In late January, Roger Federer won his sixth Australian Open title. His tally of Grand Slam championships now numbers 20—an incredible feat. As tennis’s biggest star, he is well compensated for his efforts: Forbes magazine estimates that he took home $64 million last year.

Why does Federer make so much money? The answer, most would say, is clear: talent, hard work, good looks, business acumen.

But what if Federer played badminton? He would face Lin Dan, the champion in that sport. Each man may be the best ever in his respective game, and both are extremely marketable, with competitive instincts and personal charm. But Dan doesn’t make anywhere near what Federer does—and he never will. That’s because Dan has an “industry” disadvantage. A Top 10 tennis player makes 10 to 20 times what a Top 10 player in any other racket sport earns.

Likewise, a company’s choice of industry matters a great deal—more than many realize. When we tracked the economic profit of the world’s 2,393 largest companies over 10 years, we found that about 50% of a firm’s performance compared to the broader corporate universe is driven by what’s happening in its industry, highlighting that “where to play” is perhaps the most critical choice in strategy. Your industry trend is the single biggest factor shaping your odds of outperformance.

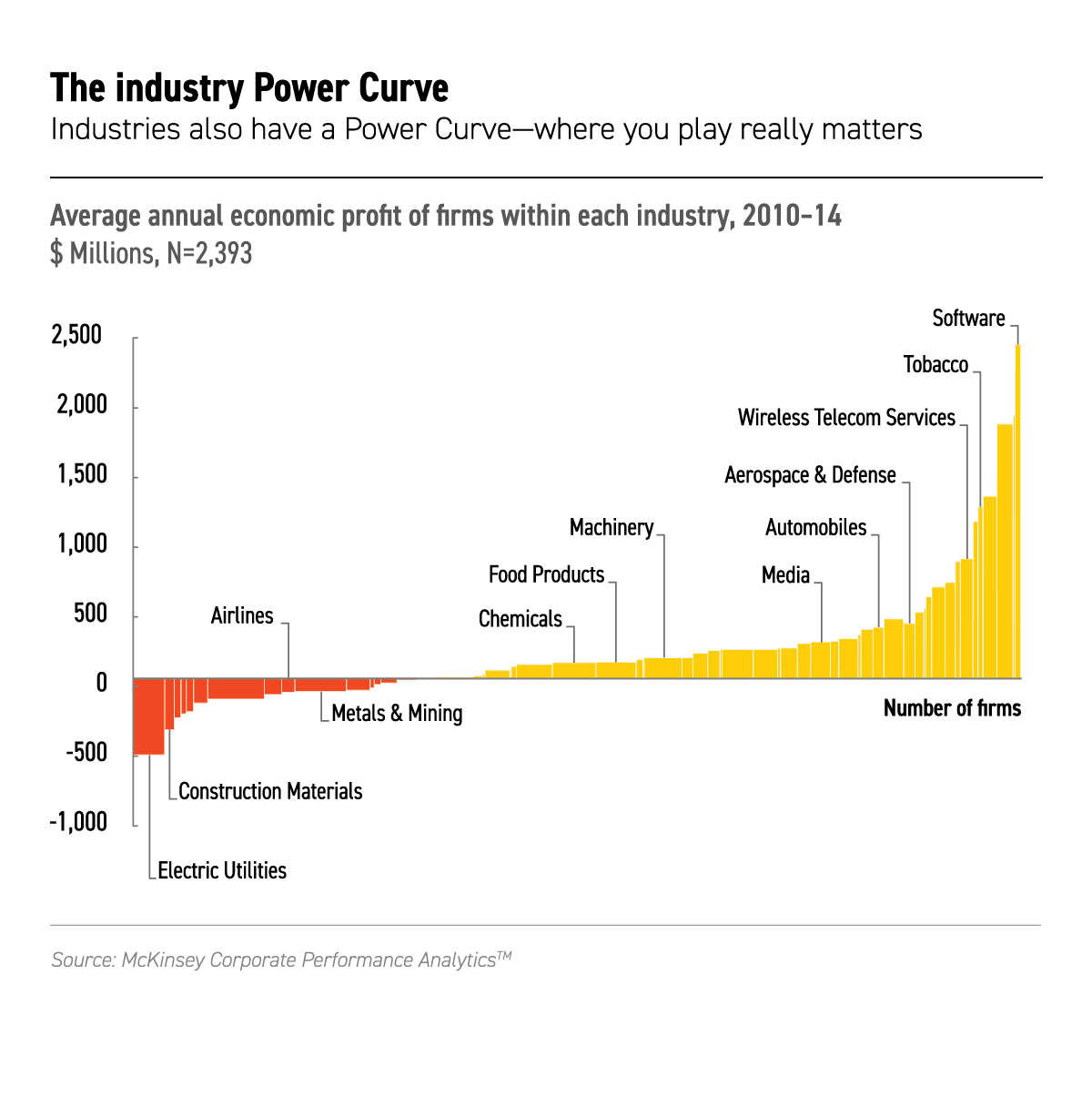

Take a look at the graph below, showing what we call the industry Power Curve:

