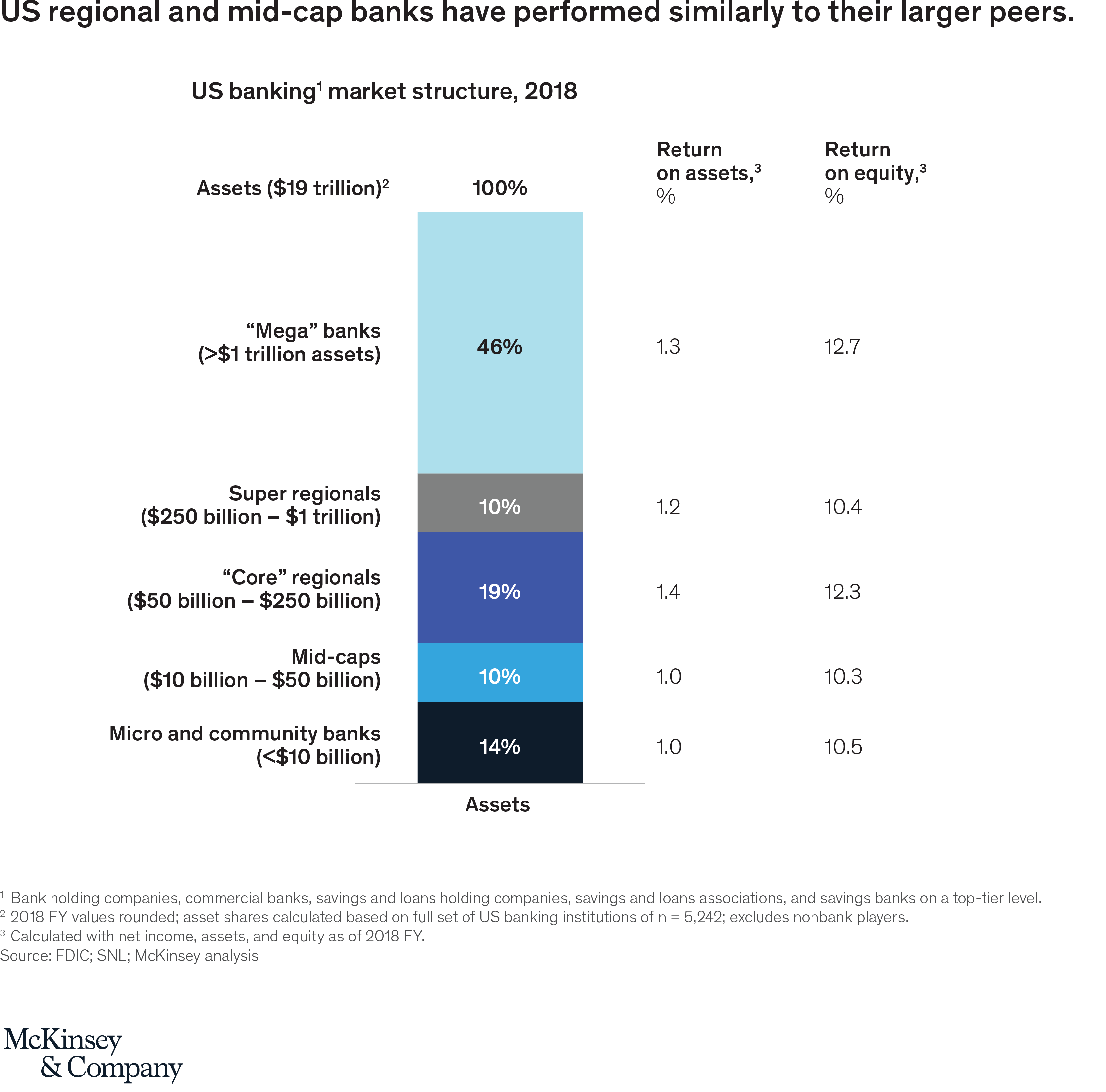

The past decade has been relatively benign for US banks, including the regional and midcap banks that account for almost 30 percent of the country’s banking assets. As overall performance in the last few years has returned to a level similar to the long-term average of the roughly 20 years before the financial crisis, regionals and midcaps have kept pace with their larger competitors in terms of return on assets and return on equity (Exhibit 1). However, this may become more difficult, as significant headwinds are rising for this group of banks.

First, macroeconomic conditions are becoming more challenging worldwide. Growth is slowing, interest rates are declining—putting pressure on net interest margins—and there is significant geopolitical uncertainty. Add to that the threat of a recession and likely resultant credit losses.

