Unconventional development in the United States has been characterized by three trends: rapidly rising production, continual investment, and persistent negative free cash flow for the independents that have driven the shale revolution. Their explosive growth has exceeded all industry forecasts, but it has come at a cost—that of a patient marketplace prepared to accept poor short-term economic performance in the expectation that returns will flow as these independents mature. However, as investor priorities shift, independents will need to address the weaknesses and bad habits that have taken root during an era of growth and take steps to improve their capital productivity and attain profitability. Our experience with operators indicates that this will require a transformation focused on achieving operational excellence, cost leadership, disciplined growth, and balance sheet fitness.

Investor priorities are shifting

Despite rising production over the past decade, free cash flow per barrel of oil equivalent produced has been negative. Exhibit 1 plots production alongside free cash flow for a sample of 36 leading independents that we studied across unconventional basins.

This performance is the direct result of a market that values production growth at any cost and has signaled that priority strongly to independents. As Exhibit 2 illustrates, the share prices of publicly traded independents have responded sharply to changes in oil production but show virtually no correlation to free cash flow or earnings—a pattern consistent with the market behavior of start-ups or sectors in a pure growth phase. Responding to this incentive has left most independents with negative free cash flow, weak balance sheets, or both.

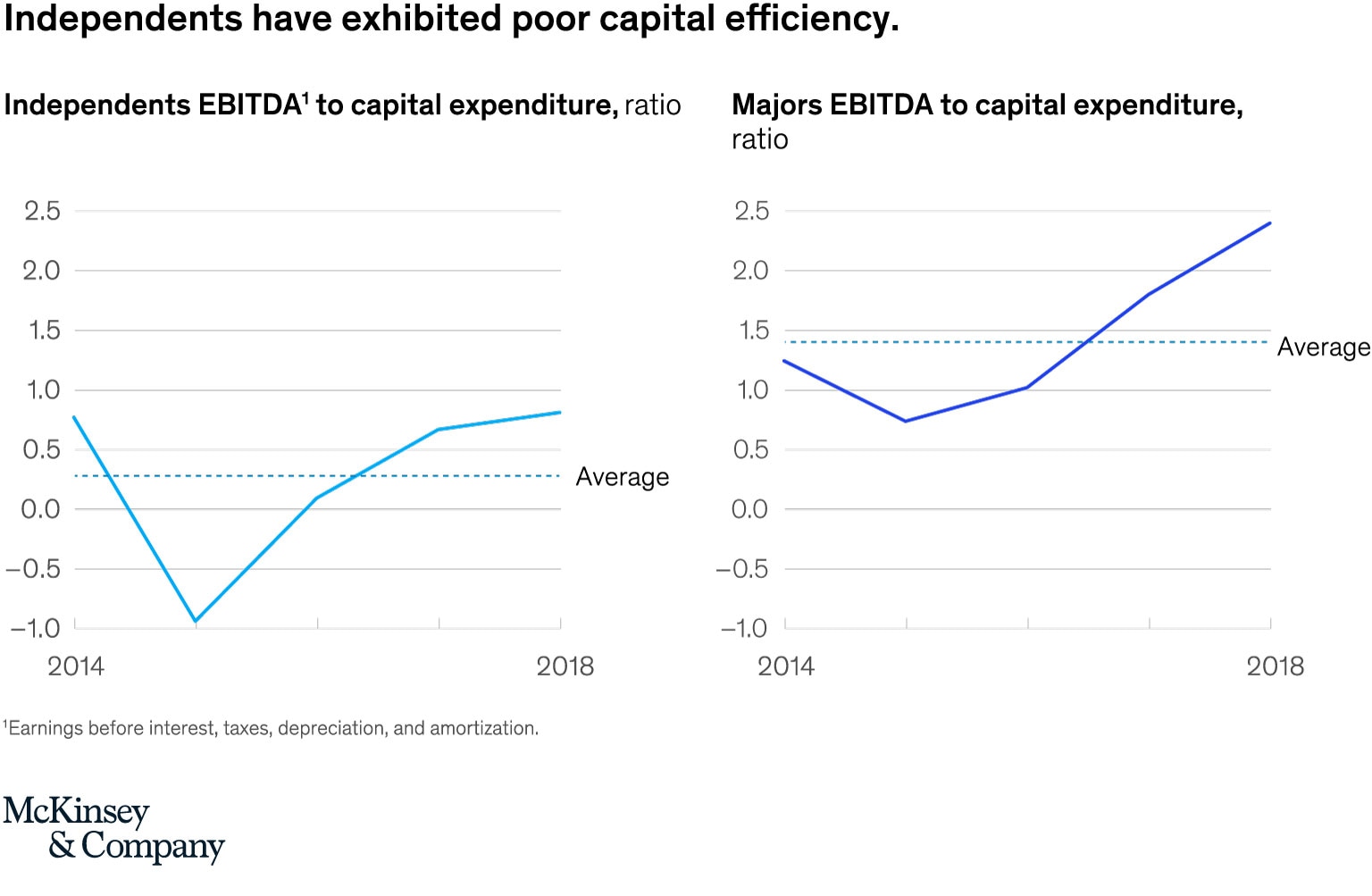

These independents have mastered how to meet investor expectations by investing large amounts of capital to deliver rapid growth. However, this has resulted in low capital efficiency, preventing independents from delivering value to shareholders across price cycles (Exhibit 3). This was evident during the first three quarters of 2018, when free cash flow was negative despite an average WTI1 price of $65 per barrel. This suggests that the US unconventional sector can sustain itself only with a price of at least $70 per barrel.

Would you like to learn more about our Oil & Gas Practice?

How should independents respond?

