“Bad banks” are back. The concept is simple. The bank divides its assets into two categories. Into the bad pile go the illiquid and risky securities that are the bane of the banking system, along with other troubled assets such as nonperforming loans. For good measure, the bank can toss in non-strategic assets from businesses it wants to exit, or assets it simply no longer wants to own as it seeks to lessen risk and deleverage the balance sheet. What are left are the good assets that represent the ongoing business of the core bank.

By segregating the two, the bank keeps the bad assets from contaminating the good. So long as the two are mixed, investors and counterparties are uncertain about the bank’s financial health and performance, impairing its ability to borrow, lend, trade, and raise capital. The bad-bank concept has been used with great success in the past and has today become a valuable solution for banks seeking shelter from the financial crisis.

But while the idea is simple, the practice is quite complicated. There are many organizational, structural, and financial trade-offs to consider. The effect of these choices on the bank’s liquidity, balance sheet, and profits can be difficult to predict, especially in the current crisis. Capital and funding markets are still fragile in many regions, and many asset classes have been severely affected.

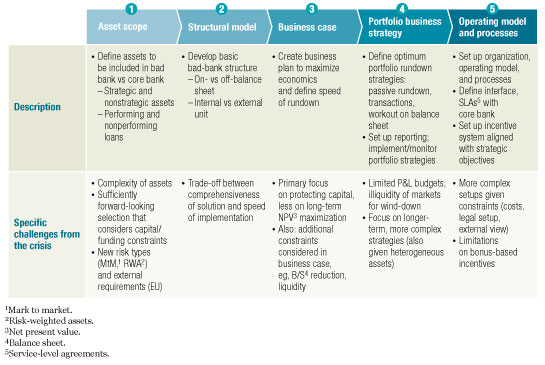

Consequently, institutions have developed several variations on the bad-bank theme to handle their particular sets of troubled assets and their available financial resources. These banks have made their choices, for better or worse, and are now working through a range of operational problems. Others, however, are still stuck at square one and are understandably perplexed by the range of possibilities and how the choice of a bad-bank model might affect their future. An analysis of bad banks set up in the crisis suggests that there are five sets of choices banks must make—choices about the assets to be transferred, the structure, the business case, the portfolio strategy, and the operating model. Each of these choices must be made while considering the impact on funding, capital relief, cost, feasibility, profits, and timing—a daunting array.

Success depends on getting these choices right, and on a number of other factors. Chief among these is government support, to help banks understand and manage the many regulatory, accounting, and tax issues, and in some cases to provide financial backing. Again, each country’s case is different, depending on the health of its banks, but broadly speaking, governments must smooth the way for the creation of bad banks and clearly establish the extent to which the state will assume the risk of the bad assets. In some countries, governments are considering a national bad bank to house the unwanted assets of all domestic banks. Many governments have not gone that far, but most are concluding that their support is justified to ensure the future stability of the financial system.

The bad-bank concept has attracted so much support lately that it is now widely viewed as the most likely savior in the rescue of the banking system. While that may be expecting too much, it is fair to say that an understanding of the bad bank is essential for the modern banker.

From good to bad

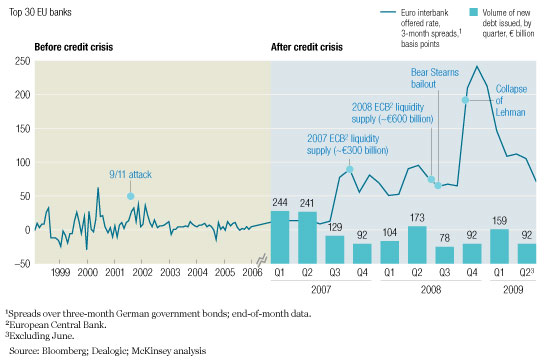

Two years on, the crisis continues to afflict most banks, particularly those with significant levels of illiquid and difficult-to-sell securities—the so-called toxic assets, and especially collateralized mortgage obligations (CMOs), collateralized debt obligations (CDOs), and collateralized loan obligations (CLOs). With these assets still on the balance sheet, banks are finding it difficult to raise funds from wholesale markets or capital from equity investors. Short-term funding spreads are slowly returning to precrisis levels, but they are still well above the levels seen in the early part of this decade—this despite the still-significant support (including quantitative easing, repurchase programs, loan guarantees, liberalized collateral requirements, and so on) from the central banks (Exhibit 1).

