For almost a decade after the financial crisis, M&A activity in the US banking industry remained limited, as many banks wrestled with challenging integrations and “shot-gun” combinations. But deal-making bounced back in 2018 and looks likely to expand. While several factors favor that growth, would-be deal-makers face obstacles. Our analysis suggests that most US bank mergers from that decade failed to create value. Going forward, US banks will require a smart strategy and the right integration approach to fully realize the value creation potential in M&A.

US banking M&A is on the upswing

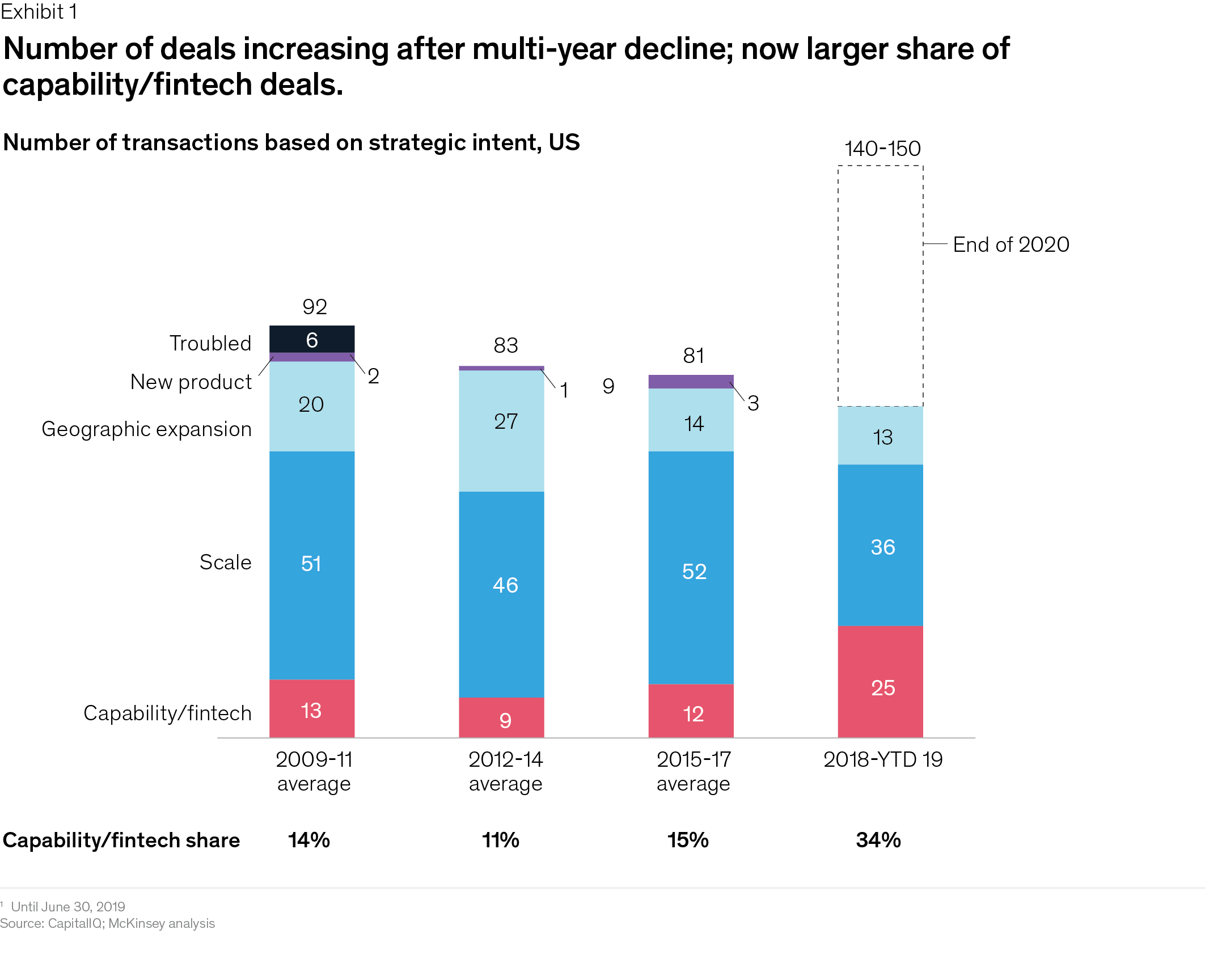

US banking M&A was relatively flat from 2009 to 2017; the industry averaged about 20 deals a year. But in 2018 activity more than doubled, as US banks completed 49 transactions. And, with total deal value of $38 billion through the first half of 2019, this year already substantially outpaces 2018.

