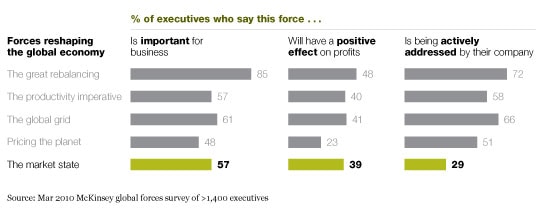

While we expect the steady advance of market capitalism to continue, the state—far from withering away—is likely to play an ever-larger role over the next decade, for three reasons.

First, even before the financial crisis hit, governments everywhere found themselves increasingly called upon to mitigate the sometimes negative impact of globalization on individual citizens.

Second, the crisis itself has prompted large-scale direct government intervention, both through fiscal stimulus and calls for increased regulation. That tilt in the power balance has been reinforced in much of the world by the perceived failings of the US-led free-market model and the success so far of a Chinese model that, while market-oriented, assumes that the state’s guiding hand will stay firmly clasped around many levers of power.

Third, the spread and dispersal of economic power around the world is making it harder to reach consensus on multilateral approaches to setting the rules of the global game. Bilateral and regional deal making is increasingly common, and these more local arrangements will remain largely market-based. Yet for business, this continuing shift away from a single set of rules will inevitably make it more challenging to seize opportunities globally. It will also require companies to engage across many fronts with many critical regional and national government actors.

Business executives, of course, face no shortage of challenges. But the tensions confronting policy makers in the coming years are truly daunting. On the one hand, states have been charged with driving prosperity by fostering economic growth and job creation. Most of them understand that this goal requires a strong role for the market rather than a reverse march toward command economies (hence our term, “market states”). On the other, governments must also ensure social stability and maintain social-safety nets. What’s more, they must accomplish these ends for citizens who continue to live within distinct national borders, even though those citizens’ ultimate fortunes will be hugely influenced by transformative shifts in flows of capital, goods, labor, and information that recognize no borders. How governments respond to these pressures, both individually and collectively, will do more to shape outcomes over the next decade than the actions of any other single kind of economic actor.

Let’s drill into the complications. In the developed world, virtually all major economies are struggling with expanded claims for government services, rising debt-to-GDP ratios, and looming entitlement time bombs. Debt levels in OECD1 countries will, on average, likely rise to 120 percent by 2014—up from less than 80 percent today. In emerging economies, governments may enjoy better demographics, but their aspiring citizens and growing economies demand huge investments in physical and social infrastructure—from roads to education to health care—if they are to avoid social disruptions and build thriving 21st-century economies.

Then there’s this consideration: over the past 100 years, an income inequality gap split the world into two large camps—Western economies buoyed by an increasingly prosperous middle class, and other nations caught in a seemingly endless cycle of poverty. Now, while inequality among nations (and across this former divide) is thankfully shrinking, the gaps between rich and poor within individual nations are widening.

While overall standards of living have risen across the globe, the gap between rich and poor has grown in almost three-quarters of OECD countries over the past two decades. Inequality is rising even faster in emerging markets: in China, it is increasing more quickly than in any Western economy.

This shift is partly structural. As economies develop, overall living standards tend to rise but so does income inequality. Manufacturing economies tend to be less equal than agrarian ones, service-based economies less equal than manufacturing ones. (The Gini coefficient—the measure of the difference between top and bottom earners—is two-thirds higher for service sectors than manufacturing sectors, and 150 percent higher for service sectors than agrarian sectors.)

Globalization further compounds the problem—and not in ways that are intuitive. Trade, though often blamed for aggravating income inequality, is not the key culprit. Instead, the rate of technology adoption is by far the biggest driver, accounting for more than three-quarters of the impact, mainly by automating away many low-skill jobs. The shortage of knowledge workers and capital deepening (which increases the productivity of top talent, hence raising its earning potential) accentuate the problem by causing salaries for top earners to soar.

The effect can be eye-popping. While a US unemployment rate topping 10 percent has drawn headlines in the current recession, the reality is starker. The unemployment rate in the top income decile of the population is barely 3 percent, but in the bottom decile, it’s ten times higher—more than 30 percent. Upward of a third of the US unemployed are now considered to be long-term (or structurally) unemployed and thus unlikely to rejoin the workforce any time soon.

While the gaps in Europe and Japan are generally smaller—Spain is a notable exception, with unemployment now approaching 20 percent—these nations pay a price. Estimates suggest that Germany and Japan, for example, have given up over a point of GDP growth a year for at least the past decade as a result of labor and taxation structures designed to produce a more robust safety net. In other words, to ensure a more equal society, they give up a third of the potential growth they could achieve each year.

Income volatility is another key issue. Despite the “great moderation”—the decline in overall economic volatility in the years preceding the recent downturn—the volatility of individual incomes has actually been increasing. In the United States, from the 1970s to 2008, it rose by as much as one-third. On average, 15 percent of US households can now expect their incomes to fall by as much as 50 percent each year. This isn’t just a US issue: more than 50 percent of middle-class Brazilians worry that they are at risk of losing their jobs or otherwise seeing their incomes plummet.

The bottom line: risk is shifting to individuals in a market-driven global economy—and governments are increasingly responsible to help pick up the pieces.