Second, consumer behaviors are changing, shaped by their experiences with leaders across industries. And digital disruption—led by attacker banks, fintechs, incumbents, and big tech firms —has progressed to the point where switching banks is easy for customers, giving them the power to unbundle their banking relationship. Competition for each product in a customer’s wallet could ramp up, increasing price transparency and raising the potential for banks to be disintermediated and relegated to balance-sheet providers with low returns on equity.

Third, advanced analytics and artificial intelligence are becoming core differentiators, leading to lower costs and better customer experience delivery for players with the scale to make meaningful investments. These investments will result in increasingly sophisticated customer experiences, including personalized interactions and tailored value propositions, as well as significant opportunities for efficiency through automation (our research indicates that about 23 percent of current work activities across sectors could be automated by 2030). Leading banks are experimenting with use cases such as AI-powered chatbots, deep learning for signature analysis in fraud management, and dynamic next-product-to-buy models. And the scope of use cases is likely to expand dramatically over the next ten years.

Fourth, the technology arms race continues to intensify, as large banks make substantial investments in technology and large tech platform firms start moving into financial services. Mega banks are leveraging their scale—both investment dollars and volume of customer data—to make significant investments and attract high-quality tech talent, increasing the gap between the leaders and laggards.

Fifth, a changing regulatory landscape could make select areas more challenging for smaller banks over time, particularly in the cybersecurity arena, which is likely to see increased focus from regulators. Many regional banks will need to continue investing substantially to manage risks effectively.

These factors will continue to drive consolidation, and only the nimblest regional banks will survive intact. To do so, they will need to rethink their operating models with the aim of achieving efficiency ratios below 50 percent (with a clear path to continued reductions), significant and sustainable sources of low-cost funding, meaningfully better customer experience, a compelling talent value proposition, and a rapid and flexible approach to operational changes.

Playing to their strengths

Despite the challenging outlook, regional and midcap banks have meaningful strengths: close connections to customers, the ability to pursue high-value niche markets and segments, and relatively rapid decision-making. Our “strategic control map” analysis of banking valuations in the US shows that the market expects a leading pack of regional banks to considerably outperform their larger peers over the next several years (Exhibit 2).

In our view, US regional banking leaders should focus on the following six areas as they shape their strategy and their response to potential mega bank dominance:

1. Focus on where the bank has a “right to win” and optimize the rest

The days of being all things to all people are over for most regional banks. Most do not have a differentiated strategy that will win over time. Many banks pursue a community-oriented strategy, but our research suggests that community connection is not a major factor in determining where people bank, and the importance of local branch presence has been steadily declining. In fact, banks that have focused on building a segment niche or driving productivity in a disciplined way have been rewarded by the market with price-to-book ratios roughly 20 percent higher than those of their peers.

Most regional banks need to take a hard look at where they can actually win, and prioritize those areas where they have a unique ability to compete. For many, this could mean shifting resources away from mass market consumers towards relationship-oriented businesses like commercial or private banking.

Several banks have been rewarded by the market for doubling down and developing a sustainable competitive advantage in one specific cluster, industry, or segment niche. These banks invest disproportionately in growing their target segment with differentiated products, sales, marketing, and operations, and develop deep networking effects by serving several types of players in the same cluster to protect their margins. For example, some banks have delivered a significantly higher growth rates than their peers by targeting the startup, venture capital, private equity, and investor cluster.

Of course, success in a niche approach is also dependent on choosing the right segment. Some of the lowest-performing banks are those that have chosen segments that did not grow as expected, or which were buffeted by greater economic headwinds.

Banks seeking to adopt a targeted segment posture should start by taking candid stock of their strengths and weaknesses, examining the opportunities in the market, and purposefully orienting management attention, operating model, and investments to succeed in that segment.

2. Ensure a sustainable low-cost funding source

Many US regional banks are not growing low-cost deposits at a rate that will sustain them. As our recent research indicates, the relationship between branch network and deposit share is breaking down (Exhibit 3). Today, growth in deposits is more closely correlated with a bank’s ability to gain customer mindshare. Banks with strong customer mindshare provide a set of products, services, functions, and access that encourage engagement between a bank and its customers. These banks excel in terms of digital maturity (the extent and sophistication of a bank’s web and mobile capabilities), share of voice (the level of a bank’s representation in advertising and marketing in specific markets), and customer experience (the ability to fulfill customers’ expectations of service, within and across all channels)—in addition to physical footprint. Larger banks with superior marketing budgets and digital capabilities are increasingly winning the war for deposits as a result: approximately 45 percent of new primary banking relationships are with the mega banks, even as they account for less than 20 percent of branches.