While many recent deals, such as the merger of BB&T and SunTrust and that of TCF and Chemical Financial, have focused on increasing geographic footprints and scale efficiencies,1,2 fintech and capability-building deals are gaining traction. US banks averaged just three or four fintech deals per year through 2017, but deal volume exploded in 2018 with 16 transactions, and the first half of 2019 saw nine fintech deals (Exhibit 1). A good example of recent deals is Goldman Sachs’ acquisition of United Capital and its FinLife CX digital customer-service platform to add an advisor-led tech-enabled platform to the bank’s growing suite of digital offerings.3

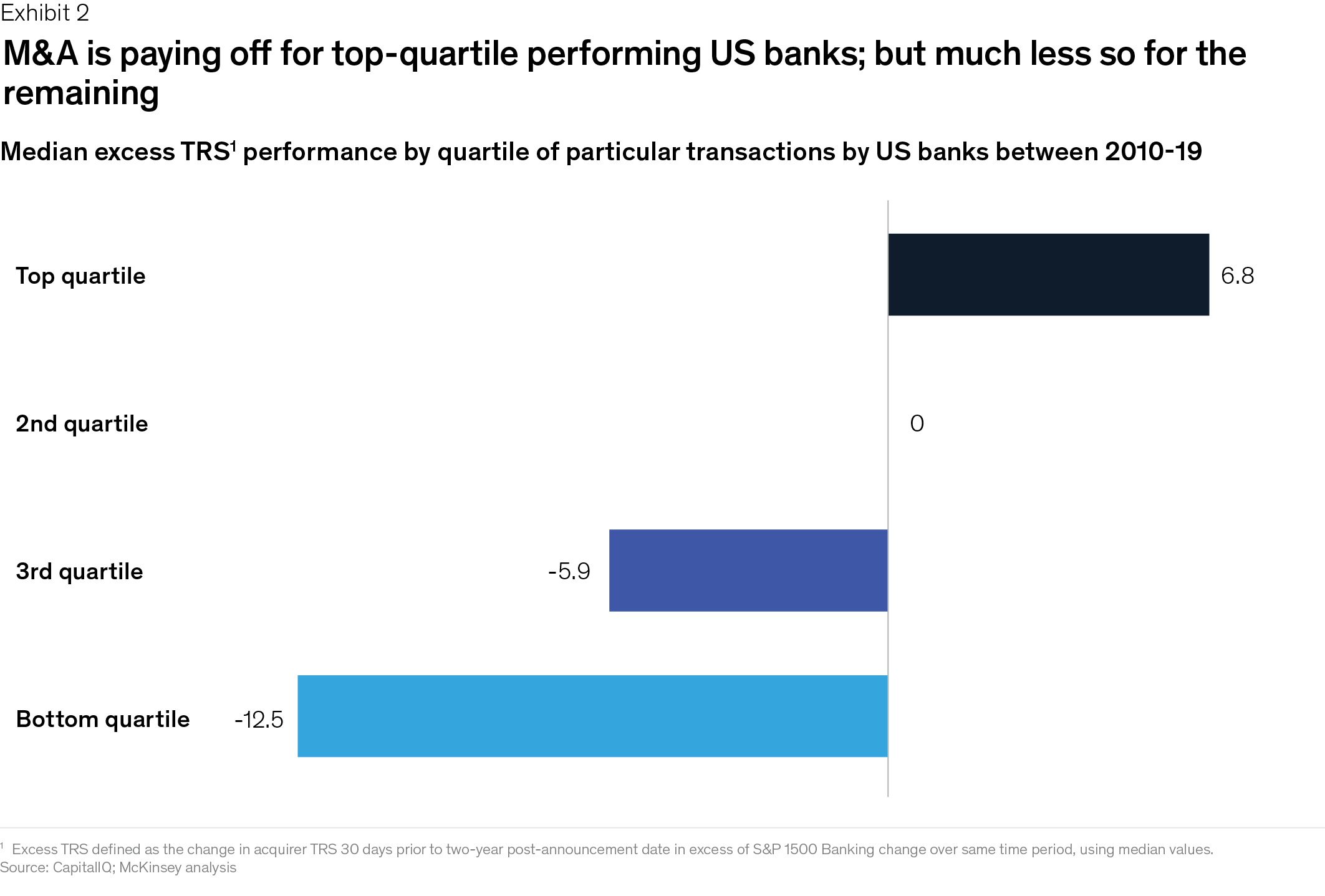

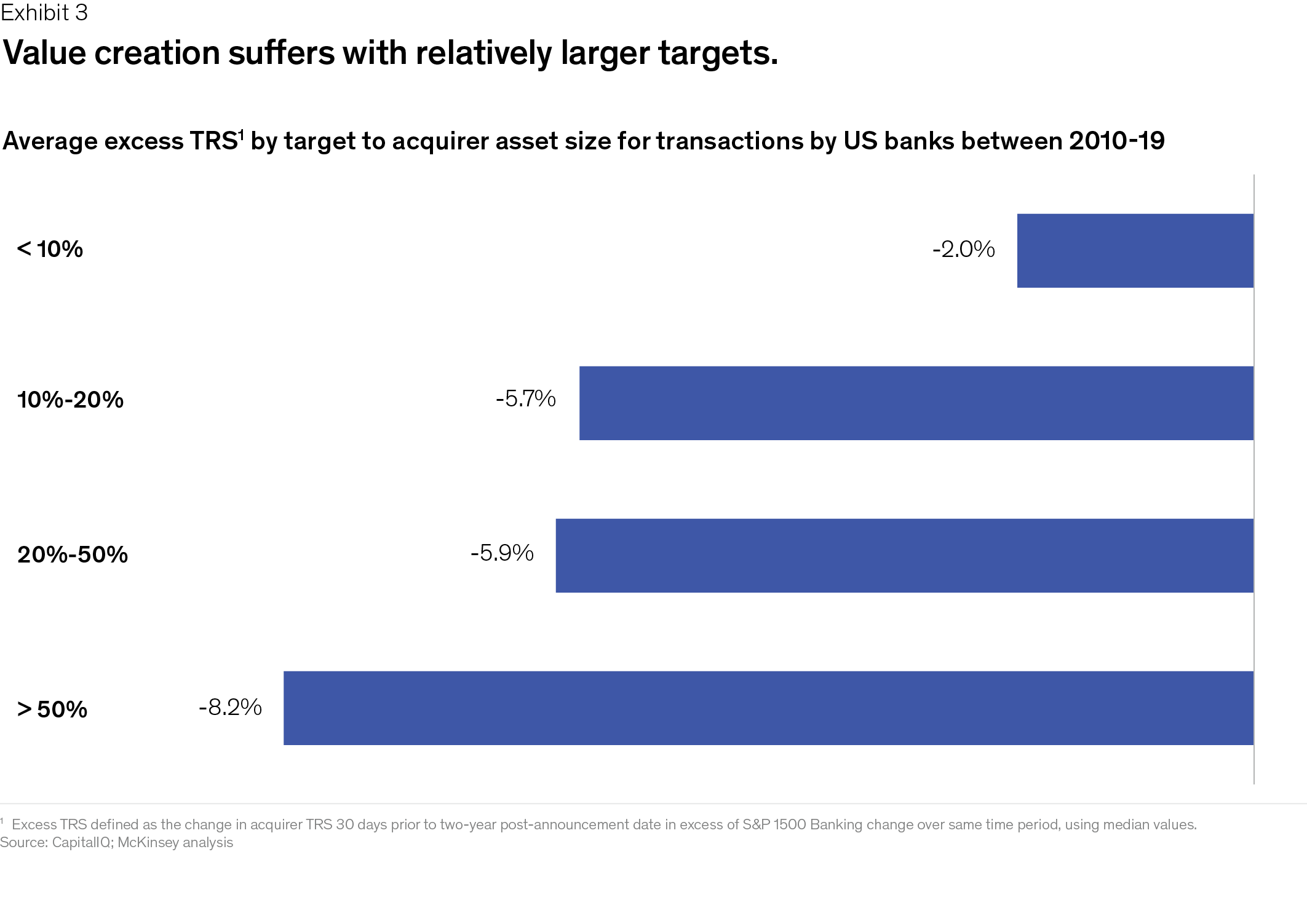

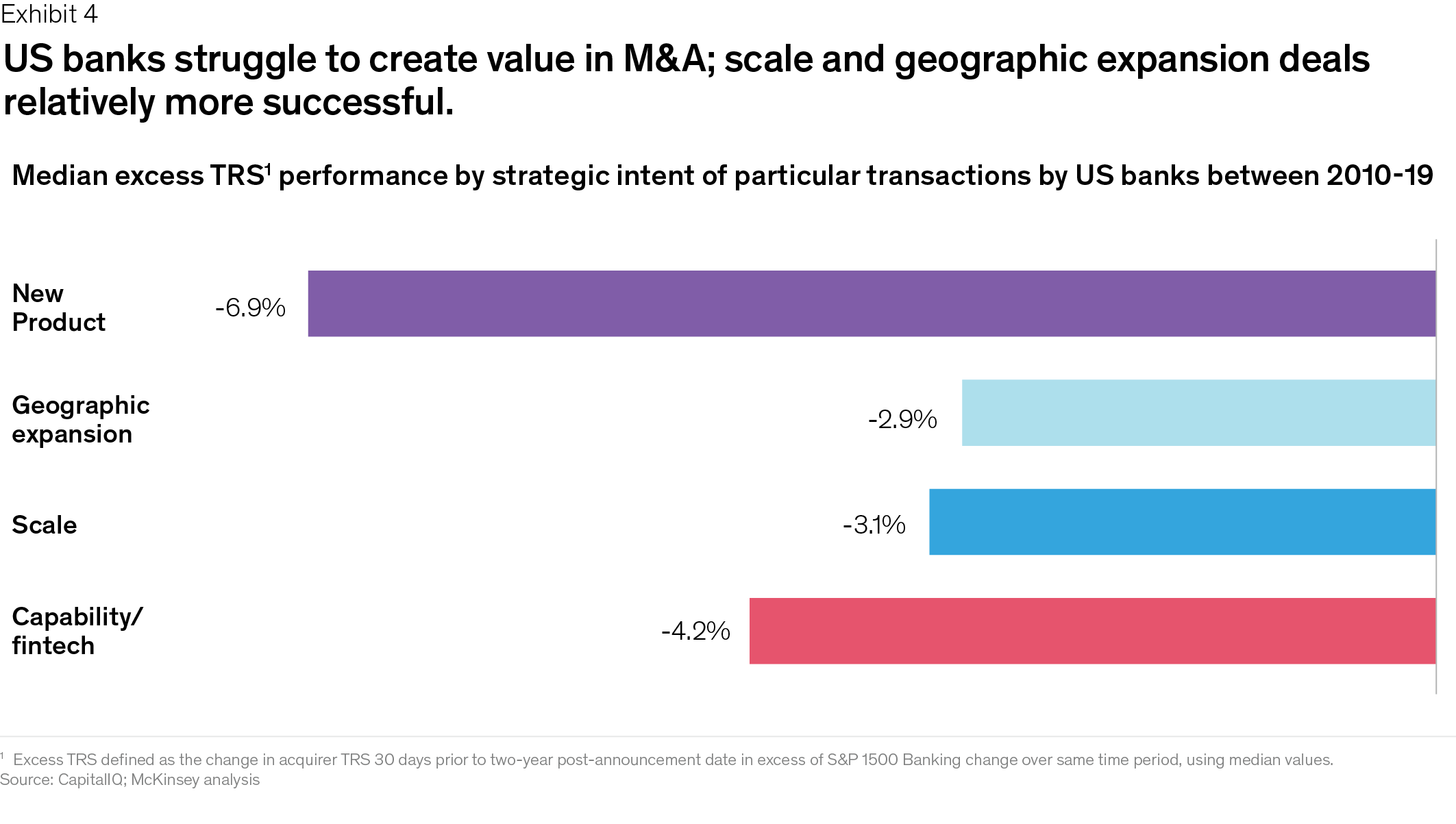

While top performers have realized substantial returns on M&A, value-creating M&A has proven elusive for many US banks (Exhibit 2). Since the financial crisis, the total return to shareholders (TRS) of acquiring banks has underperformed the banking industry index by a median of 320 basis points a year.4 And two of the most important deal types have also performed the worst. The average TRS in fintech deals trails benchmark indices by 420 basis points. In large deals where the target’s size is more than 50 percent of the acquirer’s size, average TRS performance is a jaw-dropping 820 basis points below the banking index—despite having started with the lowest acquisition premiums (Exhibit 3). Even with strong tailwinds, large deals and fintech deals require an updated approach to create value.

Tailwinds favor M&A growth

In 2019, market reaction to bank-to-bank and fintech mergers has generally been positive. On the day of deal announcement, the market rewarded both BB&T and SunTrust with share value increases of 4 percent and 10 percent, respectively. More fundamentally, we believe there are multiple reasons why M&A activity in US banking could continue to increase.

The profitability of US banks has improved substantially, thanks to significant productivity investments, higher interest rates, and lower taxes. The average ROE of US banks climbed from 8.6 percent in 2013 to 10.8 percent in 2018. Banks also enjoy a stronger capital position that puts them in a better position to execute M&A.

