The development paradigm that brought China two decades of rapid growth and lifted millions of people out of poverty is reaching the limits of its utility. Well before the US credit bubble imploded, China’s leaders recognized that this old economic model, with its heavy reliance on exports and government-led investments, was straining at the seams.1 The global recession that followed Lehman Brothers’ collapse put the model’s drawbacks into sharp relief. When exports plunged, factories closed, and millions of Chinese migrants lost their jobs, Beijing responded with a $600 billion stimulus package and a torrent of new lending by state-owned banks.

But those remedies, while highly successful in restoring short-term growth, risk aggravating structural distortions that made China’s economy vulnerable to external-demand shocks in the first place. As the global crisis ebbs, China’s leaders realize more clearly than ever that they must unleash consumer spending to achieve sustainable growth. Stoking Chinese consumption has vaulted to the top of national—indeed global—policy agendas. But how, and how much, can it be raised?

To answer that question, the McKinsey Global Institute (MGI) considered three scenarios for Chinese consumption rates over the next 15 years: a base case (no new action to raise consumption), a policy case (full implementation of proconsumption measures already announced), and a stretch case (a push beyond the current agenda to implement broad changes in the economy’s structure).

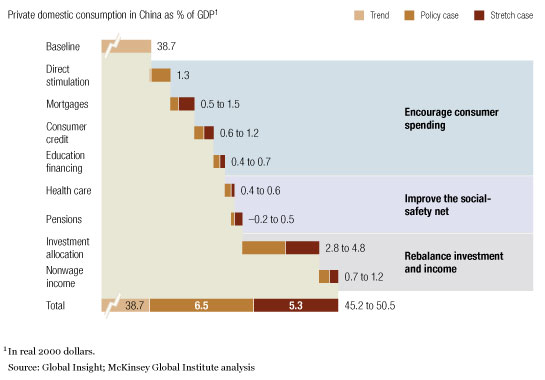

MGI estimates that in the base case, China’s consumption will rise to 39 percent of GDP, a gain of just three percentage points above the current level, leaving the country heavily dependent on exports and government-led spending for continued growth. In the policy scenario, consumption could account for as much as 45 percent of GDP, still well below levels in other major economies. If China’s leaders committed themselves to the more aggressive program of comprehensive reform envisioned in the stretch scenario, however, they could raise private consumption above 50 percent of GDP by 2025 (Exhibit 1). Clearing that threshold would bring the consumption rate in line with those in the developed nations of Europe and Asia, vaulting China’s economy into a new phase. McKinsey estimates that comprehensive reform would also enrich the global economy with $1.9 trillion a year in net new consumption, boosting China’s share of the worldwide total to 13 percent—four percentage points higher than its share without further effort.

Tools for raising consumption

Reaching the stretch target wouldn’t be easy. China’s leaders will have to wage a sustained policy struggle on many fronts, combining relatively straightforward measures to encourage private spending with fundamental reform of the nation’s health and pension systems and sweeping changes in the economy’s basic structure. Over the next 15 years, China can realistically hope to increase private consumption’s share of total GDP significantly—but only if policy makers depart from the current development paradigm and embrace new policies, structures, and institutions better suited to the country’s status as a large, maturing market economy. That transformation, though daunting, would have a worthy prize: a more stable and fair economy that uses resources more efficiently, creates more jobs, insulates its citizens from foreign-trade shocks, and contributes more substantially to global growth.

China’s constrained consumers

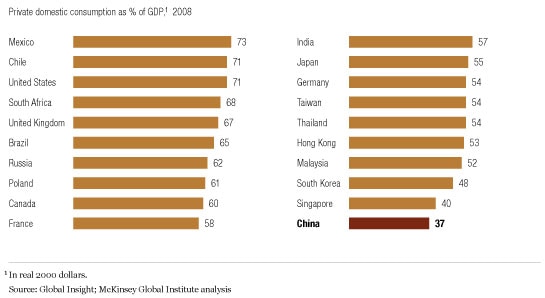

In seeking to bolster private consumption, China’s policy makers face a unique challenge. Although there is no generally accepted standard for “healthy” private consumption in developing economies, in China it is anemic by almost any measure. Private consumption there totaled $890 billion in 2007, making the country the world’s fifth-largest consumer market, behind the United States, Japan, the United Kingdom, and Germany (which China recently surpassed as the world’s third-largest economy). But relative to China’s population and level of economic development, its consumers punch far below their weight. The country’s consumption-to-GDP ratio—36 percent—is only half that of the United States and about two-thirds those of Europe and Japan. Indeed, China has the lowest consumption-to-GDP ratio of any major world economy except Saudi Arabia, where oil exports contribute the bulk of economic output (Exhibit 2).