Businesses need to recognize that governments bear the burden of legitimate challenges—and work in partnership to help solve them

In such a world, companies can no longer shrug off policy makers and legislators as interfering meddlers to be managed. Governments are facing legitimate and difficult decisions and will be forced to make trade-offs. Business leaders would do well to acknowledge these problems and to work with governments to help solve them. The risk of a populist antibusiness backlash is high—and companies will need to continue to earn “the right to operate” in relatively unconstrained, probusiness environments.

Successful business leaders already recognize this reality. Wal-Mart Stores, for example, has worked alongside national and local governments, as well as other stakeholders, to help reshape US health policy. Innovative approaches born of the effort, such as the company’s $4 prescription plans and in-store clinics, are helping to reduce the cost of health care delivery in the United States, while also helping Wal-Mart’s customers and employees to pay less for care.

Helping governments to improve the public sector’s productivity will not only save them money but can also generate profits for the providers

Some of the most agile businesses will turn the ability to help solve the state’s challenge into an opportunity. As the tax base for many governments shrinks and burdens grow, states too face a productivity imperative: how to increase services and decrease costs. Governments have been notoriously bad at adopting the lean processes and IT improvements that have driven years of productivity gains in the private sector. Creative approaches by businesses to help solve the public sector’s problems will be part of the solution. In Spain, the health insurance provider Adeslas is partnering with the provincial government of Valencia to run hospitals and clinics more efficiently. In the United Kingdom, when the British Airport Authority built Terminal 5 at Heathrow Airport, it created an incentive plan to get private suppliers to finish the project faster and under budget. (And that example showed both how these new approaches can be successes and also hit bumps along the way—more than 50,000 pieces of luggage got hung up when the terminal opened, as baggage systems worked out kinks.)

States will be competing for jobs and growth, and selecting the right nations to partner with can be a competitive advantage for companies

While politicians will continue to be pressured by—and may sometimes pander to—the antibusiness backlash, most governments will continue to see working well with business as the best way to resolve their biggest dilemmas. Just as businesses need to recognize the legitimate challenges facing governments, governments must recognize the legitimate role businesses must play in contributing to the solution. After all, only a strong, expanding private sector can provide the revenue required to meet the state’s burgeoning needs. More and more, countries will be competing for investment and wooing enterprises to generate jobs and growth.

Two cases in point: Poland has recently created special tax breaks for companies relocating operations there, and both HP and IBM have put centers in Wroclaw to take advantage of these provisions. Similarly, Singapore’s government has invested heavily in education and training in an effort to attract investment by leading multinational firms and also offers subsidies to companies locating there. As corporations think about where to invest, build factories, locate offices, and source talent, they should explore such opportunities actively.

In an interesting twist, governments sometimes turn to private-sector businesses to enhance their prospects of attracting more private-sector business. For example, the city of Shanghai enlisted the employment-services firm Manpower to help it qualify entrepreneurs for government subsidies.

Global companies need to learn to work within and across multiple—and often divergent—regulatory environments

As companies expand globally, they will need to become even more sophisticated about navigating an increasingly complex regulatory landscape. Take financial services as an example. In Europe and the United States, banks have traditionally been managed as a profit-maximizing industry—an approach that has generated no end of second-guessing given the tumultuous outcomes of the past two years. By contrast, banks in Asia have, in effect, been treated as capital-providing utilities. However these regulatory regimes evolve, they will not soon converge.

Google’s recent challenges show just how hard it can be to drive a global business model while coping with widely different political and social cultures. In China, the company has strongly reasserted its own right to privacy, maintaining that data stored on its servers cannot be probed by the state. Meanwhile, in Italy, Google executives have been convicted for impinging on the privacy rights of others; several executives received suspended jail sentences for providing a platform, via YouTube, that allowed individuals to post videos with no oversight from the company.

Information standards, such as those for safety and labor, will remain fragmented and variable across countries and regions. Continued globalization will not homogenize cultural norms and expectations. Yet, as the global grid expands, the reaction and interaction from a single misstep in one country will ripple at the speed of light to more and more places, in new ways that will make the earlier experiences of companies such as BP and Nike seem relatively simple. Companies will need to become even more proactive and dynamic to cope effectively.

Finally, if national governments feel challenged, the multinational institutions established under US leadership after World War II—the traditional enforcers of the “Washington consensus”—are doubly challenged. With little true authority, they struggle to gain agreement from an expanding group of key global players with divergent interests. That’s why the Doha Development Round of trade talks has been in limbo since 2001, despite the ongoing struggle to revive it. Efforts at coordinated regulation on issues as diverse as intellectual property, environmental protection, and capital markets may well see important progress on some fronts, but achieving large-scale solutions will continue to be a daunting task.

Business leaders must recognize their vested interest in the success of the state—perhaps the biggest risk of all is its failure to meet its challenges

Business executives should wish the leaders of aspiring market states well, wherever their leaders may fall on the light-versus-heavy-touch spectrum of government intervention. The reason is simple and compelling: no single factor is more likely to reverse the global economic expansion than a widespread failure by these states to meet the challenges that face them. This threat cannot be taken lightly. Suboptimal policy choices will dampen economic growth; bad choices could, in the worst-case scenarios, threaten geopolitical stability and this may well be the biggest macro-risk business faces in the decade ahead.

The impact of global forces on business

Related Articles

Global forces: An introduction

The great rebalancing