Bank CIOs are facing a perfect storm. IT demands are escalating while pressures to keep costs down are intensifying, as banks cope with generally meager returns on equity. We believe that CIOs must look for ways to control costs through productivity gains in order to make room in their budgets for investments in critical tech-enabled changes and be true partners to the bank’s business side.

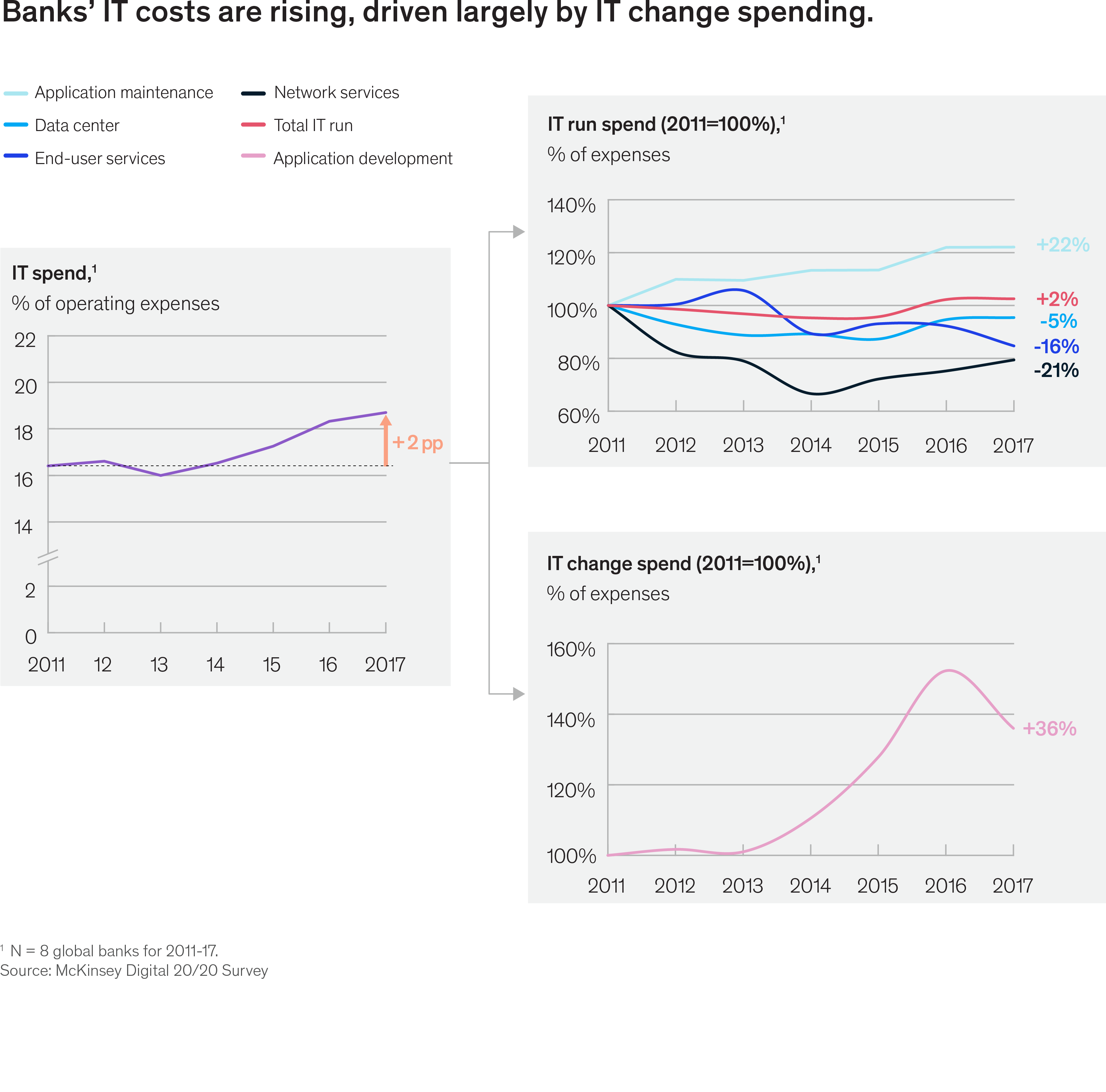

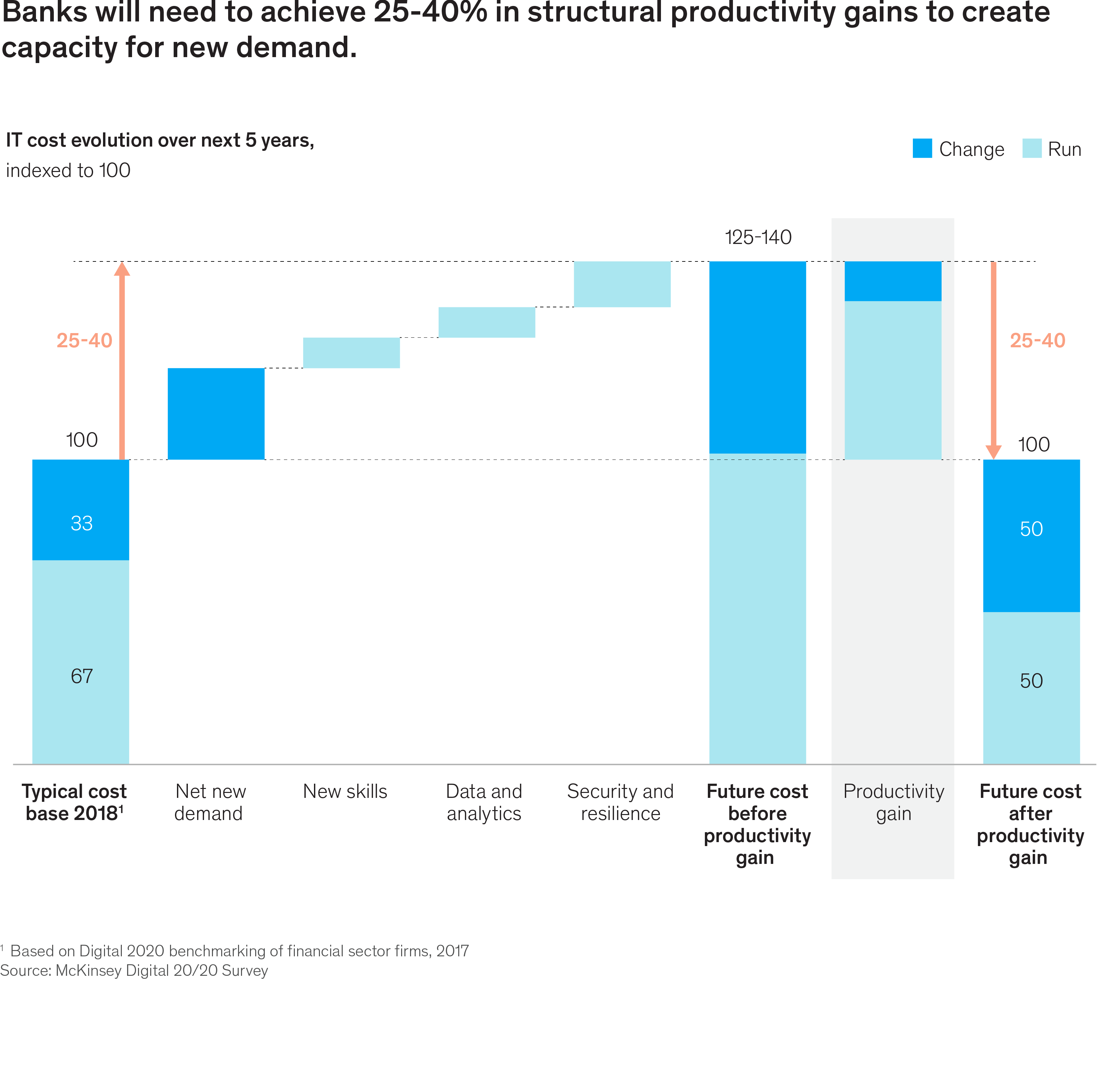

Historically, banks have offset some IT cost increases with productivity gains. A McKinsey Digital 20/20 survey of global banks showed that IT costs rose from 16.5 percent of expenses in 2014 to 18.5 percent in 2017. While run spending remained largely flat, change spending increased roughly 40 percent in the same period (Exhibit 1). But going forward we expect CIOs will need to improve productivity efforts considerably, aiming for structural productivity gains of 25 to 40 percent over the next five years just to keep costs flat (Exhibit 2).