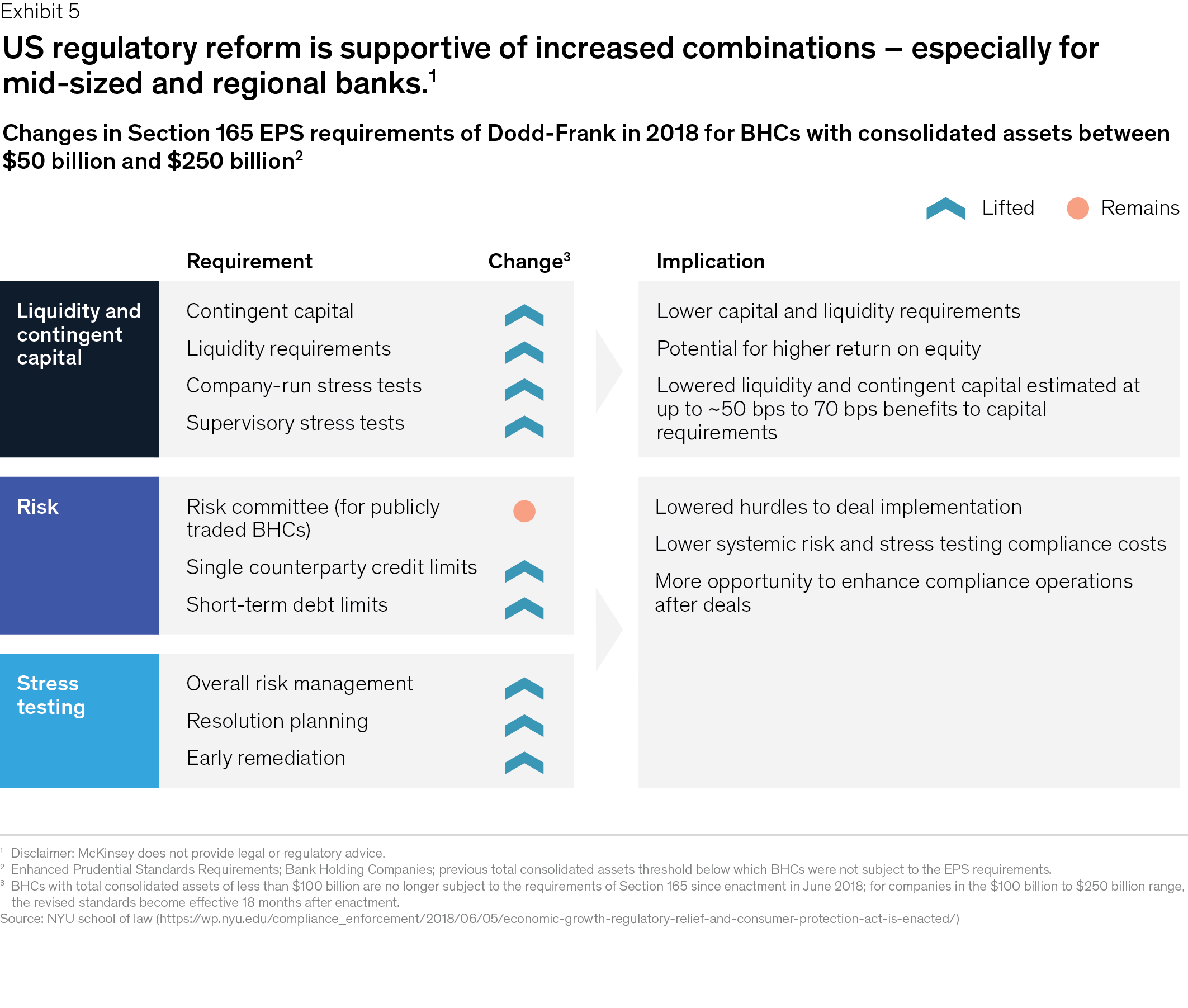

Regulatory reform is reducing requirements for banking combinations. The threshold triggering substantial additional process and capital measures has increased from $50 billion to $250 billion (Exhibit 5). This particularly benefits regional banks that need greater size and scale to strengthen their competitive position for deposits versus larger banks—where they have been challenged.

US regional banks face intense pressure to build new capabilities in robotics, machine learning/artificial intelligence, and advanced analytics (e.g., people and talent analytics) as banking increasingly digitizes. M&A is one of the best ways to acquire skills or generate cost efficiencies that can fund internal efforts. For example, when BB&T acquired SunTrust, it announced a cost-savings target of $1.6 billion and plans to invest a substantial portion into digital banking.5 JPMorgan Chase earmarked $11.5 billion in 2019 alone for technology investments, with machine learning, artificial intelligence and blockchain identified as top priorities; a good example is the bank’s recent acquisition of InstaMed, to support its position in payments. CapitalOne purchased Wikibuy, an online website that allows shoppers to compare prices for items, to help customers “feel confident in their purchasing decisions.”6

The US is home to a lot of banks. While consolidation has steadily reduced the number of US banks from roughly 15,000 in 1985 to about 5,000 today, many industry executives and experts expect the consolidation trend to continue. Our research shows that more than 60 US banks with assets of $10 billion to $25 billion might be attractive acquisition targets for well-positioned regional banks—for example, regional banks with a high cost-income ratio and a low loans-to-deposits ratio, among other factors.