Wholesale funding

Finding funds will soon get more difficult. Regulators are preparing new capital requirements and other changes that will impose fearsome new burdens on banks. Regulators including the Financial Services Authority (FSA) are considering raising capital requirements for some institutions and asset classes by a factor of three to five.

In response, banks are pursuing several channels. Most obviously, they are getting out of capital-intensive and structured businesses—in a word, deleveraging. They are pulling back from international operations to concentrate on domestic business. And they are dramatically overhauling their risk functions. All these steps are necessary and proper—but they may be insufficient. Capital is still scarce. Banks are still overleveraged, and unsalable assets still carry too much risk. Confidence is still wanting; so long as the illiquid assets sit on banks’ shelves, investors will be wary.

Hence the return of the bad bank. Dividing in two can help stricken institutions ring-fence their core businesses and keep them separate from the contamination of toxic assets. The separation allows the bank to lower its risk and to deleverage as first steps toward creating a sound business model for the future. A more efficient and focused management with clear incentives for portfolio reduction can maximize the value of bad assets. And the clear separation of good from bad can help banks regain the trust of investors, by providing more transparency into the core business and lowering investors’ “monitoring costs.” All these benefits do not, however, come for free: there are still economic losses and risks on the balance sheet that must be shared between the good-bank and bad-bank investors.

Divide and conquer

As noted, the bad-bank idea is not new. It was pioneered at Mellon Bank in 1988 in response to deep problems in the bank’s commercial real-estate portfolio. It was applied in past banking crises in Sweden, France, and Germany. And in the current crisis, banks have been busily reinvigorating the idea. As suggested above, every self-dividing bank seeks to do three things: clean up the balance sheet and so restore confidence, protect the profit and loss (P&L), and assign clear responsibility for the management of both good and bad banks.

In the early examples, the emphasis was on improving the bank’s profits through a better incentive system and a more focused and efficient wind-down of assets. In the current crisis, much of the focus is on rebuilding trust with investors and rating agencies by clearly separating the assets and providing transparency into the bank’s operating performance. With trust restored and capital to back investors’ faith, banks are convinced that their economics will improve.

In sorting through the various structures banks are using today, we have identified five sets of choices that go a long way toward determining the bad bank’s structure and operations and eventual success (Exhibit 2). We explore each of these five variables here.

Five key design elements

Asset scope

Banks need to address two broad categories of assets. At the center of the discussion, as noted, are assets with a high risk of default, substantial mark-to-market risk, or substantial risks from “ratings drift” under Basel II. For most banks, that means structured credit and related asset classes that have come under strain in the crisis. The mark-to-market and Basel II risks that dominate toxic securities portfolios seem to have reached a peak. But as the global recession continues, the risk from credit defaults is still present and may even be on the rise. In the United States, the United Kingdom, southern Europe and Eastern Europe, commercial real-estate loans are poised to default; some consumer credits are also wobbly in these regions. Some structured credits are faring poorly in the United States and Western Europe. The second category, which we call nonstrategic assets, includes anything the bank wants to dispose of, either to deleverage or otherwise resize its business model. This might include the assets of entire business lines or regional operations.

The key to determining the right assets to go into the bad bank is a forward-looking view on the bank’s risk and its future business model. A bank can only segregate bad assets once without losing its credibility.

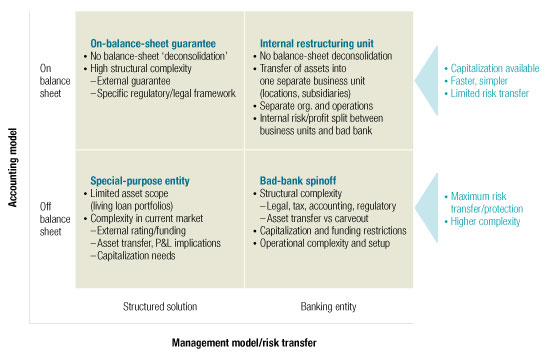

Organizational model

There are four basic models for the bad bank; variants and hybrids are possible (Exhibit 3). The model is determined primarily by the choice of whether or not to keep the assets on the balance sheet. Moving them off the balance sheet provides greater comfort to investors and counterparties and better transparency into the core bank’s economics, but it is more complex and expensive. A secondary choice is whether to house and manage the bad-bank assets in a banking entity or to accomplish the transfer of risk in a less concrete way—what we call a “structured solution.” The four basic models are as follows:

-

On-balance-sheet guarantee. In this structured solution, the bank protects part of its portfolio against losses, typically with a second-loss guarantee from the government. The model can be implemented quickly and minimizes the need for upfront capital, but it results in only limited risk transfer. The continued presence of the bad assets on the balance sheet and the lack of clear legal separation make this the least attractive model to new investors; for them, the bank’s core performance is still not transparent. The approach might best be used as a first step to stabilize the bank, buying enough time to develop a more comprehensive solution. That was the case at Citibank, where government guarantees were provided as a first step to ring-fence the economic risks on the balance sheet.

