The economic rise of Asia has been much noted. But many have not realized that this is not just a story about the emerging giants, India and China. Countries that are a part of the Association of Southeast Asian Nations (ASEAN) are also an important contributor to Asia’s growth.1 By 2009, this region already accounted for 9 percent of Asian wholesale banking revenues and 13 percent of capital markets and investment-banking (CMIB) revenues. To be sure, these are not dominant positions. But several key ASEAN economies will grow faster than the rest of Asia over the next five years. GDP growth in Vietnam (7 percent), Indonesia (6 percent), and Malaysia (5 percent) will be notably faster than in the established markets of Japan (2 percent) and Australia (3 percent).2

Several forces are propelling ASEAN growth. Chief among these are the need for new roads, ports, and power plants, and governments’ determination to expand capital markets. Evidence of both was seen in the announcement at the July 2010 ASEAN summit in Hanoi of a plan for road and rail development across the region. ASEAN’s brightening star will likely attract yet more investment from global banking majors, many of which have already built formidable presences across the region. For local banks, an inflection point is at hand. As Asian companies expand into new regions and the largest go global, incumbent banks will need to redouble their efforts or risk losing a substantial share of their investment-banking franchise to the big international banks. We see five core capabilities that local banks must build, including the coverage model, account planning, research, cross-border capabilities, and the talent proposition.

A leading incumbent bank in India set out to build these five capabilities, with considerable success: among other achievements, average monthly fee income increased by 125 percent over baseline. Several ASEAN banks will probably achieve similar success, and that in turn will increase the pressure on foreign banks to respond. We see three likely responses for these global firms, including balancing their “footprint,” capturing the midcorporate opportunity, and developing capabilities to deliver cross-cutting customer solutions.

Opportunity beckons

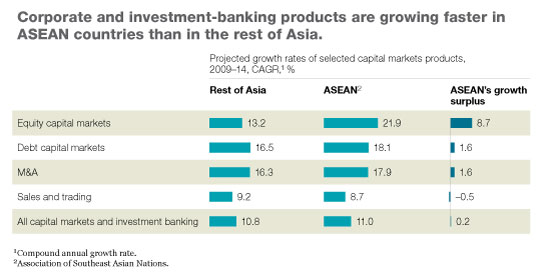

McKinsey’s Global Banking Profit Pools estimates 2009 revenues from CMIB in the ASEAN region at $7.4 billion.3 Notably, CMIB accounted for 28 percent of all wholesale banking revenues in ASEAN, compared with 19 percent for Asia as a whole. This greater reliance on capital markets is a sign of greater sophistication in ASEAN (Exhibit 1).

We focused our research on five of the biggest ASEAN banking sectors (Indonesia, Malaysia, Singapore, Thailand, and Vietnam). All except Vietnam have a higher proportion of CMIB revenues than would be indicated by their GDP per capita. This implies that for a given amount of capital, banks may enjoy greater revenues from CMIB products than from lending. Not surprisingly, the region has proved attractive to global banks that traditionally focus on fee-based businesses. Many of these foreign banks have already built leading franchises in several products and countries.

These banks also find the growth of CMIB in ASEAN attractive. The region is projected to grow faster than the rest of Asia in the key areas of equity and debt capital markets (ECM and DCM) and mergers and acquisitions (M&A) (Exhibit 2).

Skeptics would counter that, for all its attractions, “investment-banking in ASEAN” really means “investment-banking in Singapore.” It is true that Singapore currently accounts for over two-thirds of total ASEAN CMIB revenues. However, the city-state’s share is projected to decline to around 58 percent by 2014 as capital markets in other economies develop.

Similarly, at present, CMIB in ASEAN is heavily focused on sales and trading, which generates over 80 percent of revenues. Again, we expect to see a growing diversification. By 2014, sales and trading will account for 72 percent of revenues.

Sources of growth

We see five major trends propelling growth in ASEAN and shaping the evolution of CMIB markets.

