Commercial insurance lines, such as property and liability, for companies with revenue between €20 million and €200 million represent one of the most profitable and strategically important segments for insurers worldwide. That’s because insurers of this midmarket segment act as partners for a vital economic engine, in a market that’s large and growing with a wide range of cross-selling opportunities.

Yet the midmarket presents risks. Less-structured internal processes, lower risk-management maturity, and the limited professionalization of key roles often leave midmarket companies more vulnerable to both insurable and operational shocks. Their profitability is being squeezed, primarily by price pressure and rising exposure to natural catastrophes, which is undercutting insurer profit margins. And there are large, emerging challenges, including cyberthreats, AI-related liabilities, and supply chain disruptions.

Yet these risks also represent untapped opportunities. While they increase the complexity of risk assessment, in our experience midsize companies are often under-protected—which means insurers that can effectively underwrite and package these risks stand to differentiate themselves and grow profitably. Rather than threatening margins, these emerging risks offer a path to relevance and value-added growth for carriers that can respond with speed and precision.

To bolster profitability and build resilience, insurers with material exposure to the midmarket segment—both diversified players and specialists, which may be particularly vulnerable—will need to reform their approach to risk management. This article lays out a four-step framework to isolate and manage excessive risk exposure and implement a structured, data-driven approach to the ongoing management of midmarket insurance risks. While we draw on best practices used by large corporate insurers, the framework is tailored specifically to the midmarket segment, where the opportunity is clear: Acting quickly can mitigate volatility; restore technical profitability, especially among property and liability insurers; and unlock long-term growth.

Unprecedented change and emerging risks

In certain markets, such as Europe, the midmarket insurance segment has historically delivered steady profitability even with limited technical rigor around pricing and risk selection. This was largely due to a combination of external conditions and market dynamics that long worked in insurers’ favor. This equilibrium, however, has fundamentally shifted in three primary ways:

- Margin pressure. Profitability in the midmarket segment has eroded as a result of years of underpricing and the limited use of data-driven pricing tools, actuarial models, and risk segmentation techniques to accurately assess and price policies. Deteriorating loss ratios are putting pressure on insurers to raise rates and tighten terms, but competitive dynamics and broker expectations often constrain their ability to do so. The result is falling insurer margins.

- Natural catastrophes. Natural disasters and associated economic losses have significantly increased1 in the past two decades as climate patterns have shifted. For instance, natural catastrophe (NatCat) losses globally totaled $260 billion in 2025,2 and volatility from natural disasters has intensified, complicating the prediction and pricing of risk.3 Because midsize companies often operate from a limited number of sites, typically concentrated in specific regions, they may be highly exposed to single-event shocks such as floods, wildfires, or earthquakes. They also typically lack advanced risk-prevention systems such as engineering-grade protections, business continuity planning, or early-warning protocols. Insurance policies aimed at midmarkets are often not calibrated using prediction models, leading to consistent underestimation of exposure to these risks and, as a result, a possible build-up of risk across the portfolio.

- Emerging risks. Cyberthreats, especially business email compromise and ransomware,4 have been on the rise for some time. The rise of AI technologies creates new regulatory, ethical, and operational challenges around data quality, privacy, and accountability.5 And global interdependencies and logistical vulnerabilities to supply chain disruption increasingly expose businesses to delays, shortages, and increased costs.

These three trends are reshaping the midmarket insurance landscape. The first two—margin pressure and the rising frequency and severity of NatCat events—are already placing a significant strain on profitability and exposing the limitations of traditional underwriting models. In addition, the evolving environment is exposing the weaknesses inherent in applying a relatively light touch when it comes to midmarket management and monitoring of key risks:

- A fragmented approach to underwriting. Midmarket portfolios are often still managed using a case-by-case approach to risk underwriting, without standardized segmentation. This approach limits scalability and makes regular performance reviews impractical.

