As the global economy spirals into recession, retrenchment seems to be the order of the day for many high-tech companies. Our research, however, suggests that conventional downturn strategies many not serve them well. McKinsey analyzed the performance of nearly 700 such companies during contractions in markets around the world over the past two decades. We found that the turmoil accompanying downturns significantly reconfigures the high-tech landscape. About half of the companies that entered these downturns as leaders—the top 20 percent—ended up as laggards when the economy regained momentum. Our research underscores three essential findings for executives.

First, they should fully understand the dynamics and probable impact of the contraction. Revenue is (and will go on) declining, but the contours of the downturn will differ dramatically by subsector. Second, executives should know how liquidity issues may affect operations. As compared with other industries, the credit situation is stable in high tech. Problems are mounting along the supply chain, however—particularly among distributors and contract manufacturers—and in overseas markets. These developments could ultimately affect the operations of many companies. Third, high-tech executives should play offense, acting to strengthen the balance sheet and improve the competitive position. Our analysis shows that making obvious moves (for instance, cutting costs) as well as counterintuitive ones (such as increasing sales and marketing expenditures) quickly can improve a company’s position when the recovery begins.

Our broad study of the high-tech environment and economic cycles, covering a span of 20 years, provided the underlying macroanalysis for this article. To understand the factors that explain shifts in the competitive position of high-tech companies, we undertook a more focused analysis of the performance of publicly traded companies in 12 subsectors globally1 from 1995 to 2005—years that of course included the severe tech downturn of 2000–02. We ranked 688 companies by market-to-book value as well as return on invested capital (ROIC), and we categorized each of them as a “leader” (in the top 20 percent on both dimensions) or a “laggard” (the remaining 80 percent). We then charted how their market positions changed over the course of the 2000–02 recession and the recovery period: in other words, the transformation of leaders into laggards, of laggards into leaders, and so forth.

Each downturn, of course, has unique characteristics—namely, its pace and duration and how central the tech sector’s problems are to its origins and course. The underlying trends and prescriptive moves we discuss in this article are particularly relevant to the current economic contraction.

High tech = high pain

Only in the fall of 2008 did government economists officially recognize that the current recession had started earlier in the year. By then, many high-tech companies had already begun to react. Our analysis suggests why. From the peak to the trough of recessionary periods, spending on the goods and services that the high-tech sector generates traditionally drops four to seven times more than GDP does. In three of the past four major downturns, IT spending fell twice as much as GDP did; after the dot-com bubble burst, in 2000, IT spending fell by 27 percent, GDP by 3.7 percent (Exhibit 1).

Tech tumble

As the current downturn began, IT spending stood at 3.05 percent of GDP, below the 3.3 percent average of the past ten years and well below the 2000 peak of 4.1 percent, suggesting this downturn could be toward the lower end of this range. Some high-tech subsectors, however, will feel the slowdown more than others: for example, hardware—from laptops to components—will probably be hit much harder than security software or maintenance services, which are essential to keeping corporate IT departments running and where spending is less discretionary.

Expensive credit and ripple effects

As compared with companies in capital-intensive industries, such as consumer products and automotive and industrial equipment, most of those in high tech have enough cash to service their short-term debt. Yet although they may be relatively unscathed by the current credit crunch, they are not unaffected by it—particularly companies with high cash burn rates.

One in four high-tech companies, we predict, will have to tap into a credit line or refinance its debt over the next year. In some subsectors—such as the manufacturing of components, distribution, and manufacturing services—up to 50 percent of companies around the world will need funding (Exhibit 2). Already, the downturn has hit Asian contract manufacturers deeply: order flows are less predictable, and the cost of funding operations from credit lines is becoming prohibitive. These strains along supply chains and in sales channels will affect the operational latitude of a wide range of high-tech companies, affecting production, inventories, and customer relationships.