1. Infrastructure investment

Infrastructure has been a big source of growth for much of Asia, including ASEAN, and that looks set to continue. For CMIB, that will mean healthy developments in debt capital markets and syndicated loans, as well as in structured fixed-income products designed to attract funding from overseas investors.

Over the next five years, the ASEAN region is expected to spend more than $350 billion on infrastructure. Indonesia, Thailand, and Vietnam will commit the biggest sums, while Singapore is expected to spend little. Indonesia will look to address a lack of quality roads, inadequate power supply, and a dearth of public transport. In 2009, the newly elected government announced that the total infrastructure spend needed between 2009 and 2014 will be around $140 billion. Much of this investment may be structured as sukuk, a bond-like instrument that conforms with Islamic law. (For more on sukuk, see sidebar “Sukuk in Malaysia and Indonesia.”)

In Thailand, infrastructure spending has lagged in recent years. While GDP grew at over 8 percent between 1999 and 2008, infrastructure spending grew at only 3.6 percent. From 1999 to 2008, infrastructure spending as a share of GDP fell from over 9 percent to about 6 percent.

Like Indonesia, much of Vietnam currently lacks reliable electricity, quality roads, or seaports. Its infrastructure requirements are estimated at $70 billion to $80 billion over the next five to ten years. Today most of its infrastructure investment is funded by government debt. That is expected to change, as the government begins to seek investors to form public-private partnerships.

2. Government support for capital markets

We see two thrusts by governments as they seek to strengthen capital markets in the ASEAN region. On one hand, developed-market governments are trying to create financial centers (as in Malaysia) or strengthen them (as in Singapore). While Singapore is succeeding in attracting hedge funds and private banking players, Malaysia seeks to become a global hub for innovation in Islamic finance through the Malaysia International Financial Centre (MIFC) in Kuala Lumpur.

On the other hand, governments in developing markets like Indonesia and Vietnam are taking initiatives to expand markets and improve trading and settlement infrastructure.

Vietnam currently has a growing primary bond market with mainly public-sector issuances, but a thin secondary market. The government is addressing this; first, it has established a specialized secondary state bond market where most government securities are now traded. It also intends to build a benchmark yield curve and to encourage the creation of credit-rating companies. Finally, it is also installing a securities depository and a new settlement system with support from the Asian Development Bank (ADB) and the World Bank.

In Indonesia, the government has also taken the assistance of the ADB, in the form of an ongoing technical-assistance program. The goal is to build deeper and more liquid capital markets, enhance market supervision, and improve regulatory resources and capacity.

3. Expanding horizons for ASEAN companies

As ASEAN companies continue to grow, they will be tempted to look outside their home markets for growth. Already, about 40 percent to 60 percent of ASEAN M&A is cross-border deals, and more than a third of these are within the region. As companies outgrow their markets and become comfortable with international expansion, investment banks will see increased opportunities in M&A advisory and acquisition financing. Three sectors that illustrate this trend well are financial services, telecom, and energy and natural resources.

In financial services, almost all the leading banks in Singapore and Malaysia have made regional forays to expand their presence in ASEAN. These banks have achieved varying degrees of success. Among the most successful is Malaysia’s CIMB Group, which has gone through five transformational deals in four years, taking the bank into new markets in Thailand, Indonesia, and Singapore.

Several ASEAN telecommunications firms have adopted a similar growth strategy. SingTel, for instance, is now active in over 20 markets and has acquired strategic stakes in AIS in Thailand, Telkomsel in Indonesia, and Globe Telecom in Philippines.

In energy and natural resources, Indonesia in particular has seen significant M&A activity—about 130 transactions in the past eight years—originated by both domestic and overseas firms.

4. Indonesia and Vietnam coming to the fore

Forecasts of real GDP growth in ASEAN to 2050 suggest that most of the growth will come from Indonesia and Vietnam. As mentioned, these countries will benefit from government actions to improve capital markets and from the push to build new roads, power plants, and seaports. But there are other forces at work. Both countries will see broad-based economic reforms and strong growth in manufacturing. And both will benefit from a young and rapidly growing labor force as well as improved political stability.

