This article was a collaborative effort by Sven Smit, Martin Hirt, Ezra Greenberg, Susan Lund, Kevin Buehler, and Arvind Govindarajan, representing views from McKinsey Global Institute and McKinsey’s Strategy & Corporate Finance and Risk & Resilience practices.

In March 2020, we suggested that the imperatives of our time were the battles needed to flatten two curves: the curve of the viral spread and the curve of the economic shock. Today, after two terrible peaks of viral spread, and with the vaccine rollout progressing, some regions are finally close to flattening both curves. Many others have seen three or even four peaks; their situation remains difficult, and in some countries is as bad as it has ever been.

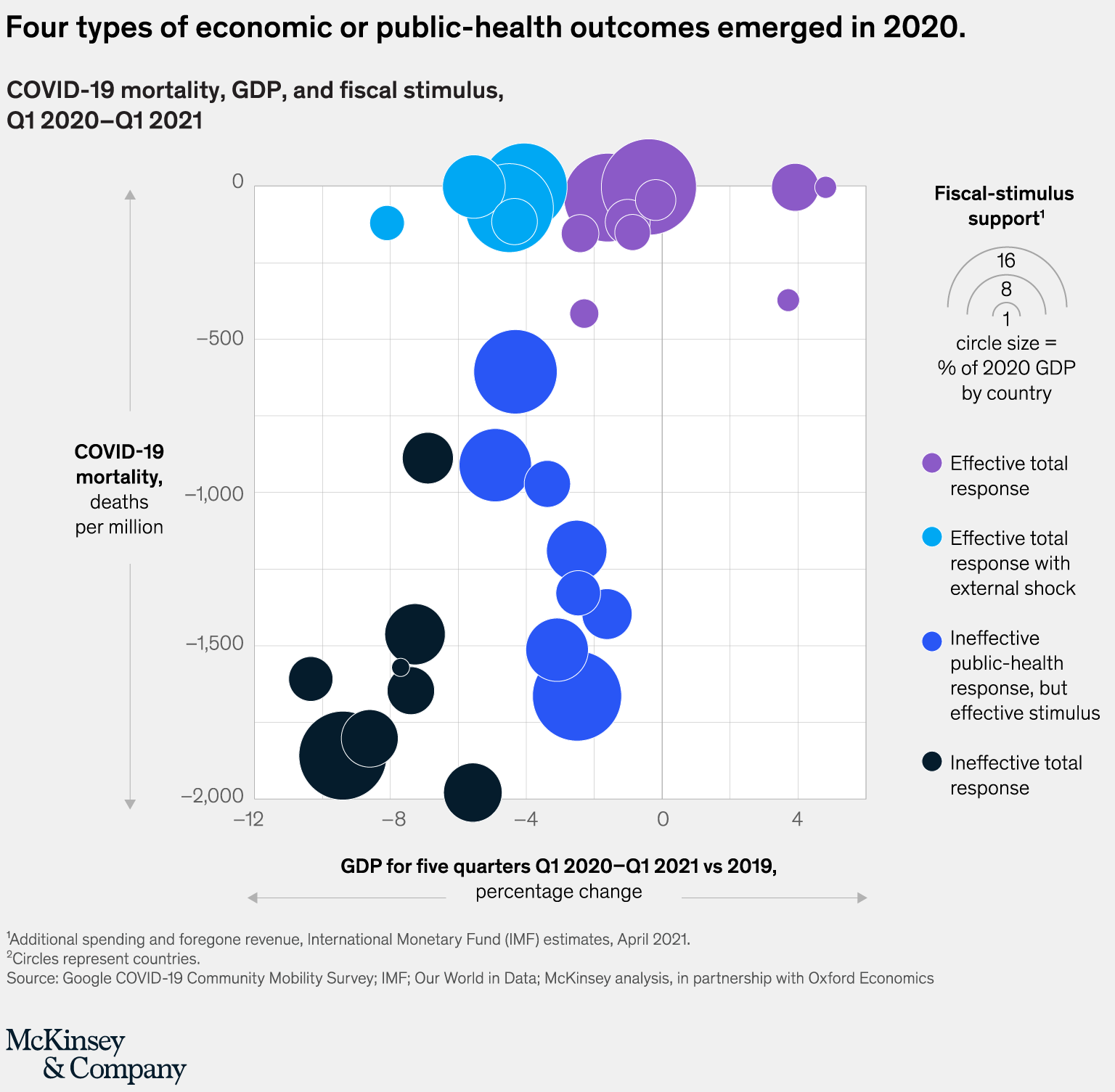

While some OECD countries managed to cap the exponential spread of the virus, they weren’t able to crush it. Depending on the effectiveness of their response, countries and regions wound up with distinctly different economic outcomes. In early 2020, there was a debate on the trade-off between the virus and the economy. At that time, we suggested that the question was off the mark: there was no trade-off. The facts are now clear: no country kept its economy moving well without also taking control over the virus spread.