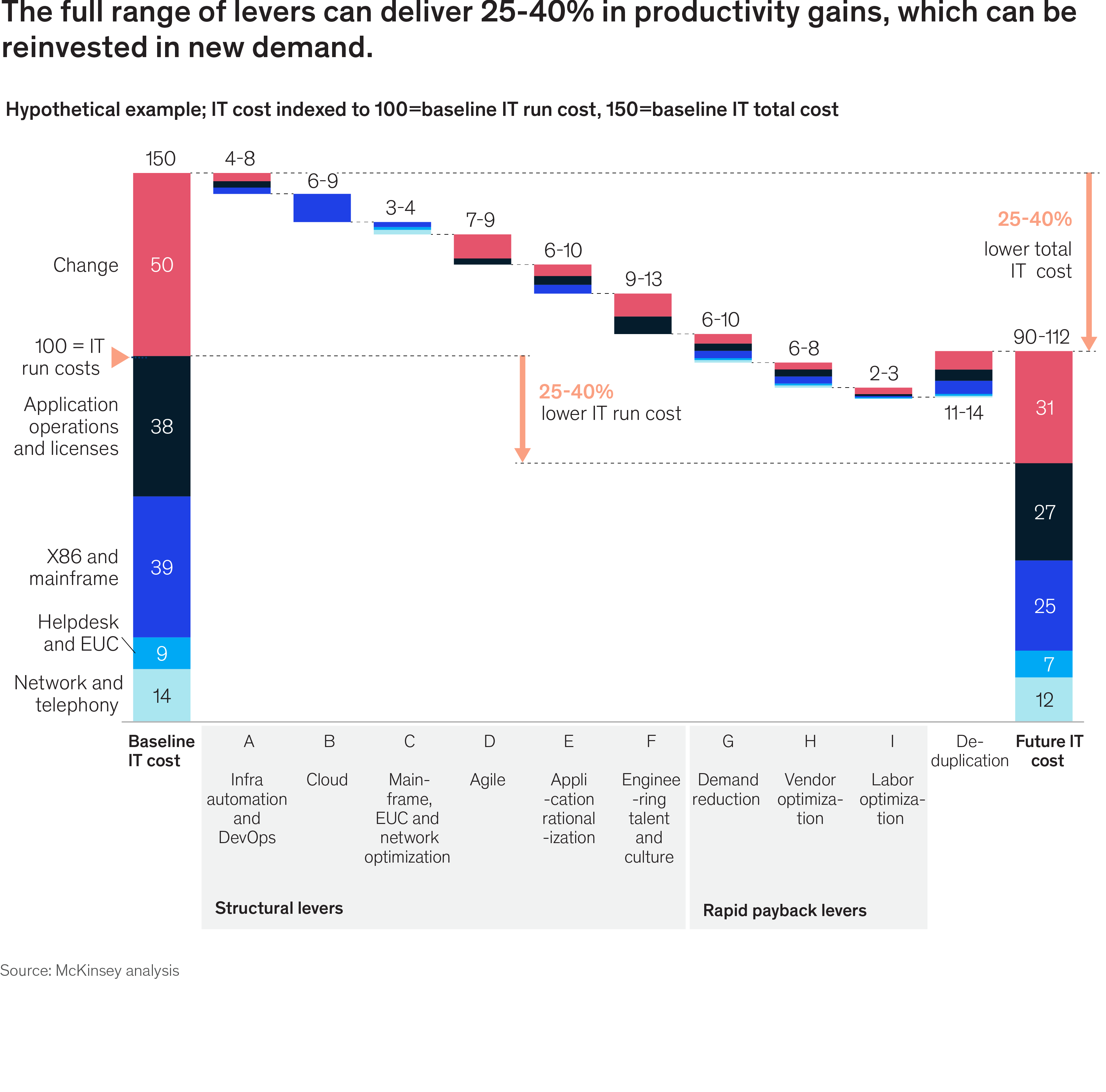

Fortunately, CIOs have many ways to improve productivity. Our experience working with banks in the last five years suggests the full set of levers can lead to 20 to 30 percent in productivity gains (Exhibit 3). The investment required would be about 1 to 1.5 times run-rate savings, with 5 to 10 percent run-rate savings achievable within the first year. A well-planned rollout could break even within two years.