The findings are striking. There are 12 tobacco companies in our research sample, and nine are in the top performance quintile. Yet there are 20 paper companies, and none is in the top quintile. Well-known high performers such as software, pharmaceuticals, and wireless telecommunications jostle for position among the top 20%, while utilities, transport, and construction materials lumber along in the bottom 20%.

The role of industry in a company’s position is so substantial that you’d rather be an average company in a great industry than a great company in an average industry. The median pharmaceutical company (India-based Sun Pharmaceuticals), the median software company (Adobe Systems), and the median semiconductor company (Marvell Technology Group) all would be in the top quintile of chemicals companies and the top 10% of food products companies.

In some cases, you’d rather be in your supplier’s industry than in your own. For example, the average economic profit of airlines is a loss of $99 million, while suppliers in the aerospace and defense category average a profit of $453 million. In fact, the 20th percentile aerospace and defense supplier, Saab AB, earns more economic profit than the 80th percentile airline, Air New Zealand. That is not to say that all airlines have poor economic performance (witness Japan Airlines), nor that all is rosy in aerospace and defense. But it is a fact of life that there are more and less attractive playing fields.

Industries as escalators

As a child, you may have tried to beat your parents up the escalator by running up the one going down. You had to run very fast just to keep up with them floating up. Industries are like that—either heading up and accelerating your progress, stuck on stop-mode so it’s only your effort that counts, or on a downward track, meaning you have to work hard just to say in place, let alone get ahead.

In our study, of the 117 companies that jumped from the middle quintiles to the top, 85 moved with their industry. Of the 201 that fell from the middle quintiles to the bottom, 157 were pulled down by their industry.

So, it’s crucial to both identify the relevant trends in your industry and to act on them in the right timeframe. You have to make the trend your friend. As the global economy moves through cycles, as new technologies and business models emerge and older ones die, as industry structures change and new ecosystems are formed, profit pools shrink and grow and move between industries. The results can sometimes be dramatic. For instance, wireless telecom jumped from near the bottom of all industries 10 years ago to nearly the top. The oil and gas business went the other way in the wake of the commodity price plunge.

If you’re enjoying a favorable industry trend—one of the key levers of performance, as I noted in my previous blog—you should ride that trend as hard as you can. If, however, you find yourself facing an industry headwind, you might need to seriously consider changing your industry—or changing industries.

Change your industry or change industries

Say your industry faces a major disruption. You have only two options: either transform your industry (through consolidation to shift its fundamental performance prospects, for example), or leave your industry to establish a new foothold in a less threatened space. Unfortunately, neither is easy.

If you’re going to stay in the same industry, you might need to find ways to alter its dynamics. For instance, the beer industry in Australia was a so-so performer decades ago until Lion and Foster consolidated it so thoroughly that it became a lot more attractive for both. Buurtzorg Nederland, meanwhile, changed the Dutch home healthcare industry and created an economic and social success story with a profoundly new and humane delivery model. What these companies have in common is that they committed to changing the game, executing strategies that dramatically altered the bases of competition in their industries and positioning themselves to capitalize on those changes.

If you can’t rewrite your industry’s rules, you may have to move into a different business. Successful industry changers shift more than 50% of their capital base over a 10-year period. Building the confidence to do so, hiring the right talent, and acquiring the necessary capabilities are tough mountains to climb, but in the face of overwhelmingly small odds of success in their current industries, some find that to be the only solution.

Likewise, if Lin Dan ever wants to snag the kinds of global endorsement deals that Roger Federer profits from, he may have no choice but to switch to another sport. Tennis, anyone?

Martin Hirt is a senior partner in our Greater China office, co-leader of our Strategy and Corporate Finance Practice, and co-author of Strategy Beyond the Hockey Stick with Sven Smit and Chris Bradley.

This article originally appeared in Quartz magazine