To win in the era of cash, independents across the unconventionals sector will need to overhaul their strategies and operations across the board. During our work with shale producers, we have identified weaknesses that are a consequence of the growth-at-all-costs incentives of the past ten years, coupled with a bias toward leanness that helped businesses survive downturns. Independents need to tackle these shortcomings directly while shifting their operating model to achieve capital efficiency across the value chain (Exhibit 4).

Our experience has shown that the most effective way to address these weaknesses is through an end-to-end transformation2 that emphasizes four key success factors: operational excellence, cost leadership, disciplined growth, and balance sheet fitness.

- Operational excellence. Independents must maintain a relentless focus on operational performance that seeks to maximize economic value rather than production volume. One way to do this is to pursue value-focused development: designing wells and development plans to optimize economic value rather than initial well rates or total production. Another way to maximize value is by sustaining base production; the most productive use of capital often lies in maintaining existing wells, so operators must take care not to neglect their base as they develop new acreage.

- Cost leadership. Successful operators must maintain the lowest-possible cost position in terms of dollars per barrel of oil equivalent, especially for deployment of capital. One key aspect of cost leadership is a relentless search for incremental improvements in drilling and completion cost, where any marginal reductions will create value. This value is derived directly from lower costs and indirectly through accelerated production if rig days are reduced or lower-tier acreage or targets are unlocked. The second key aspect of cost leadership is capturing value from procurement, logistics, and supply chain functions. An operator striving to stay lean during rapid growth may, for instance, have charged engineers with managing supply chains on top of their technical duties. But this approach can lead to higher third-party spending than a dedicated procurement team would incur. Operators can create considerable value by prioritizing and scaling up corporate functions.

- Disciplined growth. High rates of decline for unconventional wells mean that constant growth is needed simply to maintain a stable production profile. Whether that growth is achieved organically or inorganically will be a matter for each operator to determine, taking into account its strengths and risk profile. Organic growth can be achieved by unlocking low-tier acreage or expanding into emerging basins that the sector has not yet mastered. Inorganic growth via acquisition calls for strategic focus, due diligence based on deep basin knowledge with a strong ground game, and patience.

