The astonishing election upset in India has put the future of its economic-reform program in question. With the victorious Congress Party depending on Leftist parties for parliamentary support, uncertainty is running high about the future of the country’s privatization, deregulation, and foreign-investment reforms.

Voters have sent a clear message about the need for broad-based economic growth that lifts all boats. But some members of the winning coalition may well misinterpret that message. India’s recent experience—and that of its Asian neighbors—shows that continuing rural poverty stems not from too much economic reform but rather from too little. Since liberalization began, in 1991, annual GDP growth has been twice as high as it had been previously. As a result, poverty rates have fallen by nearly a third in both rural and urban areas. The celebrated software and outsourcing industries are only the latest evidence of the effectiveness of the reforms, which have created hundreds of thousands of high-paying jobs and generated billions in export revenues.

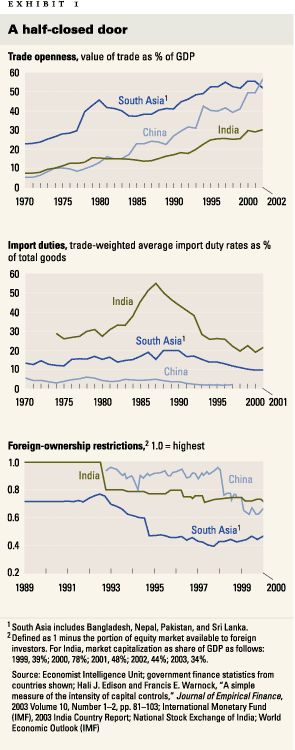

The challenge facing the new ruling coalition is to extend the success of the IT and outsourcing industries into the broader economy. To that end, foreign investment and global competition must be allowed to reach more sectors, including some in which the government now plays a significant role. Although India has broadly cut import duties and increased foreign-ownership limits over the past ten years, large parts of the economy remain sheltered by high tariffs and restrictions on foreign direct investment (Exhibit 1), which amounts to just 0.7 percent of India’s GDP, compared with 4.2 percent in China and 3.2 percent in Brazil. Imports total less than $70 billion—a small fraction of China’s $413 billion.

New research by the McKinsey Global Institute indicates that the foreign direct investment that did find its way to India has had an overwhelmingly positive impact. The introduction of foreign competition in IT, business-process outsourcing, and the automotive industry has prompted Indian companies to revamp their operations and boost productivity, and some have become formidable global competitors. Thousands of new jobs have been created in these industries. Consumers benefit from lower prices, better quality, and a wider selection of products and services, while domestic demand has soared in response to lower prices.

The task now is to build on the current momentum by replicating these successes across the economy. Earlier MGI research found that product market regulations, the lack of clear land titles, and pervasive government ownership were preventing India from achieving 10 percent annual GDP growth. MGI’s latest research shows that the country must go further in lowering trade and foreign-investment barriers if it is to continue integrating itself into the global economy.

Shining stars

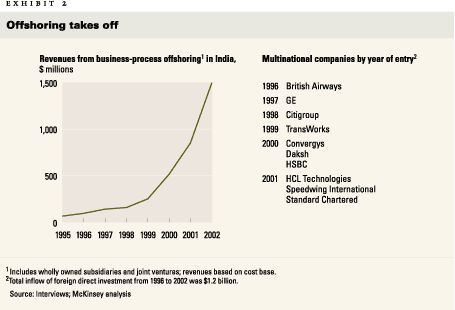

India’s $1.5 billion outsourcing business illustrates how foreign investment and trade have benefited the country. Along with IT and software, business-process outsourcing is perhaps the most open sector. In 2002, it attracted 15 percent of total foreign direct investment and accounted for 10 percent of all exports. By 2008, it is expected to attract one-third of all foreign direct investment and to generate $60 billion a year in exports, creating nearly a million new jobs in the process.

Without early investments by multinational companies, the outsourcing industry probably would never have emerged (Exhibit 2). Pioneers such as British Airways and GE were among the first to see the opportunity to move IT and other back-office operations to India. The success of these companies demonstrated to the world that the country was a credible offshoring destination. The multinationals trained thousands of local workers, many of whom transferred their skills to Indian companies that sprang up in response. Although Indian outsourcing firms now control over half of the intensely competitive global IT and back-office outsourcing market, all of the leading ones started as joint ventures or subsidiaries of multinational companies or were founded by managers who had worked for them.