- Poor risk visibility at the portfolio level. Many insurers lack a comprehensive and forward-looking understanding of their midmarket book. Without aggregated insights across key metrics (for example, the share of policies with substandard grading), underperforming areas could go unnoticed and risk concentrations could build up over time to unsustainable levels.

- The absence of structured monitoring and oversight. Most midmarket portfolios are not supported by formalized steering mechanisms to guide risk management. Unlike retail insurance portfolios, they often lack sequential processes, risk dashboards, or routine governance to guide renewals and new-business intake.

- Underuse of data in underwriting decisions. Midmarket insurers collect extensive internal and external data but rarely embed it into underwriting workflows. In our experience, decisions often still rely on individual judgment, with limited use of tools such as loss predictors or risk scoring engines. This reduces consistency, slows decision-making, and limits the ability to steer the portfolio effectively.

Yet while the changing nature of the market and emerging risks add complexity and require new technical capabilities, they do not necessarily threaten midmarket profitability. On the contrary, they represent a potential growth opportunity: Insurers able to assess, underwrite, and price effectively can offer tailored protection for coverage gaps.

A structured and scalable approach for midmarket insurers

New technologies—especially gen AI and agentic AI—hold the promise of empowering insurers to serve midmarket brokers and agents with greater speed, underwriting precision, and cost efficiency. Yet while technology is an important enabler, any effort to restore profitability and resilience in midmarket insurers must include a structured and scalable model of risk management and mitigation. Our framework presents four execution-ready steps, validated by the performance of leading players and informed by real-time portfolio insights and best practices (Exhibit 1).

Undertake a portfolio deep dive and segmentation

Midmarket insurers will need to take a suite of actions at both the policy and overall portfolio levels to understand risk and segment existing policies.

Assessing policies: At the policy level, insurers should consider establishing a sequential process to clean, standardize, and organize data by line of business (LoB). Relevant KPIs are likely to include the loss ratio across short- and medium-term time horizons; the frequency of claims, including large claims; the ratio between the premium paid by the policyholder and the probable claim cost (the actual premium to technical premium ratio, or AP/TP); the total sum insured concentration; policy risk grading; and the difference between the policy’s vintage and renewal prices.

This approach, and the nested KPIs, can be used to segment the book into four clusters based on the action required:

- Chronic underperformers with limited upside can be pruned. For example, these policies may include those with an average five-year loss ratio of more than 80 percent and an actual price to technical price ratio of more than 100 percent, limiting the ability of insurers to reprice.

- High-risk exposures requiring limit adjustments or stricter terms can be derisked through an increased use of reinsurance or coinsurance structures. These policies may include, for example, those that account for the top 20 percent of the total insured values.

- Midrange performers with potential for uplift via repricing or renegotiated terms can be targeted with actions to recover profitability. These policies could include, for example, those with five-year terms, a loss ratio of 60 to 80 percent, and an AP/TP ratio of less than 100 percent.

- Stable, high-performing policies can be retained, protected, and expanded.

Assessing the portfolio: At the portfolio level, insurers can map accumulated exposure by region, industry, peril, and channel, analyzing exposure trends and peak accumulations to identify systemic risk build-up. For example, one insurer determined that more than 25 percent of its commercial property portfolio was concentrated in areas with a high likelihood of flooding. Through an event-based stress test simulating a severe flood, the insurer found that accumulated losses could exceed reinsurance limits by nearly €50 million, largely driven by numerous claims across multisite manufacturing clients and retail chains. As a result, the insurer refined its underwriting criteria for flood-exposed zones, adjusted pricing to better reflect the underlying risk, and secured an additional layer of catastrophe reinsurance to mitigate potential losses.