To be clear, the battle is far from over. In many parts of the world, the pandemic is as bad today as it has ever been. But progress is tangible. COVID-19 vaccines were developed in record time, and they work. Furthermore, massive inoculation programs are now accelerating in many countries. Just as important: sentiment about vaccine adoption is improving. There have been setbacks, and risks abound; the formation of new virus mutations is of particular concern. Endemicity is almost certain in various parts of the world.

On the economic front, government support through fiscal and monetary policies has also unequivocally worked. Employment is recovering in all countries, though at different rates.

As a result, uncertainty is receding and losing the paralyzing grip it took in the early part of the pandemic.

The outlook for economic progress is brightening for countries leading the COVID-19 exit, with positive results now being reported for Q1. The virus still dictates the economy—Japan, which has experienced a recent resurgence and a set of lockdowns, reported negative growth in Q1. But its grip is easing. Even some countries that have yet to fully reopen, and are currently facing challenges, are likely to see strong headline GDP growth in 2021.

History suggests that there are essentially two types of economic expansions after recession: those that see GDP grow by 10 to 20 percent cumulatively in postcrisis years, and those that see 30 to 50 percent cumulative growth. Call them 40-percent recoveries.1 They don't happen by accident. They are the result of choices made by leaders in government and business and by individuals, families, and households.

Imagine a recovery that delivers 3 to 4 percent sustained global GDP growth over at least a decade. Such a recovery starts with a well-managed exit from the pandemic that masters the tricky hand off from demand led by government stimulus to private-sector-led spending, income, and job creation. Such a “prosperity for all” recovery would be propelled by increasing vaccination rates, accelerated digitization, transitions toward sustainability, significant reskilling and smart assistance to vulnerable populations, and other factors.

On the other hand, a near-term spending surge could easily prove temporary, returning the global economy to its pre-COVID-19 limitations of about 2 to 3 percent annual growth. In this kind of recovery, growth is held back by endemic COVID-19 in most countries; productivity gains that lead to layoffs rather than new jobs; halting transition to sustainability, and other factors.

To deliver on a new age of prosperity for all, the global economy will have to deal with two concerns raised as part of the debate about “going for growth.” One worry is the potential for higher inflation; the other is that newly accumulated debt will become unsustainable and constrain growth. Both are a possibility—but both can also be dispatched.

We are seeing price increases and higher wages in many geographies and markets and will likely see more as supply scrambles to catch up with surging demand. But as major central banks have continued to emphasize, these near-term shifts are not expected to turn into an ongoing inflationary threat.

