To sustain wealth creation, developed nations must find ways to boost productivity; product and process innovation will be key.

See our newest take on productivity in "2024 and beyond: Will it be economic stagnation or the advent of productivity-driven abundance?"

Emerging markets are riding a virtuous growth cycle, propelled by larger and younger working populations. In the wealthy nations of the developed world, by contrast, low birthrates and graying workforces will make it enormously difficult to maintain what economist Adam Smith called “the natural progress of opulence.”

These countries’ best hope for keeping the wealth creation engine stoked is improved productivity—producing more with fewer workers. Paradoxically, doing that well across an economy is also the only way to generate lasting employment gains. In the United States, for example, every point of productivity-led GDP growth has historically generated an incremental 750,000 follow-on jobs.

The great tension here arises at the level of politics. Over time, the world’s rebalancing demands greater consumption and lower savings among the large developing countries, even as developed ones, the United States foremost among them, save, invest, and export more. Fostering policies that raise productivity, and avoiding or altering polices that impede it, will help ensure a smooth transition. Getting this wrong—failing to generate at least modest and broad-based continued income and employment gains in developed countries—raises the odds of a political backlash that will hurt the citizens of wealthy nations and of those moving up the wealth curve alike.

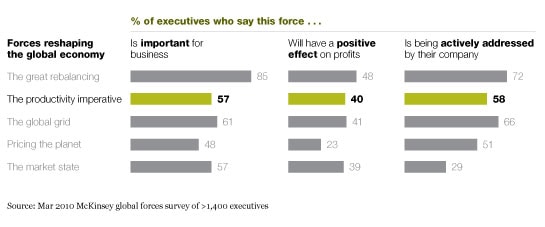

We call the productivity challenge an imperative because the need is so compelling. But to eke out even modest GDP increases, OECD1 nations must achieve nothing short of Herculean gains in productivity. In the 1970s, the United States could rely on a growing labor force to generate roughly 80 cents of every $1 gain in GDP. During the coming decade, assuming no dramatic increase in hours worked, that ratio will roughly invert: labor force gains will contribute less than 30 cents to each additional dollar of economic growth. To maintain a GDP growth rate of 2 to 3 percent a year, productivity gains will have to make up the other 70 percent.

The challenge is even greater in Western Europe, where no growth in the workforce is expected. Here, in other words, 100 percent of GDP growth must come from productivity gains. And in Japan, the hurdle is higher still: because of a shrinking labor force, each worker will have to increase output by 160 yen to generate an additional 100 yen of growth.

To complicate things further, we are seeing a growing talent mismatch. The Western economies have built a workforce optimized for mid-20th-century national industries, yet the jobs now being created are for 21st-century global ones—we need knowledge workers, not factory workers. And there just aren’t enough of the former. Anywhere. Companies across the globe consistently cite talent as their top constraint to growth.

In the United States, for example, 85 percent of the new jobs created in the past decade required complex knowledge skills: analyzing information, problem solving, rendering judgment, and thinking creatively. And with good reason: by a number of estimates, intellectual property, brand value, process know-how, and other manifestations of brain power generated more than 70 percent of all US market value created over the past three decades.

Western economies can do many things to change the equation. Deregulation has often raised productivity in the past and can continue to do so. Changing the boundaries around the work–life balance—encouraging people to stay in the workforce longer or increasing the numbers of hours worked each week—could add a few points of absolute growth too. Improving education is a no-brainer.

Businesses can and should advocate these and other policy changes that could have a long-term impact, such as easing immigration restrictions. But in the end, the real game changers will be breakthrough innovations created by companies: history shows that a majority of productivity growth—more than two-thirds—comes from product and process innovation.

The productivity economy will reward ‘do it smarter’ companies that build a better business model

Besides providing powerful incentives for companies to deliver their traditional products and services more efficiently, the new environment may make selling productivity—finding marketable ways to “do it smarter”—the most transformative business model of the next decade.

This push is bound to have a “no pain, no gain” dynamic. Innovation, by definition, is a disruptive process. Think about the book-publishing industry. Only two years after the release of the Kindle, Amazon.com now sells half of its books electronically for the titles it offers customers in both bound and digital formats. The Kindle is short-circuiting the entire physical supply chain, and Apple’s new iPad is sure to accelerate that process.

Something similar is shaking up the world of computing. It’s considered the poster child of productivity—and for good reason. But probe further and it’s not hard to find evidence of waste. Companies spend, on average, 5 to 10 percent of their total revenues on IT. Yet reliable estimates suggest that upward of 70 percent of server capacity goes unused—even more at midsize and small companies, since they can’t achieve scale. Advances in “cloud computing” (sharing computer resources remotely rather than storing software or data on a local server or PC) have vast potential to raise utilization rates and simultaneously help companies to increase their computing capacity, while slashing IT costs by 20 percent or more. Little wonder tech giants as divergent as Google, IBM, and India’s Wipro Technologies are investing furiously to win the battle for the cloud.

Health care is another arena where do-it-smarter businesses will thrive. On average, health care spending in OECD countries has outpaced GDP growth by nearly two percentage points a year, and even more in the United States. Still, in most countries, increased health care spending actually creates a productivity drag on the economy overall, because the sector has lagged behind in adopting productivity measures. (To take just one indicator, health care organizations spend, on average, only 20 percent of what financial-services companies do on IT.)