Of course, allowing foreign investment in an industry that has no large Indian companies was relatively painless. It is far harder to put local incumbents in the line of fire. Yet India has done so in its automotive industry, with impressive results. Until 1983, high tariffs and a ban on foreign investment shielded government-owned automakers—such as, Premier Automobiles Limited (PAL)—from global competition. Local incumbents produced just two car models, both based on antiquated technology, between them, and charged high prices. In 1983, Suzuki Motor was allowed to take a minority stake in a joint venture with Maruti Udyog, another government-owned enterprise, to produce passenger cars. The new competition forced the incumbents to respond. Within a few years, eight Indian car models were in production, and all of them—including those from PAL—were of better quality than the cars produced before this liberation took place.

In 1992, the government lifted many of the remaining barriers to foreign investment in the auto industry. Nine additional foreign carmakers responded, and today competition is stiff. As a result, labor productivity has increased more than threefold, in part because PAL has been forced out of business. Prices have fallen steadily by 8 to 10 percent annually in all market segments, unleashing a burst of consumer demand. Despite higher productivity and the closure of PAL, employment has held steady and workers have benefited from higher wages.

Today, India’s $5 billion auto industry is expanding by 15 percent a year—one of the world’s fastest automotive-industry growth rates—and produces 13 times more cars than it did in 1983. This year, Tata Motors will make history by exporting to the United Kingdom 20,000 cars to be sold under the MG Rover brand—a feat no one would even have dreamed of just a decade ago, given the quality of Indian cars at the time. In view of the greater competitive intensity in the market, India may be better positioned than China is to become a global low-cost auto-manufacturing base. None of this would have been possible had India’s carmakers remained isolated from the world.

Hiding behind trade barriers

The dynamic growth and competitiveness of India’s outsourcing and automotive industries stand in contrast to most of its economy, where continuing restrictions on foreign investment and trade dampen competition and help inefficient companies survive.

Another sector, food retailing, illustrates how Indian industry fares when foreign investment is banned entirely. Labor productivity, for instance, is a mere 5 percent of US levels, in part because street markets and mom-and-pop counter stores account for 98 percent of the market, modern store formats (like supermarkets and hypermarkets) for just 2 percent. But productivity averages just 20 percent of US levels even in Indian supermarkets as a result of their small scale, poor merchandising and marketing skills, and inefficient operations. In other emerging markets, including Brazil, China, and Mexico, global retailers such as Carrefour and Wal-Mart Stores have intensified competition and increased productivity. If these retailers could invest in India, improved Indian supermarkets could, we estimate, offer prices 10 percent lower than those of traditional grocery stores. Indian consumers across the social spectrum would benefit, and as many as eight million new jobs would be created.

Getting the full benefit of foreign investment calls for competition within industries, since it forces companies to improve their operations and innovate. Many forms of protection and regulation can stifle competition and thus limit the impact of foreign investment. The consumer electronics industry is a prime example. The government lifted foreign-investment restrictions in the sector in the early 1990s. From 1996 to 2001, foreign direct investment in it averaged $300 million annually—20 percent of the total for India—a large sum, although just 8 percent of the consumer electronics investment going to China and just half of the investment going to Brazil and Mexico. Still, the entry of multinational players has boosted the local industry’s productivity and given Indian consumers more choice and lower prices.

