It may be tempting to view recent declines in commodity prices as the end of the resource “supercycle”—the period of sharp price rises and heightened volatility since the turn of the 21st century. Yet rumors of the supercycle’s death are greatly exaggerated. Despite recent falls, commodity prices are still near their levels of early to mid-2008, just before the global financial crisis hit. (To track the movements in commodity prices over time, see the interactive, “MGI’s Commodity Price Index—an interactive tool.”) At a time when the world economy remains below full power, this phenomenon is striking, and a sign that the supercycle is alive and well.

Our first annual survey of resource markets was conducted by the McKinsey Global Institute and McKinsey’s sustainability and resource productivity practice. They found that a key reason for the price resilience appears to be higher marginal supply costs, which continue to rise for most commodities. While the world does not face any near-term absolute shortages of natural resources, the research finds that increasing supply will be a challenge. In particular, prices reflect three persistent forces: a challenging geology that makes it hard to extract resources and the technological supply-side innovations and resource-productivity improvements that counteract those challenges. All are having an impact:

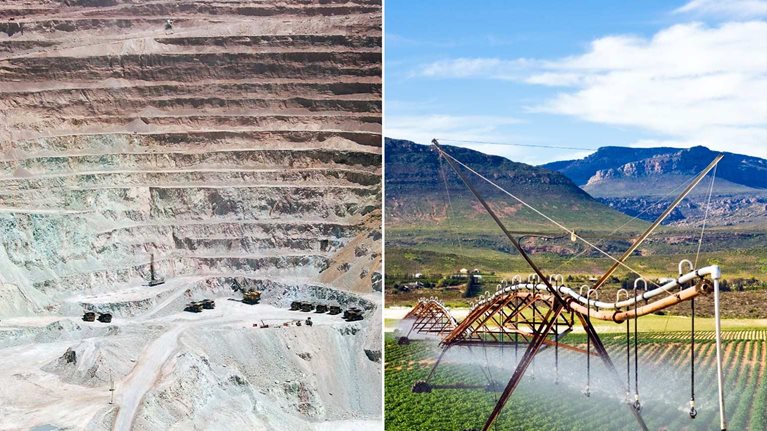

- Energy. With the notable exception of the 1970s, oil and gas prices (in real terms) were flat or fell throughout the 20th century. Yet energy prices have soared by an average of 260 percent since 2000 as a result of a combination of strong demand (notably from China) and rising supply costs. For instance, the average real expense of bringing a new oil well online doubled between 2000 and 2010—an increase of more than 7 percent a year. With the quality of traditional reserves deteriorating, production is now shifting to sources such as tar sands and deepwater oil, whose extraction is not only more complex but also more costly. Deepwater projects accounted for 24 percent of offshore oil wells in 2009, up from 19 percent in 2005, and measures required to protect the environment and worker safety are pushing costs even higher.

- Metals. While metal prices fell (in real terms) throughout the 20th century, they have jumped 176 percent since 2000. Many observers attribute the increase largely to demand from emerging markets, but McKinsey’s Basic Materials Institute finds that geological challenges and the rising cost of inputs, notably energy, have also boosted prices. In the case of gold, for example, more than 45 percent of the increase in supply costs between 2001 and 2011 resulted from geological factors that we believe will persist and an additional 30 percent from shortages of inputs, including equipment and skilled labor. In South Africa, formerly the world’s largest gold producer, mining companies must today dig several kilometers underground to extract reserves. The cost of extraction is likely to go on rising because operating expenses at existing mines are higher. With their rate of depletion now double the rate of demand growth, companies must increasingly access reserves that often are not only declining in quality but also in more challenging and risky locations.

- Food. Demand for food increased throughout the 20th century, but thanks to higher yields, prices fell (in real terms). Yet they have risen by almost 120 percent since 2000 as yield improvements slowed, demand for feed went up, and agriculture endured droughts, floods, and variable temperatures. The net result is that global buffer stocks are running low but demand for food, largely in Asia and Africa, is expected to go up by 35 percent during the next 20 years. In addition, higher production of biofuels is boosting demand for land. So is the fact that more than 20 percent of the world’s arable land has been seriously degraded through, for example, pollution and soil salinization. Finally, the land shortage is further exacerbated by the mass migration of people from rural areas to cities: urban sprawl could reduce the world’s cropland by two million hectares a year.

We believe that resource markets will be shaped in coming years by a race between emerging-market demand and the resulting need to increase supply from a more challenging geology and the twin forces of supply-side innovation and resource productivity. Innovations such as the use of 3-D and 4-D seismic technologies for energy exploration can improve access to resources. Productivity gains can reduce the wastage of food and water and make buildings more energy efficient. The question is whether technology and resource productivity can improve fast enough to counter the impact of emerging-market demand and a more challenging geology.

The race is on.

Related Articles

Mobilizing for a resource revolution

The commodity crunch in consumer packaged goods