CMIB revenues will mirror the growth in GDP. ECM in particular will prosper from a wave of local listings in both markets. In Vietnam, the government has already privatized several good-size state-owned enterprises (SOEs) and has announced plans to privatize some of the biggest, including AgriBank, Bao Viet Insurance, Vinatex, and Vietnam Airlines. Similarly, in Indonesia, following the successful listing of Bank Tabungan in 2009, the government has announced plans to divest stakes in some of the largest SOEs, including PT Krakatau Steel, Plantation Company PT Perkebunan Nusantara (PTPN) VII, and Garuda Indonesia.

M&A advisory will also benefit, as fragmented local industries are expected to consolidate. Indonesia has more than 120 banks, of which 4 are state owned. That’s many more than in mature markets such as Australia and India. Vietnam is similarly overbanked. The State Bank of Vietnam has mandated that all banks in Vietnam must have capital of at least 3 trillion Vietnamese ng (about $150 million) by the end of 2010. Many of the smaller banks will likely be unable to raise the requisite capital, and a forced consolidation of the sector may result.

5. Growing sophistication of customers

As ASEAN economies mature, capital markets are likely to see increased demand for more sophisticated products and services. As ASEAN companies grow, it is likely they will begin to tap into corporate bond markets and rely less on traditional bank borrowing, a path taken by maturing economies in the past. Banks will likely have incentives to help them do this, given the global regulatory push for bigger capital buffers and more liquidity. Southeast Asian companies are also likely to continue looking for customized currency and commodity hedges against price fluctuations.

Sales and trading businesses will also need more sophisticated products. As the ASEAN economies accumulate wealth, consumers will turn to life insurance and asset management. There is considerable room for these businesses to grow. The rise of insurance will create a kind of virtuous cycle, creating opportunity for institutional sales and trading firms that will be asked to deliver the kinds of sophisticated products (such as swaps, options, and other derivatives) that their counterparts in developed markets have sold for years.

Of course, all of Asia is expected to grow in affluence; assets under management of high-net-worth individuals are likely to rise to nearly $7.5 trillion by 2012. With interest rates low in Asia, as in the rest of the world, Asia’s private banking and affluent retail customers are likely to seek ever higher returns along with portfolio diversification, and will aggressively pursue investments such as initial public offerings, structured equity-linked products, and alternative investments such as hedge funds. This infusion of new money into equity-linked instruments will push up sales and trading revenues.

Five core capabilities

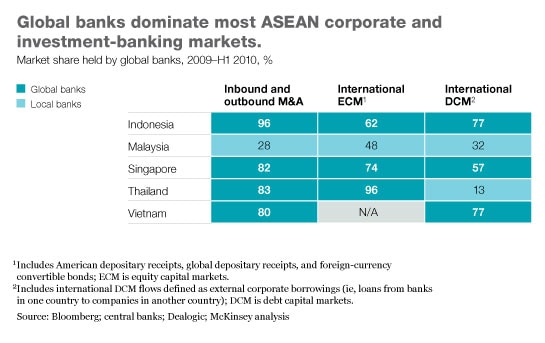

In recent years, local and foreign banks have competed vigorously to position themselves for the coming opportunity. The current state of play of CMIB markets is shown in Exhibit 3.

Despite the opportunity, some local institutions seem to be ceding the advantage in many of these markets to others. These firms are at risk of missing out on the next big wave of growth in ASEAN capital markets. To avoid that fate, they can draw on the examples of their emerging-market peers (for example, Kotak in India and Itaú BBA in Brazil), which have leveraged their balance sheets to build dominant local investment-banking businesses. In our view, local commercial and corporate banks must take five actions to succeed in investment banking:

1. Strengthen client coverage to encompass the capital markets opportunity

In our experience, banks use one of three approaches to client coverage, defined by the role of the person at the client interface. The relationship manager (RM) acts as the single point of contact with the client in the RM-led model, occasionally calling on product specialists for expertise. The RM establishes and manages the relationship with the client’s CEO or CFO in the client-service-team-led model, an emerging trend. The RM then coordinates all account-related activities of the client service team, which consists mainly of product specialists. Team members establish links and coordinate activities with their client counterparts. Finally, in a product specialist model, senior bankers and product specialists establish coverage independently.