- Balance sheet fitness. To succeed across cycles, operators need a balance sheet that enables them to weather storms. If their growth comes at the expense of balance sheet health, they will struggle to survive downturns. On the other hand, those with capital will see opportunities for expansion. This requires careful attention to how deals are structured and continual analysis of asset portfolios to ensure the best use of capital.

Giants can dance: Agile organizations in asset-heavy industries

These four success factors are supported in turn by four enablers: organization, corporate functions, governance, and digital technology (Exhibit 5):

- Organization. Designing organizations to support agility can help companies stay nimble as they grow.

- Corporate functions. When central functions such as marketing and supply chain are properly empowered, overhead per barrel produced can be reduced.

- Governance. Appropriately structured planning and oversight processes allow corporate strategy to power decision making at the asset level.

- Digital technology. If properly scaled, digital technologies can drive profitability; the best systems combine established domains such as production monitoring and real-time operations with leading-edge artificial intelligence techniques.

Three archetypes for success in shale production

By analyzing these success factors in our ongoing research, we have identified three broad archetypes of companies whose primary mode of value creation positions them to thrive across cycles. However, it is important to note that none of the shale-focused independents we analyzed have averaged positive free cash flow per barrel produced since 2013. This indicates that these archetypes represent aspirations to work toward rather than features of today’s industry landscape.

Archetype one: The technology innovator

This archetype will command operational excellence and technology leadership in every phase of the asset life cycle and act as a first mover into promising new basins and new technologies alike. It is characterized by:

- smart, fast acquisitions powered by a deep understanding of the subsurface within each basin, coupled with a strong land game

- continual improvement in completions and development through controlled experimentation and a focus on economic value

- digital transformation of functions at every level

Success for this archetype will rely on a leading technology position that empowers organic or inorganic growth, an organization geared to agility, and digitized operations across the value chain.

Archetype two: The manufacturer

This archetype will command cost leadership, as measured by life-cycle unit cost in dollars per barrel of oil equivalent. Its characteristics include:

- mastery of large-scale well manufacturing: well design, drilling and completion execution, and development planning

- prioritization of base production maintenance

- high-powered corporate functions, including supply chain and logistics, that drive value and minimize overhead

Success for this archetype will rest on low-cost execution supported by strong corporate functions and disciplined oversight. An operator that embodies this archetype is likely to be a fast follower of economically proven technologies but may prefer to master traditional modes of execution rather than invest in digital transformation.

Archetype three: The integrator

The third and final archetype will build on a low cost of capital and economies of scale to master large-scale development. This is the only archetype that requires operational critical mass. Its characteristics include:

- balance sheet strength and a very high credit rating to keep cost of capital low

- a long time horizon and a broad sphere of influence enabling coordination at scale

- the adoption of best practices across the whole company

Success for this archetype begins with balance sheet fitness and requires strength in each enabler: organization, corporate functions, governance, and digital. The organization must be carefully designed for lean operations, and the business will rely on digital technology to drive cost improvements.

The greatest potential for large-scale value creation in unconventionals is likely to lie with the integrator archetype, but as of 2019, no company is ready to assume this mantle. The independents that led the shale revolution have yet to prove they can generate value at scale or strengthen their balance sheets. On the other hand, the integrated majors that tried to use their capital and reach to achieve this archetype have been unable to match the operational and cost performance of the independents. However, recent consolidations involving majors and large independents may provide a basis for realizing the integrator archetype if operations can be transformed to unlock value.

Adapting to the new era of cash requires a disciplined and relentless focus on capital efficiency and cash generation, whether among independents seeking to retool or majors wanting to extract value from their acquisitions. For most companies, this requires end-to-end transformation of strategies, mind-sets, capabilities, and ways of working. Our work with independents has shown that this is achievable with the right leadership support, organizational buy-in, and tools to make it happen.

Future articles will consider how operators can deliver excellence and capital efficiency at each step in asset development.