This essay is part of a package of articles that examines the US stimulus broadly and explores its impact on three sectors in particular: health care, energy, and broadband.

The Obama administration plans to use electronic medical records (EMR) to cut the cost and improve the quality of health care over the next decade. In the president’s words, the objective is to “make sure that every doctor’s office and hospital in this country is using cutting-edge technology and electronic medical records so that we can cut red tape, prevent medical mistakes, and help save billions of dollars each year.” As part of the American Recovery and Reinvestment Act (ARRA), the administration has committed an estimated $40 billion in funding for health care IT.

To meet these goals, the sector must undergo a wrenching shift from the current silo-ridden and usually paper-based arrangements to a system that coordinates information more effectively and efficiently, with IT supporting a wide range of medical decisions. Government funding is likely to speed the adoption of electronic medical records and change the way players across the sector operate.

Hospitals and physicians will feel the most profound effects. The ARRA sets up incentives and penalties that will prompt health care providers to upgrade their IT systems rapidly to reach the act’s standards for “meaningful use” of EMR. IT vendors will find that this fast-moving market demands new strategies. Medical payers should be prime beneficiaries of the change, because health care costs may fall and treatments should become more effective and less error prone. In fact, the payers will probably support the even faster adoption of EMR, whose increasing use will promote better guidelines for the reimbursement of drugs and procedures.

Significant second-order effects for pharmaceutical companies and manufacturers of medical products are likely as well. Better information should not only help quicken the pace of research for both drugs and devices but also improve their quality. Nonetheless, a data- and rules-driven health care sector will challenge these companies, since better information about treatments could lead to new restrictions on products and procedures.

Left unanswered is the contentious issue of how the more aggressive use of EMR affects privacy. The substantial flow of dollars into EMR suggests that the administration feels confident that government and industry, working together, will resolve the problem.

Health care providers

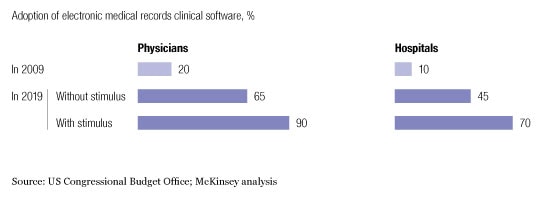

The heart of the Obama package is raising EMR adoption rates among health care providers. Most surveys show that cost is the chief barrier, though the economics of adoption are already improving. Even without the stimulus, growing numbers of physicians and hospitals will probably switch to electronic records to drive down costs and improve the management of care. The stimulus package gives a significant boost to this effort (exhibit). First, it will provide incentive payments totaling $36.5 billion for hospitals and physicians’ groups, requiring them to show that they are making meaningful use of the technology, starting in 2011. Second, it will extract escalating penalties, charged against Medicare and Medicaid payments, from providers that haven’t met this standard by 2015.

Stimulating adoption of electronic medical records

For private-practice physicians, the incentives and penalties are a powerful prod. Over five years, Medicare incentives will amount to as much as $44,000 per doctor, probably more than enough to cover the cost of installing EMR, particularly as systems using software-as-a-service (SaaS) technology1 go mainstream. The Congressional Budget Office estimates that adoption rates will climb to 90 percent by 2019.

Larger in-patient providers, principally hospitals, face a more complicated situation. The combination of stimulus payments and penalties clearly improves the return on investments in EMR and will accelerate its rate of adoption. But the costs and risks are higher, as well. For larger players, the new regime requires bigger and more complex IT systems and therefore higher long-haul costs to manage and maintain them. The stimulus grants won’t cover much of this sprawling investment, so to get the complete benefit the big health care providers must ensure that their physicians make full use of EMR. They’ll also need to retool their workflows to take advantage of the switch from a paper-based to an automated system. Some providers will look at the full complement of necessary investments, calculate the returns over five to ten years, and decide that EMR isn’t worthwhile—payments and penalties notwithstanding.

IT vendors and medical-equipment manufacturers

IT vendors can expect large opportunities. Over the next decade, we estimate, hospitals and physicians will lay out approximately $170 billion on EMR. Hospitals will be responsible for the lion’s share, 75 percent—more than ten times what they get in incentive payments. The spending will fall in three areas: hardware (roughly 40 percent), software (around 30 percent), and services (another 30 percent). The pace of adoption will pick up gradually over the first two years and then gain steam as hospitals face the prospect of punishing penalties in five years. Innovation will gain steam as well. Companies from outside the sector will probably move in on the opportunities. Start-ups will offer novel ways to bring down costs while still giving doctors and hospital administrators opportunities for customization and local control.

Medical-equipment makers have a big role to play, as well. Some, for example, already sell products to provide better but lower-cost access to care via telemedicine and remote monitoring. Better information through EMR will give these companies greater importance. What’s more, the ARRA sets aside money to develop the bandwidth infrastructure needed to bring telemedicine to underserved patients. One lingering obstacle: insurers sometimes don’t cover these solutions, so the companies that make them will need to work with payers to create new options for coverage.

To tap these opportunities, IT vendors as a group must rethink their strategies by identifying the software and services that the new IT-enabled world requires and upgrading their product portfolios to meet the meaningful-use standard. Partnerships among hardware, systems, and clinical-software vendors will improve their return on investment and play a critical role in clarifying the new environment and the demands of the health care providers.

Health insurers and drug makers

As the rate of adoption increases, payers stand to gain the most from greater reliance on IT. Better information promises to cut costs and improve medical care’s overall quality and efficiency. But to succeed, payers will need closer, more trusting relationships with hospitals and doctors to support the new wave of IT-enabled clinical decision making.

Here’s how the system should work. Under the ARRA, health care providers must implement clinical-decision-support (CDS) systems by 2015 to avoid penalties. These systems would ferry, organize, and analyze information from medical records and help clinicians choose the best course of treatment by weighing statistical evidence on the efficacy of various types of care and balancing that evidence against their costs and insurance coverage limits.

Payers should gain greater influence over physicians by ensuring that the CDS systems they use have accurate medical information (and patient-specific cost information), which will help physicians improve their clinical performance. These companies must scrupulously ensure that this information is unbiased, however, because physicians will discount recommendations that strike them as unduly influenced by cost-reduction imperatives. As records systems spread through the medical community, they will create large pools of longitudinal patient data. Payers will tap this information to deepen their knowledge of effective treatments. Ultimately, the information will help payers make better decisions on the reimbursement of diagnostics, pharmaceuticals, and medical devices.

Pharmaceutical manufacturers too will feel second-order effects. CDS systems will make it easier to impose and enforce stricter controls on the types of prescription medications that drug plans cover. Pharma products must therefore offer more strongly differentiated clinical and economic benefits than ever before; otherwise, health care providers will generally prefer cheaper generic offerings. Pharma manufacturers may thus see shifts in the market share of various branded products and shifts from them to generics. Yet new pools of data on patients will allow these companies to step up their R&D productivity and expand their markets. The data, for example, should make it possible to design better and faster clinical trials and to develop stronger evidence for the medical and economic benefits of products, both existing and new.

Although seemingly a small portion of spending on health care, the ARRA’s medical IT provisions could represent a turning point in the whole sector’s evolution. Some players will benefit and others suffer, but all will be affected and may need to adjust their strategies.

Related Articles