Liquid losses

A changing competitive position

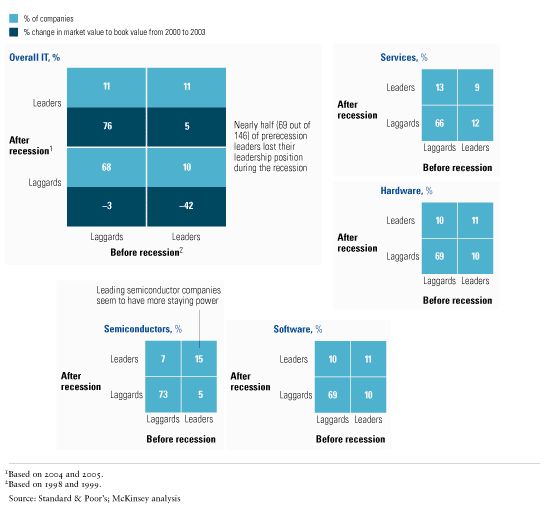

Our research shows that the competitive position of companies in the high-tech sector can change radically in a recession, depending on how well their executives understand its dynamics and take forceful action swiftly. We found, for example, that 69 of the 146 high-tech companies entering the 2000–02 contraction as leaders—47 percent—emerged from it as laggards (Exhibit 3). Conversely, 13 percent improved their positions during that same period. For example, the last downturn saw several leaders in various subsectors slip, from storage device makers and enterprise software manufacturers to virtualization and consulting-services firms. In contrast, companies such as Foxconn and HCL ascended. Even companies that remained in the same categories moved to the extremes: Cisco Systems and 3Com, for instance, continued to be a leader and a laggard, respectively, but Cisco’s performance improved while 3Com’s fell further (see sidebar, “Cisco: Exploiting a recession’s dynamics”). With so much change in the sector’s leadership, it’s not surprising that we found that the market-to-book values of leaders and laggards changed significantly—by 40 to 80 percent from prerecession values. The current crisis could exacerbate the sector’s volatility.

Trading places

Aggressive (but counterintuitive) action

Our research showed that five different kinds of decisive management moves improved the competitive standing of high-tech companies when they emerged from a downturn.

Manage working capital aggressively

By the end of the 2000–02 downturn, high-tech leaders had made their cash conversion cycle 23 percent shorter, shaving off two or more weeks of waiting time for capital to become available. A leading networking company, for instance, reduced its sales outstanding and accounts receivable by more than 40 percent, while a struggling competitor allowed its accounts-receivable cycle to balloon by 50 percent. For hardware manufacturers, increasing inventory turns and reducing actual inventory speeds up cash conversion. Both a leading semiconductor manufacturer and a top PC maker substantially decreased the number of days they held inventory—in the case of the PC maker, to just four.

Many companies we studied also used the downturn to drive down their cost bases by negotiating better pricing with suppliers and partners. Others entered into partnerships and joint ventures that allowed them to offload some costs or to garner a share of a lucrative market. Some companies that had a cash cushion and brought their expenses under control could offer financing to customers or suppliers, so that the borrowers sustained their operations and the lenders deepened their business relationships or won concessions.

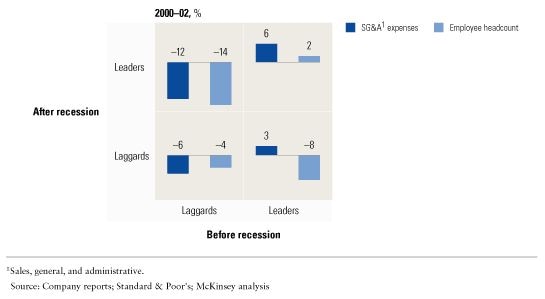

Rationalize SG&A expenses and overall headcount

The companies in our study managed their sales, general, and administrative (SG&A) expenses in a much different way than anything else we investigated. Controlling operating expenses is critical for all companies, but leading ones that maintained their positions in the 2000–02 recession actually increased their SG&A costs by 6 percent more, in absolute dollar terms, than leaders that lost their positions (Exhibit 4). Some leaders that maintained their leadership also raised overall headcounts by 2 percent; fallen leaders cut them by 8 percent. The growth in SG&A expenses and employees took place even as sales for most leaders declined by 5 percent. A leading software firm, for instance, increased its advertising expenditures from $1.23 billion in 2000 to $1.36 billion in 2001 as the market softened. And SAP ramped up sales and marketing spending by 19 percent in 2001, although it cut administrative expenses by 8 percent. In contrast, a software competitor that slipped somewhat cut approximately 2,000 sales and marketing employees.