Within investment-banking teams and products, banks align the coverage model with their understanding of the various segments of their client base. The most commonly observed model is a segmentation based on size; the coverage model is then tailored for each tier of clients. An alternative choice we see in smaller investment-banking houses is an alignment of coverage teams to sectors. Here the proposition is the coverage teams’ depth of product and sector understanding.

Wholesale banks choose the coverage model based on three criteria that reflect their stage of growth: the availability of sophisticated RMs and product specialists, the cost of coverage, and the feasibility of establishing coordination mechanisms among different product groups. There is no “right” model, and each player must tailor its coverage model based on its starting position, underlying market characteristics, growth aspirations, and manpower availability.

2. Tighten up the account-planning process

The three objectives of disciplined account planning are to ensure that the bank can increase client satisfaction through tailored offerings that address the client’s needs, to improve the bank’s profitability per client, and to increase the time spent by salespeople on selling to the right set of clients.

In investment-banking, we typically encounter six barriers that stand in the way of disciplined account planning. Three are behavioral problems: unwillingness on the part of RMs and other sales staff to commit time, a reluctance to share client-related information, and a bias against the current IT system and tools. Three problems have to do with poor processes: little understanding of the most and least profitable clients, a lack of clarity on roles and responsibilities in the client coverage team, and an absence of accountability and incentives.

A structured approach can be used to overcome these barriers and increase the effectiveness of account planning to maximize profitability per client, make salespeople more effective, and increase customer satisfaction.

3. Build research capabilities

The credibility and independence of the research function in investment banks was significantly tested during the dot-com shakeout in the first half of the decade. In response, a number of banks have worked hard to strengthen the independence of the research function and enhance transparency. Strong research capabilities are emerging as a critical success factor. Across markets, a strong position in league tables usually goes hand in hand with robust research capabilities.

Banks can start by identifying how best to meet increasingly sophisticated customer requirements. Many customers are building in-house capabilities and have consequently moved away from traditional research products (for example, PDF reports distributed via e-mail, containing the latest information on specific stocks). They are increasingly demanding “research services”—such as conversations, meetings, or analyst-introduced access to management. In response, many global players are rethinking their approach to research. HSBC has dropped two of its research product offerings—its “buy, sell, hold” recommendations and maintenance research—while increasing its analyst head count to support more in-depth analysis and customer contact. Similarly, some banks have experimentally outsourced maintenance research to specialists, while keeping sector experts, quantitative analysts, and strategists in-house.

In building a research organization, banks need to consider the growing sophistication of most of their core customer segments: affluent/high net worth, domestic institutional investors, mass retail, and, of course, foreign institutional investors. Distinctive research capabilities for the right segment, as part of a full-service offering, can lead to an increased share in sales and trading as well as ECM. Similarly, ECM is linked to M&A advisory for large deals that need to be financed through capital market issuances.

4. Gear up for the cross-border opportunity

As ASEAN companies expand internationally, local banks will need to think through how best to meet their needs. For a few banks, it may be best to focus exclusively on the domestic market. But many will decide to follow their clientele and build capabilities to serve them in their expansion.

Several local investment banks have built ties with global firms (for example, SCB Securities with Goldman Sachs and Phatra Securities with Merrill Lynch/Bank of America). The typical approach involves the local player using the partnership to build up capabilities over time, while the foreign partner accrues local market understanding and develops local relationships and brand equity. After time, when both parties have reaped the benefits of the alliance, it is often terminated and both partners go their separate ways, as Kotak and Goldman Sachs did in 2006.

An alternative approach is to establish alliances with local boutique firms with experience in cross-border deals. As an example, Avendus in India has partnered with Goetz Partners for India-Europe deals, while Kotak has an alliance with GCA Savvian for India-Japan deals. In the latter case, the alliance seeks to advise Indian and Japanese companies on cross-border mergers and acquisitions. Thus, clients of GCA Savvian in Japan can seek out acquisition targets in a high-growth market such as India with the help of local expert Kotak.