-

Internal restructuring unit. Establishing an internal bad bank or restructuring unit becomes attractive when the toxic and nonstrategic assets account for a sizable share—20 percent or more—of the balance sheet. In this scheme, the bank places the restructuring or workout of the assets in a separate unit, which ensures management focus, efficiency, and clear incentives. As an example, Dresdner Bank established an internal restructuring unit in 2003 and dedicated about 400 FTEs1 to the asset restructuring and workout of a €35 billion portfolio. The unit shut down ahead of schedule in 2005. While this on-balance-sheet solution still lacks efficient risk transfer, it provides a clear signal to the market and increases transparency into the bank’s performance—particularly if the results are reported separately. Any bank that wants to create a fully separated bad bank (described below) is likely to first create an internal restructuring unit.

-

Special-purpose entity. In this off-balance-sheet structured solution, the bank offloads its unwanted assets into a special-purpose entity (SPE), usually government-sponsored, which is then taken off its balance sheet. An example of a bank that has followed this approach is UBS, which transferred £24 billion of illiquid securities to an off-balance-sheet SPE funded by the Swiss National Bank. This solution works best for a small, homogeneous set of assets, as structuring credit assets into an SPE is a very complex move and for many banks is not practical. The heterogeneity of the assets involved, inves-tors’ mistrust of securitization structures, and new regulatory penalties make most securitizations too expensive for banks.

-

Bad-bank spinoff. This is the most familiar model and also the most thorough and effective. In the spinoff, the bank shifts the assets off the balance sheet and into a legally separate banking entity. Such an external bad bank ensures maximum risk transfer, increases the bank’s strategic flexibility (for example, for potential M&A), and is a prerequisite for attracting outside investors. However, the complexity and cost of the bad-bank spinoff and its operation are very high because of the need for com-pletely separate organizational structures and IT systems and a doubling of the effort needed to comply with legal and regulatory requirements. There are further complexities surrounding asset valuation and transfer; funding for the bad bank may not be readily available, and there is no ready-made legal or accounting framework for asset transfer to bad-bank entities. For all these reasons, the bad-bank spinoff is a last resort, a step to be taken only after other measures prove insufficient in efficiently managing all toxic and nonstrategic assets. The challenges involved in a bad-bank spinoff will typically require that governments play a key role, especially in creating a common legal and regulatory framework and in supporting bad banks through funding or loss guarantees.

Four types of bad banks

Business case

Each of the four structural solutions must be evaluated against a clear set of predefined criteria in order to create a comprehensive business case that calculates their effects, today and in the future, on balance-sheet reduction, liquidity, and capital protection—the goals of the exercise. The criteria should include those relating to solvency and the balance-sheet (capital and RWA relief under Basel II, mark-to-market volatility, expected losses), cost (transfer costs, funding costs, guarantee and capital costs, operating costs), and legal, regulatory, and accounting issues.

The result will be a business plan that will maximize the bank’s economics and suggest the speed at which the portfolio is wound down. The mechanics of that winding-down are deter-mined in the next step.

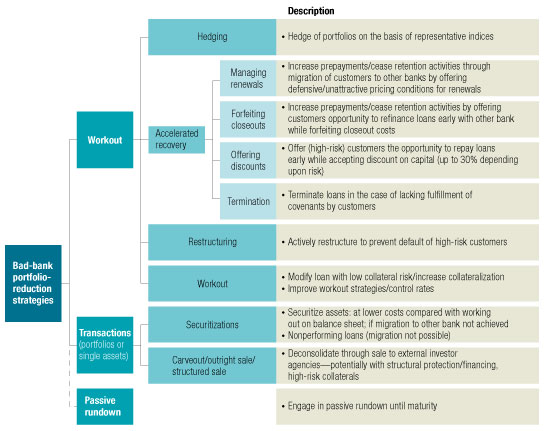

Portfolio strategy

Identifying and pursuing the optimal strategy for the bad assets once the appropriate structure has been chosen will be crucial to maximizing their value. Given that some proposed bad-bank portfolios are very large, up to €100 billion in size, an improvement of a portfolio’s return by only a few percentage points creates enormous value for the bank.

