The insurance industry has experienced a technology revolution over the past decade. Emerging capabilities such as telematics, artificial intelligence, big data, aerial imaging, and claims automation have become more prevalent as insurers have doubled down on using technology for optimization of both cost and processes.

However, not all insurers have been quick to adapt their in-house capabilities. Instead, they have increasingly relied on the platforms and services of a burgeoning landscape of insurtechs, which has witnessed staggering growth in recent years.

We expect insurers’ investments in and partnerships with insurtechs to continue to increase and flourish. In this blog post, we highlight the technology, investment, and value-chain trends that can help guide insurers and investors interested in identifying promising opportunity areas.

Technology trends

Insurtechs offering software as a service (SaaS), artificial intelligence, and machine-learning solutions have been at the forefront of insurtech focus in recent years. Key tech trends include the following:

- innovations in personalized product designs, in which new insurance value propositions from insurtechs reward customers for avoiding risk—for example, telematics that reward customers for safe driving and vitality programs that reward healthier lifestyle practices

- use of machine-learning models to determine potential customer lifetime value and elasticity modeling to complement traditional underwriting models, with external data also being increasingly used to generate optimum price points for customer segments

- a focus on a digital, omnichannel customer experience, further accelerated by COVID-19, reiterating the need for integration of remote and intermediary channels on digital platforms

Investment trends

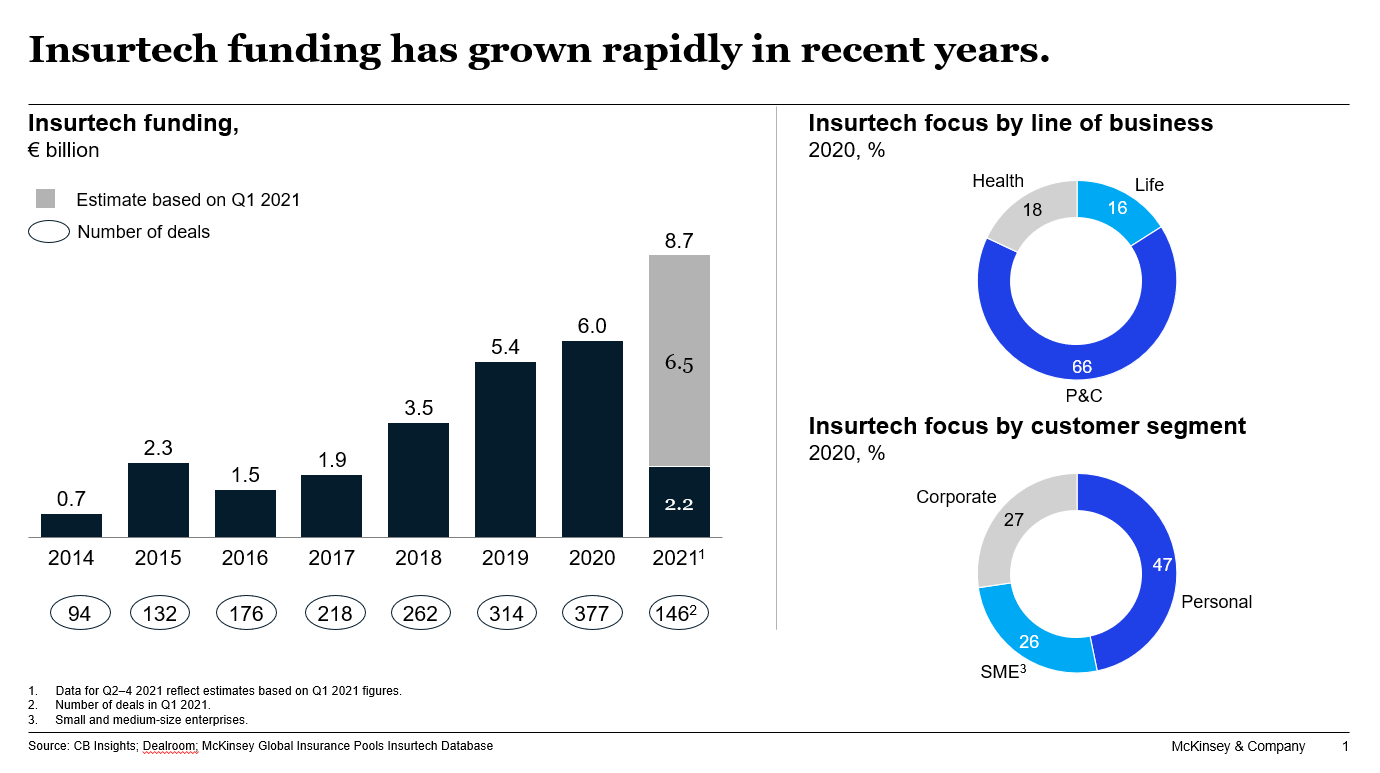

An analysis of approximately 2,000 global insurtechs focusing on life, property and casualty (P&C), and health insurance found that from 2010 to 2020, about one-third of them secured funding, and a handful established strategic partnerships with at least one incumbent. Insurtech funding peaked in 2020 with €6 billion in deals (Exhibit 1).