5. Adopt the right “people strategy”

The people strategy—the bank’s approach to compensation, its talent proposition, its recruitment model, and its retention practices—lies at the heart of building a successful investment bank. The current overhaul of regulations will have considerable impact on banks’ compensation practices. Banks will need to decide on the right mix between current and deferred compensation, and, in performance measurement, between current financial metrics or longer-term health-related metrics.

Commercial banks looking to build an investment-banking business also have to tackle the particularly acute challenge of integrating radically different performance and incentive systems. While banks have tried several approaches, our experience suggests that an approach that builds on the principles of the “one firm” model is likely to be successful. At its core, this approach ties most incentives to the overall performance of the firm as opposed to purely individual performance and contribution. Implementing this model involves instilling a culture that encourages people to work toward building the firm.

In addition to creating the right performance culture, banks will also need to develop other elements of the people strategy by designing a clear employee value proposition, a recruitment model that balances lateral and fresh hires, and an effective retention strategy.

Three moves for foreign banks

Foreign banks should not take their current dominance of many products and markets for granted. Western banks that want to secure and expand their share of the ASEAN opportunity should consider three core actions.

Effectively balance local and regional operations

Several global players have opted for a centralized approach, addressing opportunities throughout ASEAN from their offices in money centers such as Singapore and Hong Kong. Others have started this way but have expanded their presence in select geographies such as Thailand and Malaysia through their wealth-management and brokering arms; still, they remain more or less centralized. These approaches have been adequate up to now, during a period when the vast majority of deals were originated by multinationals and large corporates, which naturally turn to the global majors, either from long-standing relationships or to tap their deep product expertise.

In coming years, however, the centralized approach might no longer work. We see two major trends that will weaken the effectiveness of banks that try to cover the region from a strong center. One is greater local competition. As ASEAN capital markets deepen, local players will expand their investment-banking capabilities, given the positive impact on return on equity. Second, as noted above, a broader base of corporations will start to seek investment-banking advice. Often these will be smaller companies with no history with the global banks. Local institutions with upgraded capabilities will be in prime position to capture a greater share of this business, given their scale of operations. As an example, in Russia, local firm Renaissance has nearly 150 bankers, while the bulge-bracket firms have on average only 20 to 30. By virtue of its broader and deeper coverage, Renaissance has been able to provide superior client service and claim a greater market share.

Capture the midcorporate opportunity

As ASEAN markets develop, a broader base of corporates will have investment-banking needs, and over time, they will form a larger portion of the fee pool. To capture an outsize share of these fees, foreign banks will have to do three things.

First, this segment has traditionally been served by local incumbents, which have typically held lending relationships and which now seek to build their own investment-banking capabilities. Foreign firms cannot easily replicate this approach: they do not have a natural “entry product,” and so will need to invest in developing relationships over time. This will require a local presence.

Second, given the smaller deals and lower fees that these midsize companies will generate, many foreign banks will have to modify their cost structures if they are to generate attractive returns on equity.

Finally, foreign firms will have to find ways to inspire their bankers to work on midcorporate deals, likely by offering incentives to lure them away from the attractions of large deals. If this does not seem likely to work, firms should consider establishing a separate group, operating under a different set of economics, to cover this segment.

Serve cross-cutting needs

Local companies are likely to start asking for solutions that cut across wholesale funding and capital market products—for example, some companies are likely to need structured finance for infrastructure projects as well as sukuk. To deliver on these multifaceted needs, global firms should establish local-currency balance sheets to more effectively structure deals. Firms organized in product groups will need to develop mechanisms and incentives to link organizational “silos” (especially DCM, corporate banking, and Islamic banking) to create effective client solutions.

Throughout the ASEAN region, opportunities abound in capital markets and investment-banking. But banks will have to examine them carefully and consider the trends shaping their growth.