Beyond these trends favoring M&A growth, we believe that M&A will prove critical to next-generation transformation in US banking. Leading digital European markets clearly demonstrate the power of digitized banking, as banks there are achieving cost-to-asset ratios as much as 60 to 80 percent lower than US banks. A smart, well-executed M&A strategy can equip US banks to make slow internal efforts history. Banks can dramatically improve their cost productivity, with machine learning and robotics, and their people development, with advanced people analytics that better match talent to value and develop future leaders.

Successful bank acquirers get nine things right

In our experience, successful bank acquirers of other banks and fintechs take a strategic, long-term approach to M&A. They invest time and resources to build an end-to-end M&A approach, including deep understanding of how M&A serves their overall strategy, optimal candidate development and cultivation approaches, the merger management expertise required to execute, and the long-term capability development that enables them to deliver consistently.

In our work, we see the most effective acquirers apply nine principles to realize full value from their M&A strategy.

1. Make M&A a core plank of the overall strategy—don’t rely on opportunistic M&A.

Too many acquirers resort to M&A as a way to buy growth or acquire an asset opportunistically, reacting to available deal flow to drive activity, without thorough understanding of how the deal will create value.

The best acquirers embed M&A in their strategic planning process. They require businesses to identify where inorganic moves are necessary to advance the bank’s strategy and then translate these moves into actionable deal theses that guide candidate scanning, prioritization, and progress review. Only after pressure-testing and prioritizing these themes do leaders develop lists of M&A targets that fit the investment themes within the overall strategy.

For banks, this means making M&A an integral part of the capital-planning process, with the annual capital plan adjusted—materially—to support the highest-potential investment themes. Practically speaking, this effort requires getting very clear on the decision rights and governance model for M&A execution; for example, who leads pre-diligence exploration of companies on the M&A candidate lists, what role the CFO plays, and what triggers full diligence.

2. Continuously cultivate top-priority deal candidates with a programmatic approach, not one-off efforts.

The best bank acquirers source and develop potential M&A candidates continuously and develop them across all stages of the M&A process. These efforts extend from conducting rapid pre-diligence review of prioritized targets, including high-level valuation and assessment of synergy potential, to proactive outreach to targets, supported by talking points on the bank’s partnership vision.

One leading acquirer maintains a dynamic list of over 100 potential candidates across its businesses, organizes regular “getting to know each other” meetings, and conducts careful, creative, later-stage relationship-building efforts (including family picnics with the CEO) to identify the candidates that promise the best fit. Get-acquainted efforts loom especially large in fintech deal-making, as the fintech value proposition is often outside a bank acquirer’s core business, and cultural fit and successful integration are especially critical to success. JPMorgan Chase’s recent acquisition of WePay for $400 million supports its payments platform and also increases its presence in Silicon Valley.

3. Assess the full spectrum of opportunities, including partnerships, joint ventures, and alliances, to gain scale and capabilities.

Highly innovative industries like pharmaceuticals and high-tech have long relied on joint ventures and alliances to develop their businesses. As banking advances further into digitization and advanced analytics, JVs and alliances are becoming much more relevant, especially for regional banks that lack the digital and fintech M&A resources of the larger money center banks. In particular, to succeed in digitization, many regional banks will have to assess the full range of partnership opportunities, from full joint ventures (with or without equity) to strategic partnerships to contractual alliances.

Across this range, banks need a clear strategic objective and business case for the partnership (versus valuation for a transaction), including a methodology for valuing each partner’s contribution, a clear and aligned vision for the end state, a pre-launch partnership structure, and aligned governance arrangements that articulate clear management KPIs, transition and operational support agreements, and restructuring and exit provisions.

For example, in an effort to innovate in customer service, US Bank partnered with Optum360. According to US Bank, the partnership marries the bank’s financial expertise with Optum360’s healthcare-focused technology and analytics to expand their revenue cycle management offering to healthcare providers.7

4. Tap divestitures to strengthen value creation—don’t buy without understanding the potential for a simultaneous sale.

Our analysis of thousands of deals finds that companies active in divesting, not just acquiring, achieve TRS that is 1.5 to 4.7 percent higher than the TRS of companies focused on acquisitions alone.

Successful bank acquirers use forcing mechanisms like the budget process to review the landscape of potential assets to sell and proactively shape the assets for sale based on an understanding of their value to a more natural owner. These winners also pay special attention to managing the stranded costs that can represent huge value leaks for banks.