Any regional bank’s strategy must address deposit growth by determining the current competitive position, gaps to fill, and likelihood of success. In many cases, this may require investing in new capabilities to win in deposit-rich commercial verticals (e.g., professional services, title companies) or in the small business arena, by sharpening the conventional value proposition and building new digital infrastructure (as some European banks have recently done). The threats and opportunities presented by digital deposit attacker models have to be carefully weighed as well.

3. Build a scalable, efficient model

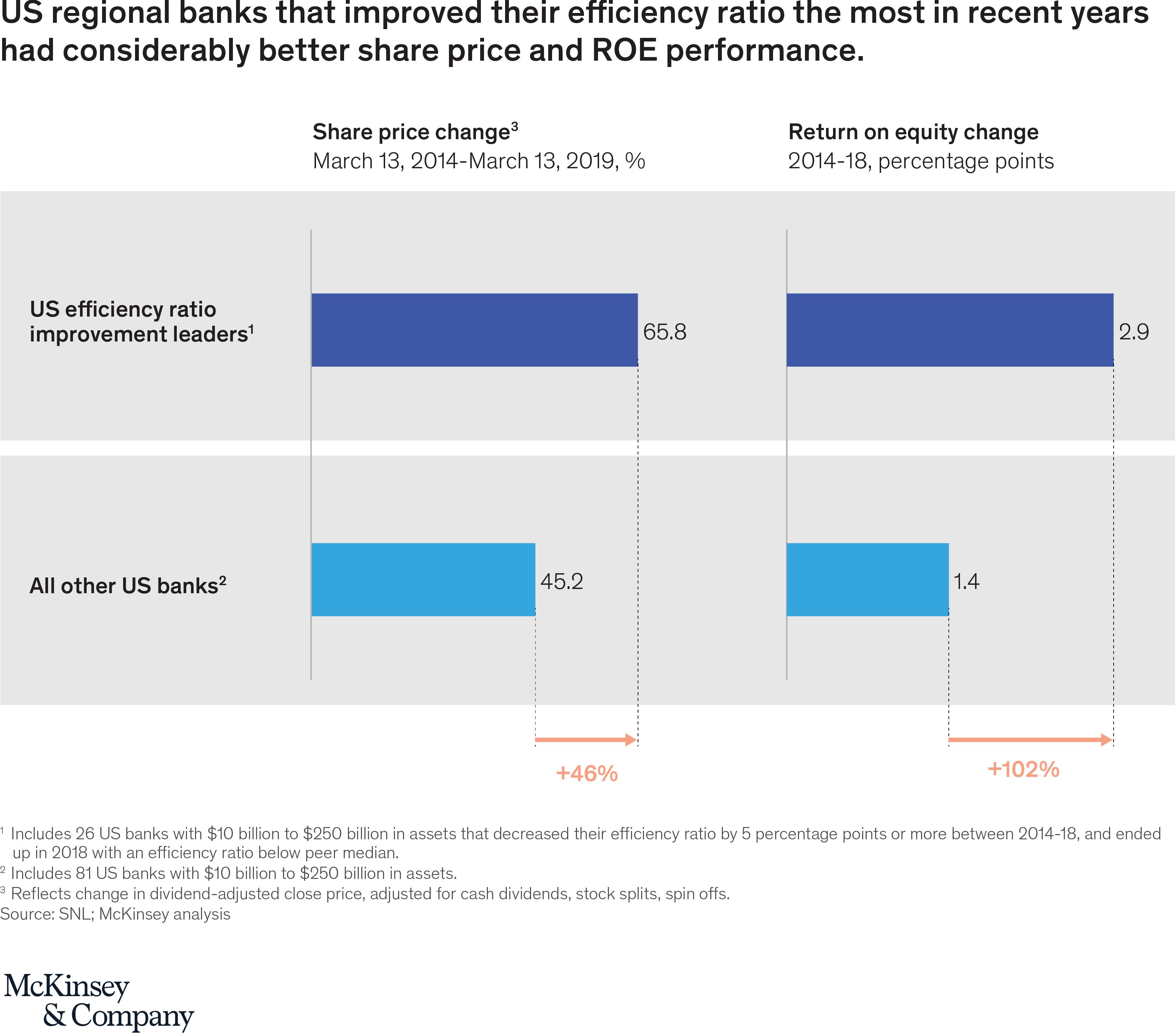

Leading players have a relentless focus on improving productivity in all parts of the bank, deepening relationships with existing clients, and maximizing the return on their current assets. Those who have succeeded in these areas in recent years have been highly rewarded by the market, achieving a median price-to-tangible-book-value of 1.9x compared to 1.6x for median regional peers. Productivity leaders have also achieved a roughly 50 percent higher share price appreciation and about two times higher ROE improvement over the last four years compared to their less productive peers (Exhibit 4).

