Insurance companies should pay close attention to insurtechs—not because they’re coming to attack, but because they're coming to collaborate. For established insurers, insurtechs can be digital enablers that drive the adoption of digital technologies along the value chain. To realize the potential, it’s important that both sides focus on the strength they’re bringing to the table.

Insurtechs are maturing

According to McKinsey research, more than $10 billion has been invested into insurtech since 2012. And, while investments have somewhat tapered off in recent years, we have observed three key trends that underscore how the insurtech space has developed and matured over time: diversification, professionalization, and collaboration.

In the beginning, insurtechs focused primarily on P&C and distribution. Now, digital technologies play a role in many more areas. Diversification highlights the fact that insurtechs today are creating digital solutions along the entire business value chain as well as across all lines of business. This allows for many more avenues for integration into existing business models.

The second trend, professionalization, typically accompanies maturity. To survive in the highly complex insurance market, insurtechs must stay abreast of new rules and regulations. Innovation is driven by companies willing to take big risks, but it also requires patience, careful planning, and a solid go-to-market strategy.

Which leads to the third trend: collaboration. Currently, less than 10 percent of insurtechs are seeking to disrupt the insurance business model, while nearly two-thirds focus on specific parts of the value chain, aiming to meaningfully integrate with established insurers. The challenge is no longer “insurtech versus traditional insurer”—but rather how the two can work together to create tangible value for the customer.

When considered comprehensively, these three trends are clearing the way for a new industry model, in which insurtechs and carriers work together closely to drive the digital transformation of the industry.

Partnering for strength

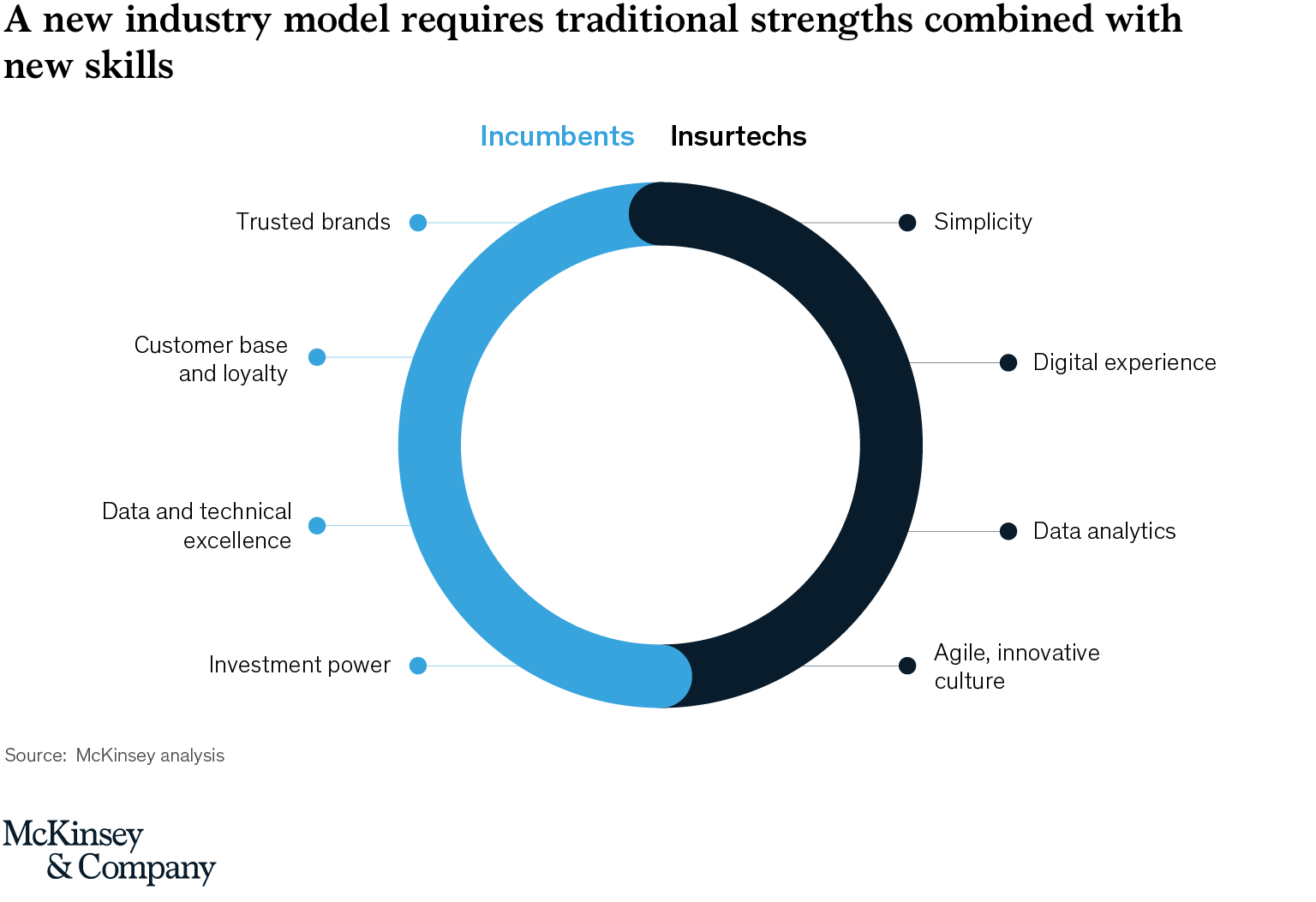

What the winning model of collaboration will look like remains to be seen, but it's clear it will require a combination of traditional strengths from established insurers and new skill sets brought by insurtechs (exhibit).

Traditional strengths: Many incumbents benefit from the fact that they are trusted brands, with hard-won reputations earned through decades of service to customers. This loyal existing customer base has also generated huge volumes of data that offer the potential to shape strategy and consumer engagement. Robust teams of experienced, skilled employees—from underwriters to claims agents—provide incumbents with a strong operational foundation. Furthermore, the size of incumbent carriers affords them the financial security to enter new markets, make strategic bets, and support the rollout of new products and enhanced services.

New skills: Insurtechs are often start-ups with simple business models and narrow areas of focus, whether it be artificial intelligence or machine learning. In addition, many insurtechs have data-analytics capabilities. They are digital organizations with the ability to respond to market opportunities much more quickly than global insurance companies. As such, they are more likely to boast an agile culture that pursues and rewards innovation, as well as a mind-set that puts them at the forefront of changes in the industry.

It’s easy to see the complementary nature of incumbents and insurtechs. The challenge becomes finding the “sweet spot,” where collaboration is most successful—and then implementing it. It’s a shift in thinking, but there are ways to make collaboration easier. Traditional insurers working with open platforms, for example, are facilitating the integration of new digital solutions via standardized application programming interfaces (APIs), which many insurtechs offer.

The future industry model will be shaped extensively by partnerships where incumbents retain ownership of the end customer while insurtechs act as digital enablers that drive the adoption of digital technologies along the value chain to help advance the digital transformation journey. Players that realize the potential of digitization early are likely to further benefit from the strengths both sides bring to the table.