Mae West was wrong – too much of a good thing isn’t wonderful

I wouldn’t recommend looking to movie star Mae West for oil and gas production guidance, drilling tips or price outlooks. She certainly did have a way with words, though one of her more famous quotes—“Too much of a good thing can be wonderful!”—is dead wrong for producers in the Permian Basin and Western Canada.

Producers in the Permian and Western Canada are forced to take hefty price discounts because production has overwhelmed takeaway capacity. We believe this will continue to be the case through the end of the year, at least for the Permian. In fact, it’s entirely possible that some additional Permian production growth may have to be curtailed in the next few months, as there is no spare takeaway capacity to get these volumes to market. This price blowout is evident in the stock prices of some Permian-focused producers. Despite West Texas Intermediate (WTI) crude oil prices stabilizing at around $70 per barrel, up about $20 per barrel over its August 2017 prices, stock values for some Permian-centered producers have struggled to keep up, weakened by news about the infrastructure bottlenecks.

The first half of 2018 saw crude production continuing to rise in North America, particularly in the Permian and Western Canada. US crude exports are also on the rise, which would indicate a positive outlook for North America’s crude market overall. However, ample production growth and constrained takeaway capacity have combined to create a tight market with big discounts.

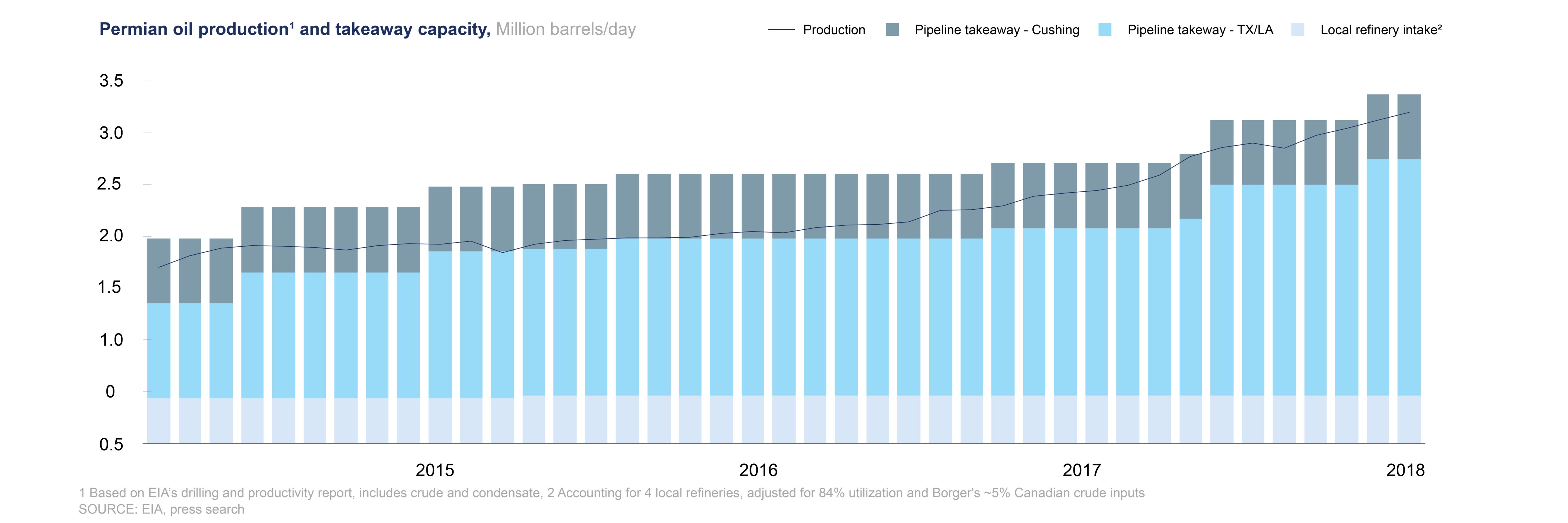

The Permian has seen production grow over 60% since January 2017, to an estimated 3.4 million barrels per day (bpd) in August 2018, placing significant pressure on infrastructure and complicating logistics for operators as they attempt to transfer crude out of the Midland area to an end market (Exhibit 1). With takeaway capacity constrained, Midland price assessments collapsed as producers struggled to get crude to a demand market, falling over USD10 a barrel from March to May 2018 (Exhibit 2).

Falling prices for Western Canadian Select (WCS) crude in late 2017 brought the WCS-to-Gulf Coast WTI discount to an all-time high of USD29.50 a barrel in January 2018. Compared to the Permian, Canadian prices fell faster and more dramatically, largely because pipes from Canada never had significant excess capacity, so even small increases in production growth led takeaway capacity to be severely constrained in late 2017. Congestion in the Cushing, Oklahoma area, largely due to increased Permian volumes, has also contributed to the continued high differential between Canadian and Gulf Coast crude prices as significant volumes of Canadian crude are routed down through the Midwest and Cushing.

This cyclical pattern should feel familiar to the industry. It’s the newest iteration of the industry’s ongoing boom-and-bust cycle, though this time it is not macroeconomic crude oil supply and demand that are out of balance but more localized imbalances between supply of crude oil and demand for outbound transportation capacity.

These same temporary imbalances have hit other basins, notably the Marcellus and the Bakken. Deep discounts were forced on gas producers in the Marcellus when supply of their product exceeded outbound pipeline capacity. In the Bakken, however, the availability of railroad transportation capacity served to alleviate, though at a price, the imbalance a few years ago between crude oil production and pipeline capacity.

Increased demand for pipe capacity causes the market to be tight and differentials to coastal crudes to widen, driving up pipe utilization. With increasing utilization, additional investments are made to expand current capacity, which often leads to overcapacity and differentials narrowing as pipe tariffs fall. Last week, Enterprise Products announced it would expand the Cushing-to-Gulf Coast pipeline by 100,000 bpd in September by using drag reducing agents to help alleviate bottlenecks from both the Permian and Canada. In other words, the Permian discounts likely are a short-term phenomenon.

Another infrastructure bottleneck is somewhat constraining US crude oil exports. While the US supply of crude for export continues to grow and have the potential to replace other light- and medium-grade crudes for some international buyers, the lack of significant very large crude carrier (VLCC) loading capabilities currently in the Gulf Coast makes it more challenging for big buyers, particularly in Asia, to consistently load US crude.

This export bottleneck should start to ease in 2020 when the Corpus Christi port terminal expansion is completed. While the crude export dilemma is causing US crude prices to fall slightly, they are still strongly linked to the international market. The real impact on prices comes from supply levels and logistical constraints in inland regions such as the Permian and Western Canada. And there, we see at least another 6 months of discounts and growing pains.

For a more detail on this topic, please see this article.

Tim Fitzgibbon is a senior industry expert based in Houston. We would like to thank Emily Billing for her contribution.