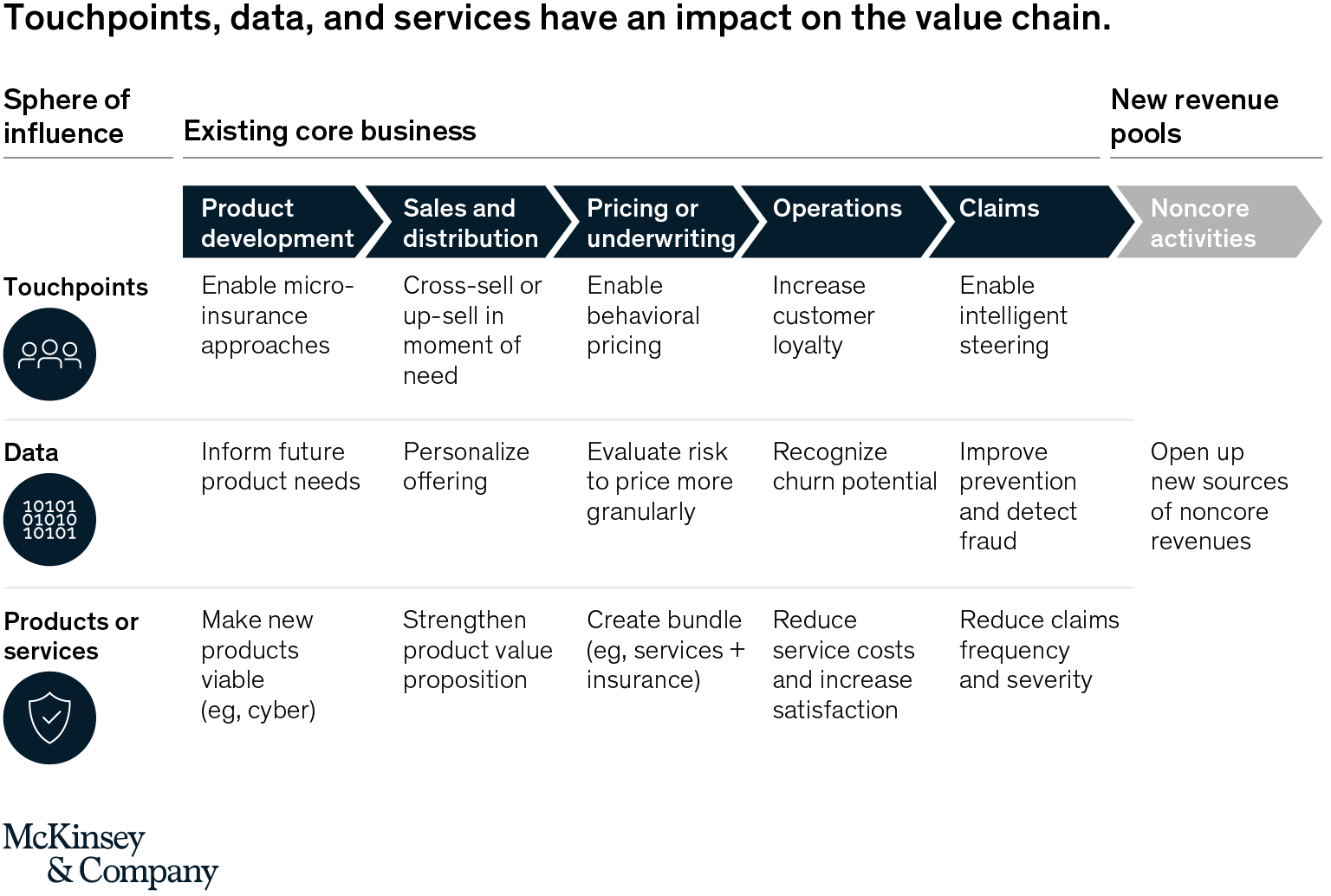

Ecosystems have the potential to open new revenue streams for insurers. The substantially larger benefit, however, may come from contributions through touchpoints along the insurance value chain, data on the customer’s preferences and activities, or the services themselves (exhibit). Such an ecosystem approach can help generate new leads, lower distribution costs, increase customer retention, and improve prevention and assistance to reduce claims.

Various insurers are demonstrating first indications of an ecosystem strategy’s positive impact. For example, Ping An’s online car-purchasing platform, Autohome, draws more than 38 million unique visitors a day, generating one-third of customer leads for the insurer’s P&C and financial services businesses. South African insurer Discovery has shown that users of its health-and-wellness-management platform have 28 percent fewer hospital stays and 10 percent fewer chronic conditions, likely because of a combination of selection effects and actual behavior change.

What do insurers need to do to succeed?

Many insurers still struggle to measure and generate value from their ecosystem efforts. To be successful, insurers need to define their strategic goals: where they want to play, based on their current brand positioning and existing assets, and what parts of the value chain they want to strengthen. Some may decide to build up a comprehensive service landscape, while others may focus on integrating their insurance offerings into existing customer journeys. In both cases, insurers need to invest in their technological and organizational capabilities.

On the technology side, insurers should build up scalable and flexible API-based IT architectures that support quick integration of offerings into seamless customer journeys. Moreover, data-management and analytics capabilities can help carriers take advantage of new touchpoints and data.

On the organization side, investments should focus on partner-management capabilities, digital agility to support services, and a consistent cross-channel experience. Legal structures that allow linking the different offerings (particularly in the context of non-insurance business) are also a must.

As speed and scalability are the fundamental ingredients of the game, insurers need to find a manageable mixture between making, buying, and partnering. While building up services may fill gaps in the market, partnerships and acquisitions can provide insurers with the flexibility to rely on innovative services and talent from other industries. In all cases, insurers should play out the “parenting advantage”—using their own resources to create new offerings better than their rivals—by drawing on customer and data assets and capabilities to develop services or attract partners wherever feasible.

Over the next decade, ecosystems will become central for insurers. Now is the time for insurers to lay out their strategies and visions and select use cases based on customer value. Above all, they must focus on the available productivity levers more comprehensively. Doing so will not only improve performance but also lay a solid foundation for generating value through ecosystems.

The authors wish to thank Patrick Löffler, Jahnavi Nandan, Shirish Sharma and Ulrike Vogelgesang for their contributions to this blog post.