But multiple innovations promise to improve outcomes significantly while reducing costs. For example, some 75 percent of health care spending in many OECD countries pays for chronic-disease management. France Telecom’s Orange is partnering with health care providers to offer services that constantly monitor diabetics and cardiac patients remotely. Low-cost mobile-monitoring devices ensure better compliance with treatments and reduce the number of high-cost, life-threatening events. Germany’s T-Systems has linked up with the health insurance provider Barmer to provide mobile systems that track and monitor exercise patterns, so patients—and doctors—can monitor progress and reduce risk more effectively.

A raft of industries and services are poised to benefit from productivity improvements. Huge gains could be extracted just by applying the insights learned over the past 15 years in the most productive sectors, such as telecoms and financial services, to less productive ones, such as health care, education, and government.

The best companies will learn how to maximize returns from people who think for a living

Just as the early 20th century saw the development of management theory for improving the productivity of factory workers, the 21st century will see the evolution of myriad better techniques for managing people who think for a living.

The potential stakes are enormous. Companies that have higher concentrations of knowledge workers (above 35 percent of the workforce) create, on average, returns per employee three times higher than those of companies with fewer knowledge workers (20 percent or less of the workforce). Yet companies with more knowledge workers also show more variable returns: differences between competitors in the same industry with fewer knowledge workers.

Turning this gap into a key source of competitive advantage requires much more than reverting to the well-worn “attract, deploy, develop, and retain” talent wheel found in HR manuals everywhere. Yes, the road to success still starts with capturing more of the right talent. But to increase productivity dramatically, companies will then need to think aggressively about how to increase the pace of talent development, to deploy the best talent against the highest-value opportunities, and to improve the way such workers engage with their peers. Our analysis suggests that at many large multinationals, nearly half of all interactions between knowledge workers do not create the intended value—because people have to hunt for information, do not know where to find what they need, or get caught in the maws of inefficient bureaucracies.

Companies will need to reinvent work—what, where, when, how, who, and why

Companies such as Best Buy have increasingly recognized that work is not a place where you go but rather something you do. To get the most out of its corporate workforce, the company has adopted a “results-only work environment,” which gives workers big targets but lets them meet these goals any way they see fit. This approach has improved worker productivity by as much as 35 percent in departments that have deployed it.

Transforming process flows will also unlock new kinds of productivity. Companies such as Cisco and IBM are aggressively developing approaches—from social networks to videoconferencing—that tear down silos and reinvent how far-flung employees collaborate and exchange knowledge. What’s more, these approaches work: UK grocer Tesco, for example, saved up to 45 percent of the travel budgets of key departments by substituting videoconferencing for long-haul travel. The Hong Kong apparel supplier Li & Fung now uses videoconferencing to connect clothing designers with fabric and notions suppliers around the world, dramatically speeding the design process. That’s no mean feat for a company known for its ability to turn around “fast fashion” in weeks, not months.

Although the demand for knowledge workers is sure to grow, the supply will not. Governments aren’t moving fast enough to educate workers with the skills needed to meet the productivity imperative, and businesses can’t afford to wait. That means companies must get much more innovative at sourcing talent, whether by tapping global labor markets, building part-time workforces, or making better use of older workers. Firms also will need to rethink work progressions in a world with much flatter age pyramids—young workers no longer outnumber old ones, which has been the premise for role advancement in most companies for decades. BMW has experimented with auto production lines geared for older workers. Retailers such as CVS and Home Depot are pioneering “snowbird” programs, which let retirees go to warm climates in the winter and to work in stores there, returning to their original stores in the summer.

Information streams are the infinite by-product of a knowledge economy—the best companies will turn this free good into gold

A final productivity driver will be something businesses are creating in digital bucket loads: information. Although the volume of data created is expected to increase fivefold over the next five years, best-guess estimates suggest that less than 10 percent of the information created is meaningfully organized or deployed. That number will only shrink as the rate of information production goes up.

Enter business analytics software, which increasingly allows companies to make sense of data “noise”—helping them “de-average” data to eliminate waste, more closely target customers, and identify new opportunities. In general, companies that are aggressive adopters of business analytics are proving twice as good at predicting outcomes and three times as good at predicting risk as those that aren’t.

The Swiss telecom operator Cablecom, for example, reduced customer churn nearly tenfold through the better use of customer information. Both Amazon and Google have developed predictive models that use enormous amounts of data to figure out what products customers might like, based on past searches and clicks. IBM, Microsoft, Oracle, and SAP have spent a combined $15 billion in the past several years snapping up companies that develop software for advanced data analytics. Expect a host of new offerings that help turn information into gold.

Soon, Web 3.0 technologies—which create “smart” data, or data that can be combined intelligently with other data, mostly without direct human involvement—should extend the power of information even further. We fully expect Web 3.0 to begin disrupting information networks within the decade.

In short, companies that deploy technology more successfully to get more from the higher-quality knowledge employees they attract will gain large business model advantages—and drive substantial growth and productivity gains.

The impact of global forces on business

Related Articles

Global forces: An introduction

The great rebalancing