Three rapid payback levers

- Demand reduction. For most banks, a comprehensive review of IT expenditures can reduce demand significantly and deliver 5 to 10 percent savings within six to 12 months. Examples include prioritizing projects that are directly linked to the bank’s strategic goals (for example, next-generation payments strategies), reducing service levels to match real demand, reducing non-value-adding service levels, shifting workloads away from peak times, capping usage, purging historic data, matching the number of licenses to the number of users, and capping end-user usage.

- Vendor optimization. Banks can reduce third-party expenditures by working more efficiently with vendors (for example, standardizing laptop images), moving vendors to alternative pricing models (for example, fixed- or performance-based pricing where appropriate), renegotiating prices (for example, estimating “clean-sheet” costs), and consolidating relationships. These efforts typically deliver 5 to 10 percent savings within six to 12 months.

- Labor optimization. Replace simple labor models, such as wholesale outsourcing, with a strategic mix of insourcing, outsourcing, offshoring, and strategic partnerships that balance costs with responsiveness, controllability, and agility. For example, many institutions are restricting the usage of temp labor to only those roles which are truly scarce or flex capacity, which can save up to 20 percent of temp labor costs.

Six longer-term structural levers

- Cloud. Transitioning to public cloud can improve efficiency 30 to 40 percent compared to traditional hosting for some workloads. In particular, labor savings can reach up to 90 percent, and banks can reduce non-labor costs by eliminating data-center related spending (e.g., housing, networking assets) and through better utilization management (e.g., shutting down development/test servers). Cloud also enables other transformation levers, such as infrastructure automation.

- Infrastructure automation and DevOps at scale. It’s possible to automate 30 to 35 percent of activities across the IT value chain—particularly provisioning, testing, deployment, patching, and support. One large traditional European bank reduced its IT infrastructure team by 45 percent in 9 months by moving to standardized, automated infrastructure products that development teams could use without manual intervention.

- Agile. Agile ways of working allow CIOs to rapidly take ideas to market, speeding up the release of new functionality from quarterly or monthly to several times per week. Agile improves application development and maintenance efficiency by 20 to 30 percent, which banks can capture either as savings or as freed up capacity.

- Engineering talent and culture. Experienced software engineers are an order of magnitude more productive than novices. However, many institutions routinely source large teams of offshore novices, leading to lower costs but very low productivity. Leading banks are insourcing roles that can provide competitive advantage and increasing the share of expert engineers (relative to novices) to improve productivity.

- Application rationalization. Banks can optimize and modernize their application landscapes by increasing cloud-based functionality and SaaS, microservices and highly configurable API-based architectures. A systematic, top-down, simplification program can reduce applications by 30 to 40 percent and the cost of ownership of applications by 15 to 20 percent. One European bank managed to reduce its total IT costs by 8 to 10 percent per year by rationalizing its application landscape.

- Mainframe, end-user computing, and network optimization. By optimizing core infrastructure components banks can build a solid foundation for the other transformation levers and reduce their run costs. Mainframes can be managed by offloading applications or transactions, using a shared mainframe environment, or smoothing peaks—which together can reduce costs by 20 to 30 percent. Helpdesk and end-user computing costs can be reduced by automating common requests (e.g., password resets), harmonizing device specifications, and through systematic root-cause analysis of the most common issues—which can reduce costs 20 to 30 percent. Network costs can be reduced through software-defined networking that responds to demand fluctuations rather than provisioning fixed capacity.

Done right, the new IT function will have a structurally lower cost base, improved customer-oriented mindsets and capabilities, and significantly improved speed and quality of delivery. It will also be better equipped to deliver future platform needs such as APIs and customer authentication, as well as business enablement needs such as digital services, AI, and so on.

As they begin this transformation journey, forward-thinking CIOs are asking themselves three questions:

- How much headroom in the IT budget do I need in order to deliver new value-adding capabilities?

- How do I sequence the IT productivity transformation in a way that is self-funding or close to self-funding?

- How should I get started on these initiatives in a way that balances the benefits, risks, and execution challenges?

Digital disruption continues to change the banking landscape and put pressure on the traditional banking model; meanwhile, growth is becoming more difficult for banks as the global economy appears to slow. To thrive in this environment, banks must build highly efficient IT delivery models. The eventual winners will be those that use these productivity gains to create the necessary “headroom” in their budgets to invest in critical tech-enabled changes, thus ensuring they are a true partner to the business in an increasingly dynamic environment.