One leading money center bank makes divestiture review part of its annual strategic planning process, evaluating businesses throughout the year on their strategic importance, operational value, and amount of capital freed up, if sold. The bank has a “productivity czar” who reports to the CEO and uses an algorithm-supported approach to counter the tendency of division leaders to protect assets in their portfolio by overstating their importance. The algorithm deepens insight into growth contribution (or lack of), required management resources, operational complexity, capital deployed, and ROE impact. This approach makes the bank much more nimble in divestitures and ready to use “acquisitions for growth” as catalysts for simultaneous value-adding divestitures.

5. Establish a value-added integration management office (IMO) led by an “integration CEO”—don’t make integration a checklist exercise.

We often hear financial industry executives say that they have a merger playbook and know how to execute. But the TRS numbers show that banks have struggled to create value through M&A.

Beating the odds requires more than checklists used in past integrations or third-party process support. M&A winners establish an IMO and empower an integration CEO to tailor how they manage every integration effort to deal rationale and sources of value. For example, winners heavily discount cost synergies envisioned beyond 24 to 30 months because they know the importance of realizing the lion’s share of the synergies in year one. Winners also move purposefully to take control of the acquired bank, particularly its credit decisions, portfolio management, and back-office systems and costs. One leading bank mobilized a “SWAT” team to stabilize the target’s shaky balance sheet and free up substantial capital.

Winners also implement cost-saving measures as soon as possible. Failure to do so poisoned the culture in one bank’s branch sales network through delaying inevitable branch headcount reductions until several months into the integration effort.

6. “Open the aperture” on capturing value—don’t rest with the due diligence numbers.

Failing to update synergy expectations during integration is one of the most common, but avoidable, pitfalls in any transaction. This is especially true in banking, where the industry structure invites treating M&A as a project. This project typically sets synergy targets during due diligence, builds the targets into department operating budgets, and creates a checklist-based PMO process to monitor progress against the targets.

M&A winners regularly exceed due diligence synergy estimates by 200 to 300 percent because they reassess synergy potential throughout the life cycle of the deal, especially pre-close, pushing hard to uncover upside and transformational synergies. In successful banking deals, this often means dividing synergy-capture efforts into two time-based categories ─ initiatives that move quickly to generate maximum bottom-line impact in the first year (and often capture 50 to 70 percent of the cost synergies) and larger, longer-term initiatives that are typically technology-dependent.

Protecting the base business is a critical component of value capture that often goes unappreciated in banking mergers. M&A leaders make taking frequent temperature checks and attending to the health of the front-line business and customer satisfaction during integration a core responsibility of the integration CEO. For example, customer churn in corporate banking requires special attention early in the merger, since many customers do business with multiple banks. In a recent successful merger, this meant proactive outreach to corporate customers by pairs of acquirer/target relationship managers and careful manual migration of customers to the acquiring bank to avoid any errors or complaints.

Ensuring that the value capture team opens the aperture on synergies is particularly important given the recent tendency to announce a banking deal as a “merger of equals.” The intent is admirable but impractical to enact. Merger-of-equals positioning may benefit pricing, but it typically slows and softens decision-making, hamstrings implementation, and raises the risk of value leakages throughout the integration effort.

7. Build an independent technology roadmap—don’t let current business operators and maintenance dictate the approach to capturing value.

In our experience, IT enables about 70 percent of a bank’s cost synergies but, without careful planning, can easily take 50 percent longer than expected to capture the value and can add incremental costs of 50 to 100 percent to what the bank already spends on IT. Making tough choices on IT integration is especially challenging for banks because they rely heavily on third parties to maintain their many custom-built legacy platforms. Banks can’t always count on those providers to provide objective advice on the right technology roadmap to follow.

Successful bank acquirers make IT integration a strategic priority, rather than a PMO-managed integration project. They develop an overall technology blueprint aligned with their strategy, sources of deal value, and customer-service requirements before launching costly IT integration initiatives and project management. One M&A leader looks to independent, internal subject-matter experts to build the “no case” for proposed technology roadmaps, tasking them with pressure-testing the logic and forcing discussion of other options.

This approach is particularly salient in fintech deals, since, along with talent, the technology platform is often the raison d’être of the deal, but in some cases that platform may meaningfully exceed the experience and expertise of the bank’s IT team. The bank must determine as early as possible what capabilities of the target the deal should preserve and what target-specific attributes (people, processes, and platforms) make those capabilities work so the integration effort can protect and nurture those attributes to scale.

One M&A leader has repeatedly chosen its future platform within the first months after deal announcement, using workarounds after close to maintain an adequate customer experience until the optimal systems integration roadmap is ready. This bank often migrates first and transforms later because it knows that advancing on both fronts at once is too complex. In a recent successful bank-fintech merger, customer migration proceeded in two waves—manual migration of corporate customers, followed by automated migration of retail customers.

