Only 30 percent of executives representing the health care industry in the United States say their companies are ready for reform and changing economic conditions, according to a McKinsey survey on how prepared industry players—payers, providers, and pharmaceutical companies—are for change.1 However, 76 percent say the impact of reform on the industry will be significant, and 54 percent say the same about the effects of the current economic crisis.

The survey asked executives where their innovation efforts are focused, which areas are likely to provide the greatest benefit to their companies in the near term, how the importance of innovation has changed within respondents’ companies since the financial crisis erupted, and how ready they are to adapt to ongoing reform and the new economic environment.

The minority of companies whose executives say they are ready to adapt have a different strategic focus than the others. Their top priority is to increase the value of health care by, for example, reducing the misuse, underuse, and overuse of care or increasing the quality of care received. In contrast, at most companies, the top priority is increasing revenue or membership growth. Also, companies prepared for change innovate differently: they can count on leadership’s support, for example, and drive innovation in a wider range of areas, including product design, customer service, and IT.

Is the industry ready?

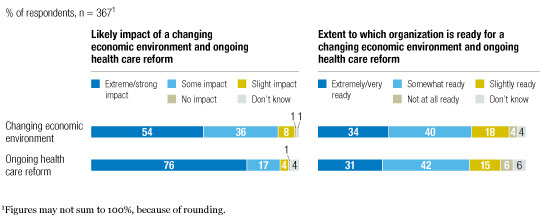

Despite ongoing attention in the United States to health care reform and the current economic crisis, less than a third of health care executives say their organizations are “extremely” or “very ready” for reform; slightly more are prepared for changes in the economy (Exhibit 1). Among insurers, the percentage who report they are prepared for reform drops to 14 percent, and more than 20 percent say they simply don’t know. (In contrast, only 2 percent of executives at providers and 6 percent of executives at pharmaceutical companies are unsure about their organizations’ preparedness.)

Unprepared for change

What differentiates the prepared?

Executives who say their companies are ready for reform are focused on increasing the value of health care. This strategy makes sense in the face of rising costs of care. Among respondents overall, however, 42 percent say the top priority is instead increasing revenue or membership growth.

Leadership and innovation

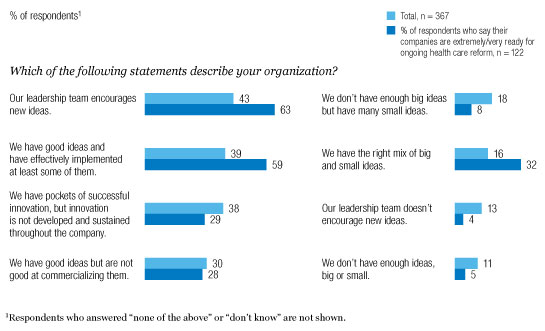

Companies that are prepared for change are also more likely to have leadership teams that support innovation. Moreover, in the face of economic crisis and the US election, innovation has taken on an even more prominent role at these companies: 75 percent of executives who say their companies are prepared for change—versus 58 percent of respondents overall—say the importance of innovation has increased since September 2008. Moreover, 63 percent of executives at well-prepared organizations say their leadership teams encourage new ideas, compared with 43 percent overall (Exhibit 2). One-third say their senior leadership does extremely well at developing an innovation strategy, versus only 11 percent overall, and almost 80 percent consider their organizations more innovative than their competitors, compared with about 50 percent of respondents overall.

Companies prepared for change

A diversified innovation portfolio

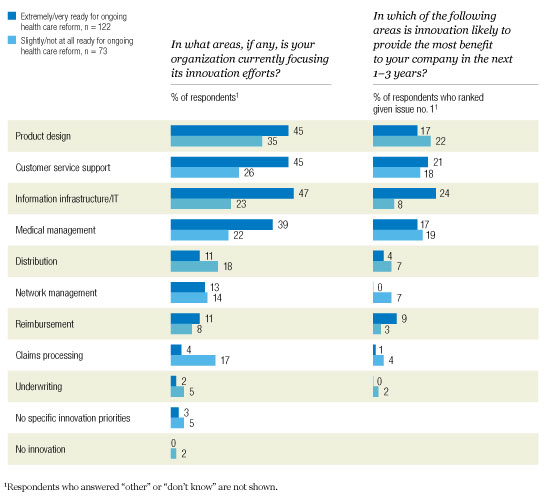

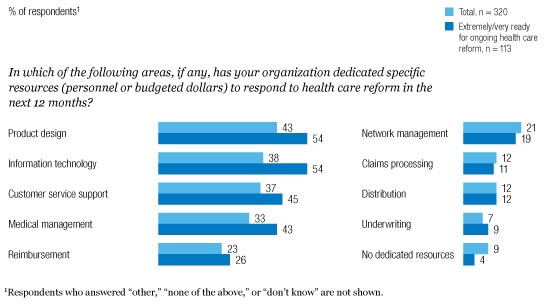

Companies prepared for change also pursue innovation in a wider range of areas than others do (Exhibit 3). As these companies aim to increase the value of health care, they are focusing their innovation efforts on product design and customer service equally. The well-prepared companies are also targeting innovation in the areas where they expect to gain the most benefit in the next one to three years—much more so than less prepared organizations are. Furthermore, companies that are ready for change have assigned dedicated personnel to these areas or have budgeted funds to use over the next 12 months in response to reform (Exhibit 4).