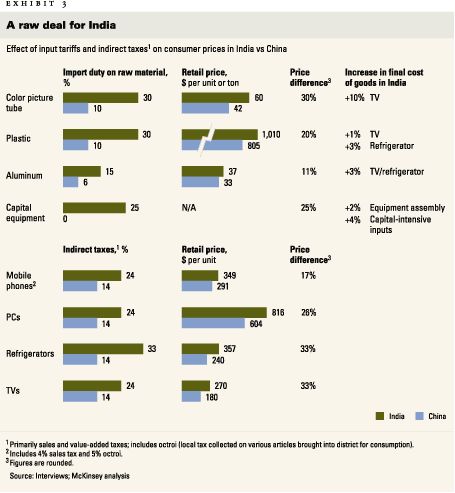

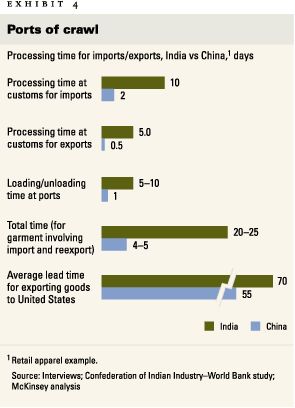

Despite these gains, consumer electronics goods made in India still can’t compete internationally, and the country’s consumers pay unduly high prices for them. The industry’s average labor productivity is only half of Chinese and 13 percent of South Korean levels. Tariffs, taxes, and regulations are the main culprits. Tariffs of 35 to 40 percent on finished goods keep out imports and allow inefficient companies to continue operating. They also force even the best manufacturers to operate with subscale plants when, as usually happens, Indian demand doesn’t justify larger scale. Tariffs on inputs and indirect taxes (mostly sales and value-added taxes) add substantially to the price of final goods, further limiting demand (Exhibit 3). Meanwhile, labor laws that prevent the rationalization of plants and limit the use of contract labor increase production costs for both foreign and domestic companies. Red tape in getting export licenses and inefficiencies in India’s ports make exporting finished goods prohibitively expensive (Exhibit 4).

These same problems limit foreign investment and prevent many industries—including banking, heavy industry, and textiles—from reaching their full potential. Ultimately, consumers and workers pay through higher prices and the anemic pace of job creation.

Going global

India has clearly benefited from closer integration into the global economy in industries such as automotive, business-process outsourcing, and IT. To build on that success, the government must now lower trade and foreign-investment barriers still further.

First, tariff levels should be cut to an average of 10 percent, matching those of India’s neighbors in the Association of South East Asian Nations (ASEAN). Although progress has been made on tariffs, the Indian government still prohibits imports of many goods and protects inefficient companies from foreign competition. To give those companies a chance to improve their operations, the government might first lower duties on capital goods and inputs. Then, over several years, it could reduce them on finished goods.

Foreign-ownership restrictions should be lifted throughout the economy as well, except in strategic areas, notably defense. At present, foreign ownership is not only prohibited altogether in industries such as agriculture, real estate, and retailing but also limited to minority stakes in many others, such as banking, insurance, and telecommunications.

India’s government should also reconsider the expensive but often ineffective incentives it offers foreign companies to attract foreign investment, for these resources would be put to better use improving the country’s roads, telecom infrastructure, power supply, and logistics. What’s more, MGI research found that the government often gives away substantial sums of money for investments that would have been made anyway. (To give one example, it has waived the 35 percent tax on corporate profits for foreign companies that move business-process operations to India, even though the country dominates the global industry.) Moreover, state governments often conduct unproductive bidding wars with one another and give away an assortment of tax holidays, import duty exemptions, and subsidized land and power. Yet MGI surveys show that foreign executives place relatively little value on these incentives and would rather see the government invest resources in the country’s poor infrastructure.

Finally, interviews with foreign executives showed us that India’s labor laws deter foreign investment in some industries. It is no coincidence that software and business-outsourcing companies are exempt from many labor regulations, such as those regarding hours and overtime. Executives tell us that without these exemptions, it would be impossible to perform back-office operations in India. To attract foreign investment in labor-intensive industries, the government should therefore consider making labor laws more flexible.

Some Indian policy makers might argue that the reforms proposed here would undermine long-held social objectives, such as creating employment. But the evidence shows that regulations on foreign investment, foreign trade, and labor have actually slowed economic growth and lowered the standard of living. A decade ago, India’s per capita income was nearly the same as China’s; today, China’s is almost twice as high.

India’s economy has made real progress, but further liberalization will be needed to sustain its growth. The country now has 40 million people looking for work, and an additional 35 million will join the labor force over the next three years. Creating jobs for all these Indians will require more dynamic and competitive industries across the economy. Opening up to foreign competition, not hiding from it, is the answer.

Related Articles

India’s path from poverty to empowerment

The rediscovery of India