Goldman Sachs’ acquisition of Final is a good example of a deal that augments strategy, in particular Goldman Sachs’ publicly stated objective to invest in its consumer-centric business. Final impacts Goldman Sachs’ partnership with Apple Card by adding digital features for fraud and theft protection, including those which allow consumers to monitor their spending in real time.

8. Take a scientific approach to identifying cultural issues and change management—don’t pay lip service to cultural integration.

Mission, vision, and values can look very similar across banks. Executives often return from pre-deal announcements convinced that the cultures of the companies involved are very similar and that smooth organizational integration will be a snap. This is a major source of deal failure.

M&A leaders don’t underestimate the importance of proactively tackling the challenges involved in integrating cultures. They understand that culture goes beyond values and comes alive in a company’s management practices—the way that work gets done, such as whether decisions are made by consensus or by the most senior accountable executive.

If not addressed properly, cultural integration challenges inevitably lead to friction among leaders, decreased productivity, increased talent attrition, and lost value. M&A leaders rigorously assess top management practices and working norms early and design the overall program to align practices and mitigate risks early and often. Alphabet, for example, is well-known for a programmatic approach to M&A and integration of fintech acquisitions that proceeds in phases linked to talent and sources of deal value.

Successful cultural integration often lends itself to an added area of opportunity in scale mergers. In these cases, the merger itself can be leveraged to reinforce critical behaviors that may be lacking in the acquiring organization, thereby creating not just an integrated culture but putting a stop to bad behaviors that might have existed pre-integration. In these situations, leading organizations choose to evaluate culture, and more broadly talent management and experience, holistically across both organizations and set a clear aspiration for a merged culture that will best enable the new organization’s strategic goals. This is particularly important when the acquisition brings in fundamentally new talent pools that may have different definitions of success, progression, and experience, as in the acquisition of a fintech into a large traditional bank.

M&A leaders also don’t skimp on formal change management planning. They take a rigorous and regimented approach to each phase of the integration, engaging stakeholders through the process and ensuring a dedicated handoff period for the transition to steady state.

9. Build capabilities for future deals—take full advantage of every opportunity to deepen the bench.

M&A leaders treat each deal as an opportunity to upgrade their M&A team’s skills and expertise. In banking M&A, talent is increasingly emerging as one of the primary sources of competitive advantage. Banks that allocate human capital, as well as financial resources, strategically and dynamically stand to generate significant economic return. This makes leadership and talent development the “next big thing” for unlocking value in banking M&A, with direct impact on the bottom line.

After doing a deal, M&A leaders are just as rigorous in measuring success. They carefully track deal impact across critical KPIs, such as lower cost-income ratios, increased revenue growth above base trajectory, and more efficient use of capital.

Many CEOs and top teams in US banking and fintech see increasing their existing talent bench as critical for success, as has been raised with McKinsey in multiple CEO discussions and recent banking executive roundtables. Most need to make building M&A and integration skills a top priority. This calls for defining their talent development needs comprehensively and responding appropriately—for example, with executive training programs, leadership development, functional capability-building, coaching, and proprietary diagnostics for the talent development “playbook.”

One winning financial industry acquirer regularly devotes a full day, usually a weekend, to reviewing the profiles needed for the integration of a specific deal. This M&A leader spends substantial time identifying the right talent for each role and making sure that the hand-picked leaders get the right training to succeed in the context of the given deal.

***

Deal-making by US banks spiked in 2018 and shows an upward trajectory for 2019. Many banks can capitalize on the opportunities, especially if they apply the principles of M&A strategy and integration that have served the few successful acquirers in the industry so well.

The authors would like to acknowledge the contributions of Alok Bothra, Alex Camp, Kameron Kordestani, Steve Miller, and Zoltan Pinter to this article.

Click here to download a PDF of the article.1 “BB&T and SunTrust to Combine in Merger of Equals to Create the Premier Financial Institution,” SunTrust press release, February 7, 2019.

2 “Chemical Financial Corporation and TCF Financial Corporation Close Merger of Equals to Become the New TCF,” Business Wire, August 1, 2019.

3 “Why United Capital Chose Goldman, Not a PE Backer,” Barrons, May 16, 2019.

4 Based on comparison with an index of peers’ TRS during the two years following an acquisition.

5 “BB&T and SunTrust to Combine in Merger of Equals to Create the Premier Financial Institution,” SunTrust press release, February 7, 2019.

6 “Changing the Game: Saving Money Online Is Easy, Lightning Fast With Wikibuy from Capital One,” CapitalOne.com.

7 “U.S. Bank expands fintech partnerships to B2B space,” usbank.com, October 29, 2018.