Many banks that have grown through acquisitions have accumulated broken processes and inefficiencies over the years. To deliver leading customer experience and achieve top-level efficiency, these banks need a scalable model built around a simple structure, a focus on performance management, and redesigned processes (e.g., credit) that leverage demand elimination, digitization, and automation. This allows banks to pursue acquisitions with a higher probability of positive returns to shareholders, and to achieve a lower overall cost structure.

Banks seeking to emphasize productivity start with a bank-wide transformation, designing the target state, identifying cost and revenue initiatives, and executing over 12 to 18 months. In most institutions there are substantial opportunities bank-wide: for example, improving the efficiency and customer experience of the credit function, optimizing the branch footprint, creating a value-focused procurement organization, boosting the effectiveness of the commercial and consumer sales forces, and increasing fee income (e.g., from treasury management).

Productivity leaders among banks develop a culture throughout the enterprise that sustains their advantage over time. In our experience, with the right commitment from the top, a typical bank can achieve a 7 to 10 percentage-point improvement in efficiency ratio over two years—enough to move from median to top-quintile. This improvement can free up significant capital for investment and lift the bank’s share price, unlocking opportunities for strategic M&A.

4. Develop a technology strategy to enable the business strategy

Core IT is increasingly a constraint on innovation and on how deeply costs can be cut for regional banks; and a robust core IT is also important for tapping into the next wave of efficiency improvements. Mega banks are making multibillion-dollar investments in digitizing customer journeys, automating the back office to improve speed and reduce costs, and making bets on next-gen functionality. Regional banks lack the resources to compete in all these areas—consider that one mega bank spent more on technology last year than all 59 US banks with $10 billion to $50 billion in assets combined.

Given this resource gap, US regional banks must carefully determine where to over-index and focus investment based on the specific strategy pursued. They also need to clarify their approach to partnerships with fintechs—as this may be one way to “leapfrog” larger competitors in certain capabilities. Regional banks need a plan for leveraging tools like cloud computing, scaling agile beyond select pockets in IT, and streamlining key customer journeys. In addition, they need to craft an approach to core technology modernization (choosing, for example, between big-bang core replacement, journey-led progressive modernization, and greenfield tech stacks) that best suits their overall business goals and the set of pain points they face—for example: cost profile, time to market, personalization, partnerships and innovation.

5. Hire talent for the future

Regional banks will need new skill sets to be successful over the next five years. They will need to hire, develop, and retain talent in critical functions, including data scientists, analytics translators, full-stack developers, UX/UI designers, and agile coaches. Compounding the challenge, many regional banks are facing a retirement “cliff” in key traditional roles (sales and senior management), increasing the urgency of staying relevant with younger potential talent.

A three-year talent aspiration based on each bank’s individual business strategy is needed, defining tangible talent milestones (and measurable objectives) along the way. A robust talent attraction, development (e.g., academy journey for key roles which have a supply/demand mismatch in the bank’s geography, peer coaching, chapter structure design), and retention plan to achieve the objectives is needed. Success will be heavily predicated on having the right talent. Thus, the challenge cannot be relegated to secondary priority status in HR, with annual reports back to the board. It must be led actively and jointly by the CEO, CHRO, and CFO.

6. Use M&A in a targeted way to accelerate scale

M&A has been a key driver of asset growth for US banks, with approximately one deal per business day over the last four years, amounting to about 840 deals and roughly $780 billion in acquired assets across the industry. Regional banks have accounted for the majority of deal volume and acquired assets across the industry. While the pace of M&A going forward is not certain, we believe that the banks that have executed on the above points and achieved higher multiples will be best positioned to leverage M&A successfully.

Our research across industries shows successful M&A practitioners follow several principles: First, they focus on deals worth less than 30 percent of their assets, and stick to one major deal per year. Second, they typically avoid smaller deals (that is, those below roughly 5 percent of assets), because they tend to absorb a disproportionate share of management attention and integration functions. Third, they emphasize acquisitions that build capabilities or support expansion to adjacent geographies. Fourth, divestments account for a sizeable share of transactions, as the bank reshapes its portfolio of assets towards strategic growth markets. Fifth, they capture value rapidly from M&A through a highly disciplined “integration engine”—including a playbook for front line, operations, and IT—that can capture a majority of the benefits for a major acquisition within six months and complete the integration within twelve.

Change in the US banking industry is likely to continue accelerating in the coming years. Regional and midcap banks that successfully address the six areas discussed here and craft a clearly-defined strategy for the evolving environment are much more likely to deliver above-average returns, weather the turbulence, and set themselves up for longer-term success.

The authors would like to thank Neil Smith for his contributions to this article.

For a PDF version of this article, click here.