Frugal China

In fact, China’s consumption-to-GDP ratio has dropped by nearly 15 percentage points since 1990 and continues to deteriorate in the aftermath of the financial crisis. While falling consumption rates are common in developing economies, the speed and magnitude of this decline have no precedent in modern history. In the United States, private consumption remained above 50 percent of GDP even during the full-scale industrialization drive of World War II. In Japan and South Korea, consumption remained above 50 percent during periods of rapid industrial development.

The sources of China’s low consumption rate are both behavioral and structural (see “China’s consumption challenge”). The country’s households have an extraordinarily high ability to save: the average Chinese family squirrels away an astonishing 25 percent of its discretionary income, about six times the savings rate for US households and three times the rate for Japan’s. Indeed, China’s savings rate is 15 percentage points above the GDP-weighted average for Asia as a region.

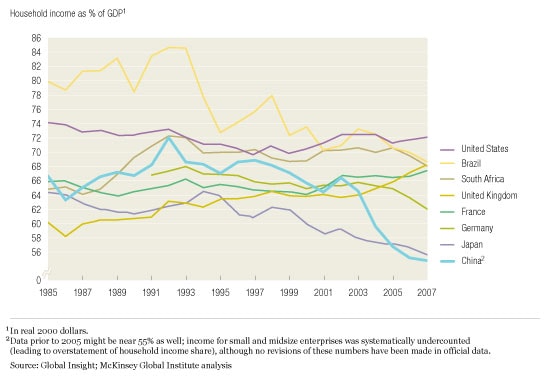

Frugality’s impact is compounded—and in many ways produced—by structural features that restrict consumption’s share of the national income. For one thing, Chinese households command only some 56 percent of it (Exhibit 3), compared with more than 60 percent in Europe and more than 70 percent in the United States. No effort to raise Chinese consumption rates significantly can hope to succeed without addressing the structural factors that both channel income away from consumers and discourage them from spending even their modest share.

Household finances

Mending the social safety net

Perhaps the most common explanation for the Chinese consumer’s reluctance to spend more freely is the frayed social safety net. Many argue that the country’s consumers oversave and underspend because they lack adequate health insurance and can’t count on government- or employer-sponsored programs to provide for them in retirement (see “Unlocking the power of Chinese consumers: An interview with Stephen Roach”). The relationship between social-welfare programs and private consumption is complex, but the moral imperative to extend health and retirement protections to the millions of Chinese who lack them is clear. Over the long run, mending the social safety net would ease anxieties about the future and bolster consumer confidence.

But MGI believes that better health and pension guarantees wouldn’t raise private consumption significantly before 2025. In assessing their impact on consumer spending, the key question to consider is who pays for them. If enhanced health and retirement benefits were financed through increased or expanded payroll taxes—a virtual certainty—households would feel less pressure to save, but after withholding they would have less money to spend. Thus the primary impact of expanding health and pension programs would be distributive, shifting to middle- and upper-income households the cost of benefits for poor ones. Moreover, any effort to broaden health insurance coverage would probably require a substantial increase in public outlays for medical care and thus raise the government’s share of total consumption.

MGI’s effort to model the reciprocal effects of such changes suggests that, in the aggregate, even a fully fledged program to expand China’s health and retirement benefits wouldn’t raise private consumption’s share of GDP significantly. We estimate that, at best, such improvements would boost it by only a percentage point above the 2025 base-case projection.

Putting products within reach

Measures to make goods and services better and more easily available could encourage consumption much more than would fixing the social safety net. China’s consumer infrastructure is incomplete. Too few products are tailored to the needs of those who would use them. Prices remain high compared with income levels: a Chinese worker toils more than seven hours to buy the same amount of goods and services a US worker earns through only one hour of work. In rural China—home to more than half of the country’s 1.3 billion consumers—organized retail establishments mediate only 18 percent of consumption, compared with 50 percent in urban areas.

Even when high-quality products are readily available, China’s consumers hesitate to buy them on credit. At 3 percent of GDP, outstanding consumer debt in China falls well below that of other large developing countries, such as Brazil, at 12 percent, or Russia, at 7 percent (see sidebar, “China’s fast-evolving consumer finance market”). What’s more, the privatization of China’s housing stock created a powerful new imperative to save: only the most affluent urban families can obtain mortgages, which thus account for just 23 percent of the value of new homes in China, compared with 65 percent in the United States.