In terms of product categories, 66 percent of insurtechs operate within P&C lines of business (led by auto insurance), while 18 percent and 16 percent focus on health insurance and life insurance, respectively. Around 47 percent of insurtechs launched between 2000 and 2020 focused on personal lines, with the number that operate in commercial lines increasing in recent years.

The increased funding, coupled with the mounting focus on commercial lines, may push insurtechs to explore new, exciting opportunities, especially in serving small and midsize enterprises (SMEs). The SME segment’s need for customization, experience, and lower complexity of products makes this space ripe for insurtech interest.

Value-chain trends

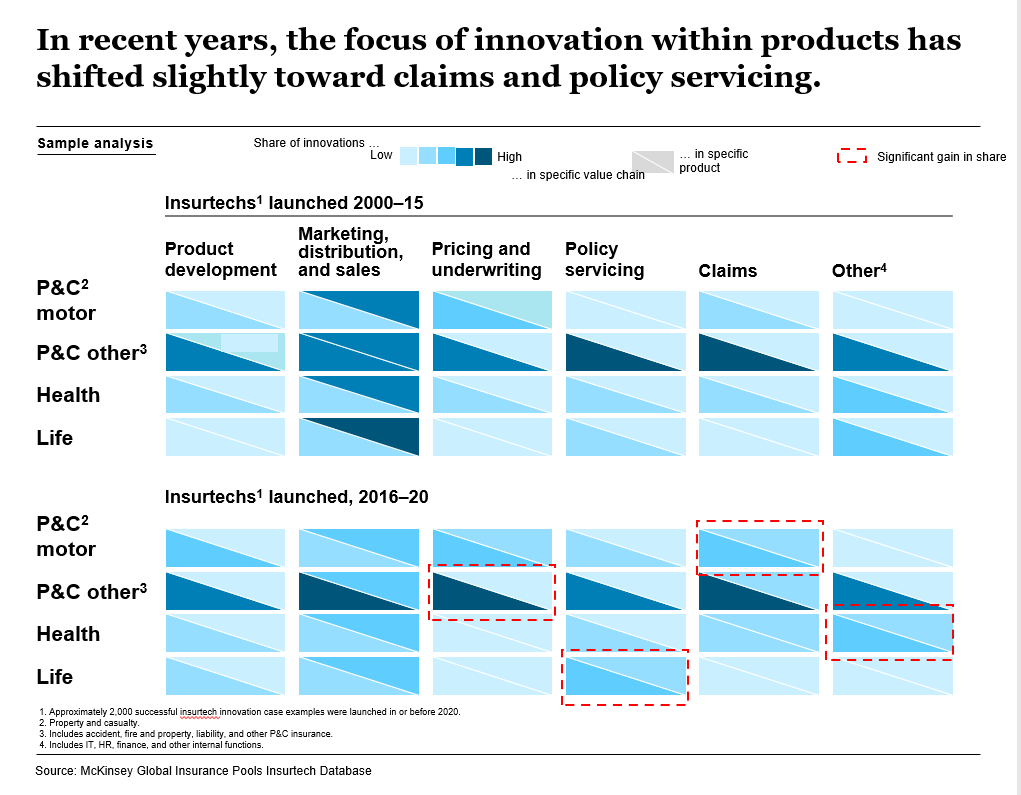

P&C insurance leads other segments, namely health and life, in technological innovation, according to analysis of the McKinsey Global Insurance Pools insurtech database. Across the insurance value chain, the strongest insurtech presence has been felt in marketing and distribution, with a number of insurtechs gaining footholds in investment and partnerships with traditional insurers. However, increasing innovation is also evident in operational aspects such as policy servicing (especially in life), claims (especially in auto), and back-office functions and operations (especially in health). (See Exhibit 2.)

Because insurance is a dynamic industry, the timing of entry and focus is critical. Focusing on the aforementioned themes at the right time can be a distinguishing factor—not just for investment and acquisition but also for mutually beneficial partnerships.

Insurtechs are increasingly ripe for insurer investments and partnerships

The authors wish to thank Ramnath Balasubramanian, Simon Kaesler, Doug McElhaney, Rahul Mondal, Matthew Scally, Katka Smolarova, and Grier Tumas Dienstag for their contributions to this blog post.