In recent years, the assistance industry has demonstrated strong growth: from 2015 to 2020, revenues jumped by roughly 50 percent (see sidebar, “About Assistance Performance Insights”).1 Many insurers have expanded their product portfolios to include emergency assistance services—such as roadside, medical, and travel assistance—as a way to enhance their value propositions and deepen their relationships with customers.

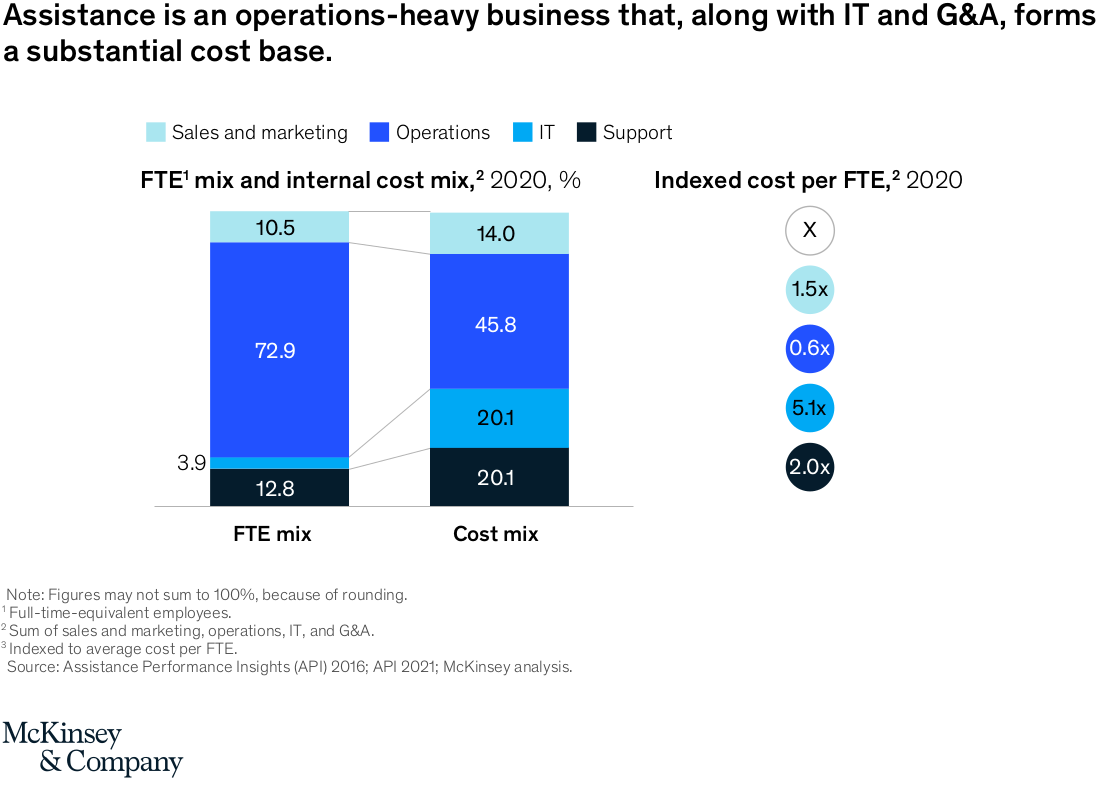

However, the business model presents a number of challenges inherent in maintaining and scaling a global footprint—including people-intensive operations, complex products and processes, and significant IT requirements (exhibit). At the same time, assistance companies face increasing pressure to adapt their business models in response to changing consumer behaviors and a growing demand for integrated solutions.

The COVID-19 pandemic exacerbated many of these challenges, with varying effects on individual business lines. Not surprisingly, travel was hit the hardest, with revenues falling by up to 40 percent from 2019 to 2020. Meanwhile, revenue in the assistance and health segments grew by approximately 5 percent and 15 percent, respectively, over the course of the year. The overall effect, however, was largely negative, even as some players partially offset losses by sustaining customer renewal rates (especially in roadside assistance) and renegotiating contracts with third-party providers. The industry is showing promising signs of recovery, with some leading players achieving growth of 10 percent in 2021, according to public data. This growth is likely driven by widespread consumer trends, including the opening up of travel and sustained demand for assistance products.

As we begin to emerge from the pandemic, forward-looking assistance companies have made progress in refining their operating models and optimizing their underlying cost bases. However, there is still a long road ahead for companies to transform and fully embrace a digital and global operating model. Our analysis shows that leading assistance players2 have taken a number of actions to drive operational efficiencies, including the following:

- Investing purposefully in IT. Leading assistance players’ IT spending increased by nearly 20 percent between 2015 and 2019, with an additional 15 percent increase from 2019 to 2020—partially to facilitate remote working and digital customer experiences. Our research shows that insurers that make large, targeted IT investments achieve higher growth and better performance compared to their peers. Critical areas for IT investment include marketing and sales, underwriting and pricing, policy servicing, and claims.

- Improving productivity. From 2015 to 2019, employee productivity3 among leading assistance players grew by 20 percent, followed by a marginal dip in 2020 due to the hiring of specialized roles in IT and central functions. Over the same period, the cost ratio for G&A functions4 improved by more than 15 percent—mostly driven by companies with localized G&A operations in low-cost labor markets (compared to centralized operations in high-cost European markets). While these are clear signs of progress, companies that push to reimagine their G&A functions can further reduce costs and increase efficiency while improving the quality of their service.

- Reducing external spending on sales and marketing. Confronting pandemic-related revenue losses in 2020, leading assistance players cut back on direct spending in sales and marketing, such as promotional expenses and external vendor contracts. These reductions can typically be made without a significant impact on business operations and can help companies redirect valuable resources to more immediate priorities.

To compete on a global scale, assistance players must go beyond optimizing their existing operations and pursue a reinvention of their business model. This will require a marked shift in cost performance and productivity, enabled by advances in digital capabilities and technology. Companies will need to forge innovative digital partnerships (for example, with third-party administrators); tap into attractive, high-growth areas (such as the mobility revolution); and take advantage of strategic M&A opportunities to enter new markets and product segments.

As with the broader insurance industry, the assistance industry shows promising signs of rebound—but future growth is not guaranteed. The next normal will require companies to constantly transform their business models and reimagine their roles in the broader ecosystem.

Download the article here.

By Suneet Jain, Ulrike Vogelgesang, and Christoph Weber

1 All statistics and analysis are based on McKinsey’s Assistance Performance Insights, 2015 to 2020.

2 A subset of assistance players in the Assistance Performance Insights benchmark that adopted measures to improve efficiency.

3 Full-time equivalent employees (FTEs) per $100 million in revenue.

4 G&A functions include finance, HR, facilities, audit, compliance, and other support functions.