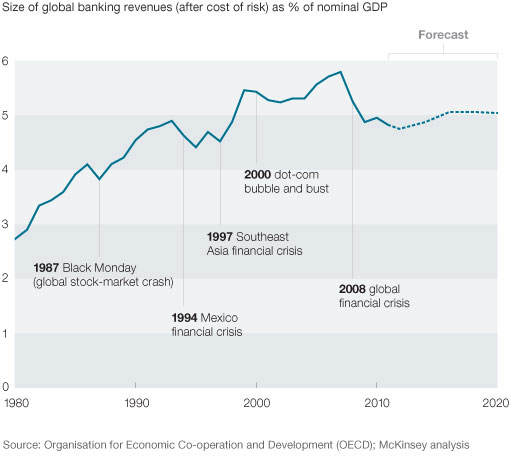

After climbing for 30 years, the share of economic activity attributable to bank revenues1 fell in the wake of the global financial crisis. Looking forward, revenues could flatline at about 5 percent of GDP through 2020 (exhibit). In fact, that’s our base scenario for the global banking industry—one that implies growth at the same rate as nominal GDP, following the pattern of other industries.

In developed markets, factors contributing to this trajectory include deleveraging and stiffer regulatory regimes that will require higher bank-capital ratios. In many emerging markets, banking penetration is relatively low (less than 4 percent in India, Mexico, Nigeria, and Russia, for example). In others, it is falling—in China, from 6.2 percent to 5.3 percent, we estimate, mostly as a result of credit liberalization, which will go on dampening margins. These forces are unlikely to be counterbalanced by the positive impact of outliers such as Brazil (where banking penetration is more than 10 percent), global infrastructure-spending growth, or the emergence of a new class of borrower in developing nations. If interest rates in developed markets rose faster than anticipated, or if an unexpected burst of product and service innovation took hold, though, the industry’s growth could become stronger.

Banking’s growth as a share of global economic activity may be leveling off.