There are three common strategies for extracting value from the assets (Exhibit 4):

-

Passive rundown. The bank monitors the assets and acts only if risk rises above a predefined threshold. In today’s environment, given the high cost for transactions on illiquid and nonstrategic assets, this represents a “base case”—that is, the option that banks should choose unless they can see a compelling argument to pursue one of the more complex strategies. This is particularly true for bad banks built around structured credit assets that cannot be sold without incurring significant costs.

-

Transactions. This option includes hedging, where feasible, and the securitization or sale of selected assets, whole portfolios, or entire businesses. It is especially effective for divesting nonstrategic businesses or low-risk portfolios for which an adequate price can still be achieved, as well as situations where the portfolios or businesses can easily be separated.

-

Workout. Besides selling or hedging the risk, the bank can also try to accelerate recovery by actively “managing down” the assets themselves. It can, for example, forfeit closeouts, offer discounts, or terminate contracts if, say, covenants have been broken. Other options include restructuring high-risk assets to prevent defaults. Where assets are already in default, banks can follow a standard workout process. However, while workout has been a key strategy in the past, its efficacy in the current environment is less sure, given the limited ability of many borrowers to prepay. Nevertheless, some tactics, such as seeking early repayment, may still be relevant to particular loans.

Three portfolio strategies

To determine the best strategies, their impact should be incorporated into the business-case analysis by way of net-present-value (NPV) calculations, P&L impact, effect on capital and funding, and risk implications. Most banks will find it necessary to balance the need for the quick disposal of assets with the potential losses that would result from selling them below book value.

Operating model and processes

Especially if the bank chooses to work out its assets in a discrete unit—either an internal group or a spun-off bad bank—choosing the right operating model, setting up a proper organization, and developing appropriate processes are essential to extracting value from a more focused management of the assets.

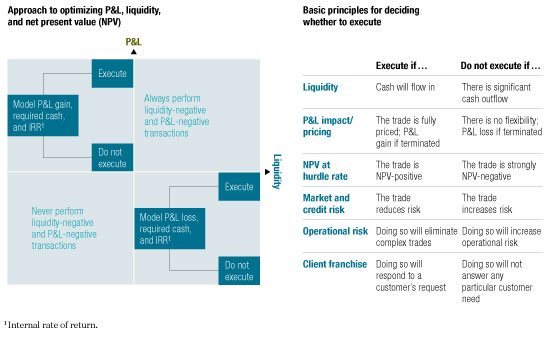

Defining the objectives is a good starting point but can be a challenge. In past efforts, the focus was largely on the P&L, NPV, and value creation. In today’s environment, liquidity, collateral, and gross risk reduction must also be considered for structured credit assets. Targets must be set, and the trade-offs must be clearly understood (Exhibit 5).

Understanding the trade-offs

With its objectives identified, the bank can then determine its operating model, taking into account the size of the portfolio, the type of assets, the geographies involved, and other factors. The workout unit (and of course a spun-off bad bank) will require its own top-level management; it can be considered a separate market unit or part of the risk or finance organization. The unit crucially needs both top-quality leader-ship and highly developed workout skills, and its people need a strong sense of entrepreneurship. In many instances, the unit should have its own functional support and operate more or less as a stand-alone bank. Other banks will find it better for the unit to be entirely market-focused, drawing upon the core bank for support. In the former case, the need for specialization extends to the support functions; these people too need a deep understanding of workout so that they can provide structuring advice from a risk, accounting, and funding perspective.

For banks that choose to do more than just passive rundown of the assets, workout skills will be essential. But most will find that processes need to be rebuilt and strengthened, as most banks’ workout teams have not had much to do over the last several years. Finally, the incentive system needs to be aligned with the bank’s strategic objectives. As was established in the pioneering bad banks, incentives should consider time versus P&L effects. This time around, and particularly for structured credit assets, the P&L needs to be neutralized for market movements (in both directions) and must also consider additional constraints. While uncapped bonuses awarded on an NPV basis (as in the past) may still be appropriate, in many instances banks will want to take the measure of stakeholder opinion and comply with any new guidelines on compensation. As the portfolios shrink over time, special attention should be given to non-monetary incentives, such as the right of workers to return to the core bank at a later date, or special training to qualify for a new position once the assets have been worked out.

The financial crisis took most by surprise, and the assets it impaired continue to languish on many banks’ balance sheets. The good news is that there are mechanisms such as the bad bank that can help managers and governments deal with the crisis and effectively stabilize the banking system, even in the face of further deterioration.

Related Articles