Launch a remediation program on renewals

The results of the policy assessment can be used to launch a systematic clean-up effort on renewals. First, insurers can cluster in-scope policies by priority, considering the type of intermediary involved and actions identified. They can then take steps such as holding one-on-one meetings with top agencies to review portfolio performance and define joint actions, while undertaking the rollout of repricing or pruning initiatives directly with brokers given that those relationships are often more transactional. Third, carriers can enact joint commercial-action plans, such as strengthening collaboration between underwriting and sales through combined renewal planning and coordinated meetings with agents and LoB teams. Finally, insurers can identify and define actions that boost the results of the renewal initiative, such as the technical contributions of agents.

Institutionalize a risk-exposure framework for new business

Many carriers still make underwriting decisions individually at the renewal or new-business stage. While this approach can work for assessing individual risks, it often hinders a holistic portfolio perspective across dimensions such as segment, industry, geography, intermediary, or risk quality. As a result, insurers frequently miss opportunities to proactively steer the portfolio by identifying underperforming clusters, managing risk accumulation, or prioritizing profitable growth segments.

While insurers can use event-based stress testing to identify risks and vulnerabilities, they can also institute clear guardrails at a portfolio level to proactively manage risk concentration and establish early-warning triggers to guide underwriting and reinsurance decisions. These guardrails can define quantitative exposure thresholds by peril, geography, industry, and client segment, while a thorough governance structure ensures guardrails are reviewed regularly to assess how well they are adapting to portfolio evolution, market dynamics, and treaty renewals. Carriers also need to pay close attention to the way in which new guardrails are operationalized within the underwriting workflow, including by defining early-warning triggers and related actions and rethinking ways of working.

Monitor and refine over time

To ensure that new guidelines are embedded throughout the organization and have the maximum impact, insurers need to track the actions they take and the impact of those actions on chosen KPIs—and recalibrate when necessary. Key metrics to track, for example, may include the post-renewal loss-ratio delta and the percentage of policies that have been pruned or repriced. Insights from this monitoring should be embedded into overall portfolio governance, including account planning and LoB-level governance meetings. This regular monitoring and impact evaluation can feed fast feedback loops and real-time course correction.

Reaping the rewards: Sustainable growth

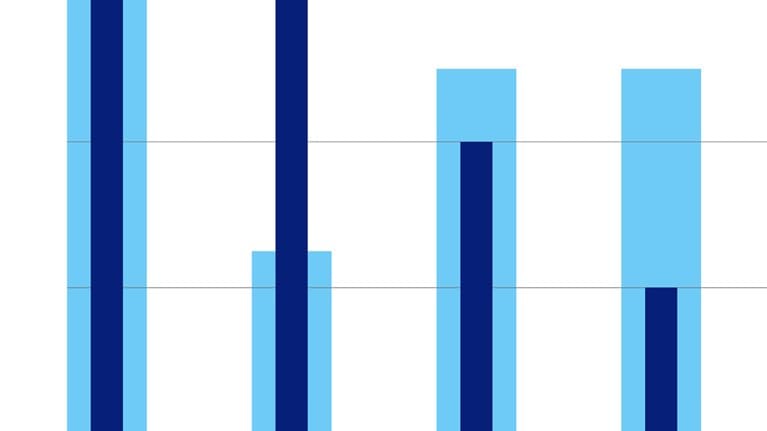

This framework has the potential to unlock significant improvements in profitability. In our experience, insurers can achieve uplift of 30 to 50 percent on gross underwriting results through coordinated action across three key levers: pruning the portfolio, transferring high-exposure segments, and recovering profitability on midrange reformers (Exhibit 2). Combined, these levers may enable insurers to rebalance portfolios toward higher-quality risks, reduce exposure to extreme events, and achieve sustainable improvements in underwriting profitability and portfolio resilience.

Although the current risk environment has exacerbated profitability issues, the volatility of the midmarket segment is structural, not cyclical. Without a disciplined approach, insurers risk continued earnings erosion and capital misallocation. But those acting quickly and decisively to integrate risk management best practices may be well positioned to maintain profitability and capture market share in this strategically important segment.