Similarly, concerns about financing the cost of a university education drive much of China’s saving: an April 2009 survey of urban Chinese households commissioned by MGI found that this was the number-one reason for it, eclipsing concerns about medical expenses and retirement. In China, local governments provide for primary and secondary education. But surveys suggest that nearly nine in ten Chinese households hope to send their children to colleges, where costs are high relative to incomes—on average, the cost of a university education is nearly half the disposable income of a typical Chinese family. China has two national student loan programs, but only 10 percent of its college students now participate in them.

MGI estimates that, in the aggregate, measures to facilitate consumer spending—through better and more easily available products and expanded access to consumer credit and to financing for a university education—could raise consumption’s 2025 share of GDP by 2.8 to 4.7 percentage points.

Restructuring an investment-centric economy

Over time, a stronger social safety net and improved access to better goods and services will encourage China’s households to save less and spend more. But the country can’t hope to increase its consumption rate meaningfully unless it reverses a major current trend: households have a small and shrinking share of the national income. Any significant rise in household incomes will in turn require far-reaching policy changes that would transform some of the economy’s most basic structures. The fundamental causes of depressed consumption rates are systemic—hardwired into a development model that values investment over household income—rather than unique consumer preferences rooted in culture.

China’s current growth model tilts overwhelmingly in favor of large industrial companies, which typically are state owned or led, benefit from preferential financing from state-controlled banks, and enjoy considerable monopoly power. These features collectively place consumers at a disadvantage and limit employment growth. In any economy, large companies in heavy industry tend to be capital intensive, requiring fewer workers per unit of output than smaller firms in light industries or the service sector. In China, state ownership of heavy industry magnifies this tendency. Such companies, which can count on ready access to capital from China’s big banks and don’t have to pay dividends on state-owned shares, have ample funds to plow back into capital investment. Large, state-led manufacturers tend to have monopoly power in their industries, making it easier to resist pressure from workers for higher wages.

The result is an economy dominated by giant, capital-intensive manufacturers with strong incentives to pile profits back into ever more plants and equipment rather than disburse them to households as dividends or wages. Labor-intensive producers—small and medium-sized enterprises—and the services sector get short shrift. Over the past two decades, the corporate share of China’s national income has risen to 22 percent, up from 14 percent, even as the share of households has fallen to 56 percent, down from 72 percent. Media images of the country’s factories teaming with workers belie the reality: the economy generates too few jobs given its size and rapid expansion. In recent years, employment growth has inched forward at a rate of 1 percent per year even as GDP advanced by double digits.

Ultimately, China can’t hope to unleash the power of its consumers unless the economy creates more jobs and pays higher wages, so regulatory policies must change. Banks should be encouraged to support the services sector as well as small and medium-sized enterprises. Dividend policies for state-owned enterprises should be changed and the development of equity markets encouraged. By 2025, a comprehensive effort to restructure the economy along these lines could add 3.5 to 6.0 percentage points to consumption’s share of GDP.

A fundamental shift

China has already embarked on measures that will shift the focus of its economy away from heavy industry and exports and toward services and consumer products. But two wide gaps remain: between what’s been proposed and achieved and between what’s been achieved and the country’s long-term potential. The government’s stimulus package, by offsetting collapsed overseas demand for Chinese goods with a huge jolt of new domestic public and business investment, has helped the country shake off the global recession’s immediate impact. But the stimulus package does little to tilt the balance in favor of private consumption. In the short term, it will do just the reverse: 89 percent of it is devoted to infrastructure investment, only 8 percent to measures supporting consumption.

A genuine shift away from the old paradigm will require difficult economic and political choices and is sure to meet with opposition. Yet such a shift is undoubtedly in the long-term interest of the nation as a whole. A more consumer-centric economy would allocate capital and resources more efficiently, generate more jobs, spread the benefits of growth more equitably—and grow more rapidly—than China will if it remains on its present course. The narrowing of the trade surplus and the Chinese consumer’s larger contribution to global growth would make foreign ties more harmonious. In years past, China has demonstrated a remarkable ability to make major economic changes rapidly in pursuit of broad national objectives. It can do so again by shifting to a new economic paradigm that unleashes the spending power of its consumers.

Related Articles