Innovation strategy

Responding to reform

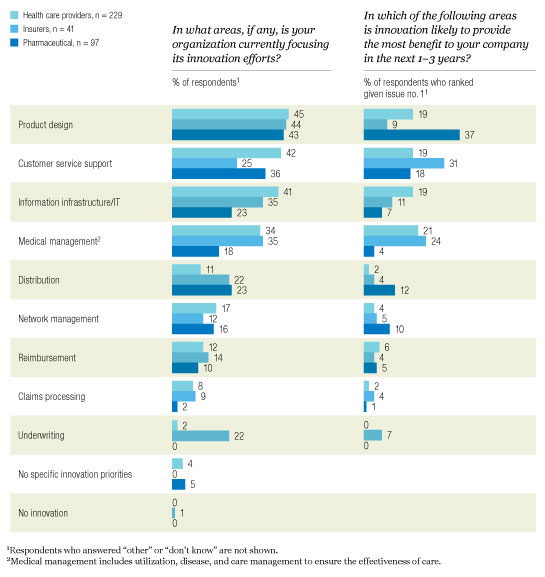

Prepared or not, health care providers are more focused compared to other players. Providers say product design, customer service, IT, and medical management2 are likeliest to yield the majority of benefits in the near term and they are focusing most of their innovation efforts on those four areas (Exhibit 5). By contrast, insurers invest significant effort in product design, yet this is the area they say is least likely to yield returns in the near term.

Where the innovation is

Adjusting to the changing world

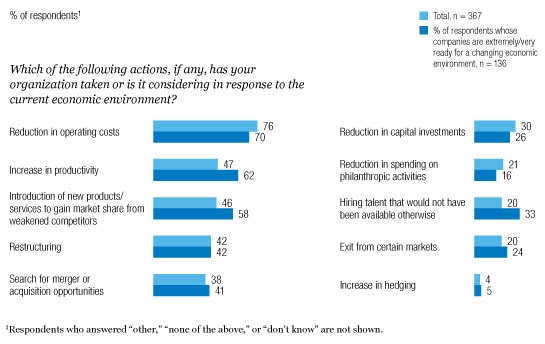

To prepare for health care reform and a changing economic environment, 65 percent of respondents at companies prepared for change say they have made one or both of these subjects a formal part of leadership meetings and discussions. Forty-five percent of executives also mention gathering competitive intelligence as a way to prepare. While 70 percent of respondents at these companies say they are reducing operating costs in response to the crisis, around 60 percent are also focusing on more strategic initiatives, such as increasing productivity and introducing new products or services to take advantage of weakened competitors (Exhibit 6). By contrast, about 85 percent of the unprepared are focusing on reducing operating costs, followed by only 35 percent who are aiming to increase productivity.

Strategic initiatives to confront the crisis

Where does innovation come from?

Overall, most new ideas, health care executives say, come from competitive market analysis and employees. Surprisingly, given the increasing public attention to consumer-focused health care, only 41 percent say new ideas come from consumer insights. Further, the results indicate executives have more to learn about consumers’ preferences when purchasing health insurance and other health-related products. Around 50 percent say employers exert the most influence on consumers who are choosing insurance and that employers are the preferred purchase channel. A separate McKinsey consumer survey on retail health care,3 however, found that consumers are more likely to go to health insurance companies’ Web sites for information and prefer to purchase health insurance from a salesperson or agent in person or via phone.

One in three respondents say their organizations do not currently have in place any formal mechanisms to facilitate innovation. Thirty-one percent say their organizations have formal partnerships with research centers or academics, followed by 27 percent whose companies have dedicated funds to innovation initiatives. Executives who rate their companies as more innovative than their competitors are more likely to have dedicated funds to innovation (35 percent versus 27 percent of respondents overall) and to have in place a council or committee that reviews innovation initiatives and their progress (32 percent versus 25 percent overall).

Looking ahead

-

While each player within the industry—insurers, providers, and pharmaceutical companies—faces a different set of challenges, many could benefit from improved innovation practices. These include setting an innovation strategy that focuses on the areas most likely to yield returns, applying more sophisticated consumer insight techniques, and generating ideas using sources beyond employees and competitors.

-

Investments in product design are critical as organizations prepare for change, but insurers and health care providers can’t afford to overlook innovations in customer service and IT, which they say will also provide the most benefit in the near term.