Successful downsizing

Laggards that emerged as leaders took a different tack, trimming their SG&A expenses by 6 percent more than laggards that didn’t and reducing headcounts by 10 percent more throughout the recession. Although some leaders that maintained their position also instituted layoffs, these tended to be less steep and were concentrated early in the downturn.

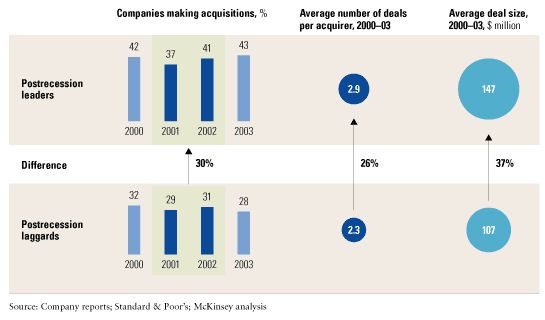

Make frequent, significant acquisitions

Companies that emerged as leaders invariably used the downturn to make significant acquisitions that strengthened the product portfolio. Their acquisitions were both more frequent and more substantial than those of companies that ended the 2000–02 recession as laggards: they were 30 percent more likely to make acquisitions and racked up 26 percent more deals. These companies also tended to wait until later in the downturn, when the valuations of their targets were most attractive (Exhibit 5).

Leaders prevail

Divest noncore assets early in the cycle

Despite this penchant for acquisitions, leaders also used the 2000–02 downturn to streamline the number of battlegrounds in which they competed. These companies, which were 50 percent more likely to divest noncore businesses than laggards, improved their overall positions in the remaining businesses.

With two notable exceptions—HP’s acquisition of EDS and Oracle’s string of acquisitions including BEA—2008 was a relatively slow year in high-tech M&A. Companies are playing a waiting game to see where this recession will take valuations. Buyers are counting on further declines in stock prices; sellers are unwilling, for the present, to deal in a fire sale, which is why Yahoo! rebuffed a Microsoft offer that would now be worth a hefty premium. We expect more aggressive M&A action in 2009.

Maintain a stable level of leverage relative to equity

Our research shows that maintaining or improving the debt-to-equity (D/E) ratio throughout the 2000–02 recession was a hallmark of high-performing companies; some leaders even managed to pay down debt. But the central point is that the D/E ratio of laggard companies increased on average by 950 basis points—almost doubling their level of leverage. Given the steep drop in technology spending during contractions, such escalating debt loads left these companies little room for investing in operational improvements, much less for acquisitions or developing new products.

Particularly in the case of laggards, uncontrolled leverage and heightened liquidity risk depress valuations just when the market-to-book ratios of all but the leading companies are falling, as generally happens in downturns. What’s more, even an effort to decrease leverage doesn’t guarantee survival: companies, such as Nortel, with relatively low debt ratios can suffer a drop in revenues so severe that cash flow turns negative and forces a reliance on cash reserves—and, in the end, insolvency. The debt loads of high-tech companies owned by private-equity firms are harder to gauge, but these are usually the most highly leveraged businesses, so they may be even more vulnerable. We therefore expect some of them to seek bankruptcy as they burn through cash and find additional funding too expensive or credit nonexistent.

Companies that correctly make the five kinds of moves discussed in this article may find themselves with new opportunities to increase their revenues. The most common strategy is to introduce new products, as have almost all hardware, software, and equipment companies that strengthened or maintained their industry leadership during past downturns. Some of these products, such as smartphones and Apple’s first iPod, met with spectacular success. Many companies also ramped up their R&D to focus on next-generation products that could provide high growth and high margins as IT spending picked up.

Are the five kinds of moves described here the only ones to consider? Of course not, since each downturn has a unique profile that makes other moves necessary and perhaps more valuable. Yet our findings do suggest that understanding the shape of past high-tech recessions, and taking well-timed moves of the type discussed in this article, should help companies withstand the more pernicious effects of downturns and capitalize on their very real opportunities.

Related Articles

Mapping decline and recovery across sectors