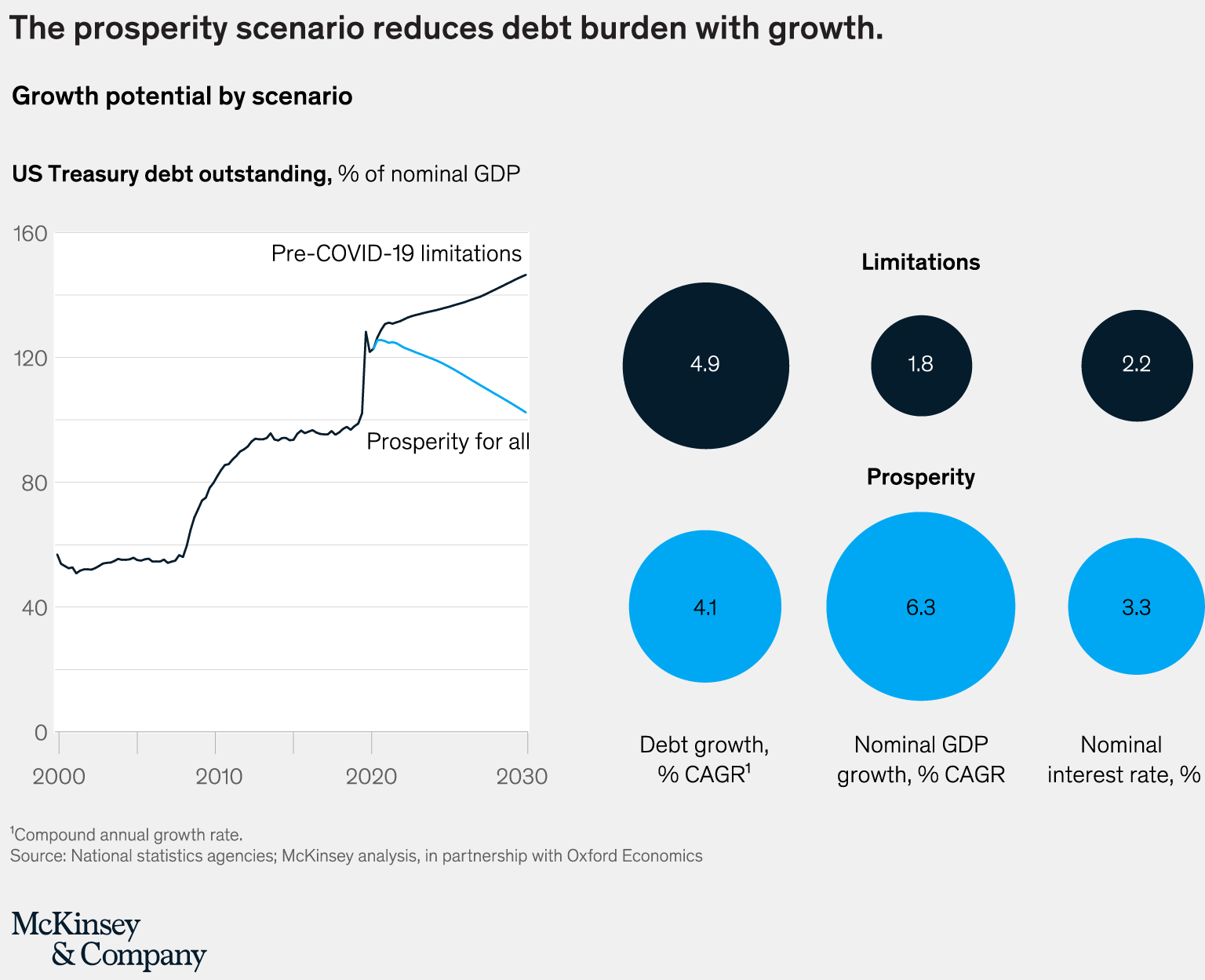

Problems from a debt overhang are not inevitable. In the United States, for example, outstanding debt in 2020 reached 133 percent of GDP, topping the previous record of 123 percent in 1946, just after World War II. But in the postwar years, and in many other examples over time, the debt burden was reduced by driving nominal growth, not by cutting debt.

Similarly, in a new age of prosperity for all, the debt burden could again fall, as nominal GDP growth exceeds debt growth and the nominal interest rate.

The benefits of the high-growth scenario would be widespread. Global GDP would rise to about $122 trillion by 2030, 45 percent above the $84 trillion recorded in 2019—a strong acceleration even when compared with our pre-COVID-19 trajectory. A bigger global income does not by itself solve the problems of equality and sustainability, but it opens a wide range of possibilities for governments to consider. With it comes a hope to alleviate some of the societal tensions and polarization that have become common within and across countries. Similarly, faster economic growth need not slow down the drive toward sustainability; it might even accelerate it as we mobilize the investment required to make the transition to clean energy.

If global leaders set the expectations that these outcomes are possible, and act on them, then the world could be on the cusp of a new age of prosperity: an economic recovery that will add 30 to 50 percent to GDP over the next decade, with better quality of life for more people and a more sustainable future for the planet. If not, then the recovery could end up adding only 10 to 20 percent to GDP, less equitably distributed, less sustainable, and with worse outcomes for global health and the environment.

The trauma of this pandemic will be with us for a long time to come. The big question for humanity is whether we can now turn this crisis into a moment of pivot, where we harness the innovations, the new insights, and the crisis-fortified determination to improve the world. The time for these choices is now. It’s up to all of us whether we will move into the 2020s with a new paradigm for safeguarding lives and livelihoods: a new age of health and prosperity for all.