The contagion that started in homes in 2007 has spread to offices and shops. Commercial real estate (CRE)—one of several asset classes severely affected by the global crisis—has seen property values decline by over 25 percent in many markets, with some experts predicting an eventual drop of more than 50 percent for the worst affected regions. Most banks are deleveraging significantly, some to ensure their own survival; for many, this deleveraging includes a sharp curtailment of CRE lending. As a result, financing for CRE has dried up significantly. Some large property groups, unable to refinance as balloon payments come due, have already defaulted. A few have even filed for bankruptcy. In short, the commercial property industry and its lenders find themselves in the midst of a downward spiral.

Given this bleak outlook, there is perhaps no better time for a look inside the opaque CRE finance industry. Many CRE lenders find it difficult to understand how their performance stacks up against that of their peers. And few can say with any certainty how top performance is achieved. These gaps in understanding put banks at risk; if they misunderstand their economic performance, they will also likely miss critical opportunities to improve their business models. Such an opportunity might well be at hand as the financial crisis passes and the new reality sets in.

To help banks understand this business better, McKinsey & Company launched its initial Commercial Real Estate Finance Survey, one of two McKinsey surveys focused exclusively on commercial real estate.1 Eight large European banks took part in the initial survey; several others granted supplementary interviews. Collectively, we estimate that these two groups comprise about 40 percent of the CRE loans outstanding on balance sheets across Europe. Our survey spanned 2006 and 2007, the final two years of the property boom, providing a clear picture of how the industry performs in good years.

Our research has produced two key findings. First, the industry as a whole does not return its cost of capital (defined as equity) even in the best of times, let alone over the business cycle. Put another way, the “profits” recorded in good times are in fact economic losses to equity holders; worse, they fail to provide a cushion for the significant losses that come in industry downturns. In our view, as we will explain, the primary culprit is poor deal selection and, more specifically, a failure to adequately price the underlying risks. Other factors include a lack of revenue diversification and cost inefficiency. Because of these dynamics, we expect that even after the current crisis has faded, the CRE finance industry will continue to destroy value.

That said, some CRE lenders do in fact generate returns exceeding their cost of capital—our second finding. Top-performing lenders have developed a thoughtful approach to their business, choosing their customers with care, concentrating on the markets they know best, and taking a deliberate view of the many risks inherent in property markets. Furthermore, they have kept their businesses at a manageable size, moving countercyclically to reduce volumes.

These top performers have exercised admirable prudence, and many are now reaping the benefits of a seller’s (i.e., a lender’s) market. The rest are struggling. Troubled lenders should not let a good crisis go to waste. They can take advantage of the lull in their business to enrich their understanding of the ways top performance is achieved and build the capabilities such performance requires. Banks that can establish these skills and processes soon will be well placed to capture an outsize share of the economic profits of this important market once the crisis has passed.

A fundamentally challenging industry

Our analysis of the core problem—banks’ inability to turn economic profits in CRE finance—starts with the ease with which any large pool of capital can enter this business. CRE lending can generally be conducted using the support groups and systems that almost any commercial or investment bank already has in place. No branch network is needed, though a few offices in key locations that can house some origination activity are helpful. It is a transaction-based business—relationships count for less than they do in, say, corporate lending. CRE borrowers tend to maintain relationships with many CRE lenders in the absence of any material switching costs. And the business is essentially based on one easy-to-deliver core product.

Because there are few barriers to entry, excess capital is often deployed in CRE finance, distorting the economics of the business. Many CRE proposals receive bids from several lenders, some of them from entrants that are less cognizant of risk and content to accept lower relative returns. These players often win the deal, setting the market price at the margin. The period of loose capital that started in late 2001 and ended in 2008 was only the most recent and vivid example of this phenomenon in action. During this period of increasing commercial property values, CRE lenders accepted ever lower margins and ever higher “loan-to-values” (LTVs).2 By the end, pricing on CRE loans reached historic lows at a time when the underlying riskiness of such loans reached unprecedented heights, due in part to the inflated pricing of the financed properties.

Seeing this phenomenon unfold, some lenders grew concerned and pulled back in early 2007. But most did not; they continued to compete with other CRE lenders and investment banks—which offered cheap funding via their commercial mortgage-backed securities (CMBS) businesses—and placed their trust in the seemingly perpetual rise in commercial property prices. These lenders were left with a razor-thin margin for error, even as their borrowers became increasingly vulnerable to vacancies and other cash-flow problems.

These optimistic lenders, in other words, consistently fail to price the rising risk of default and property market declines into their loans. And even those banks that, spotting the risks, try to charge more for them often find themselves well off the market as others undercut their offers. The result is that, in aggregate, CRE lenders do not return their cost of capital—even in good years.3

The challenge of CRE lending is well illustrated by a look at its underlying economics (Exhibit 1). In 2006, our survey respondents, on a weighted-average basis, generated a lending-related margin of 141 basis points (bp), expressed relative to the CRE loan book,4 with cross-selling income from products such as derivatives and deposits adding another 6 bp. But operating costs totaled 43 bp and banks spent 22 bp on risk,5 leaving our respondents with a net profit before tax of 82 bp. With a pretax cost of capital that we estimated at 99 bp, these banks failed to record an economic profit in a year that saw commercial property prices soar. Not surprisingly, our respondents as a group did not fare much better in 2007, an even better year for commercial property.

A loss-making industry

The drivers of performance

While the industry as a whole underperforms, some CRE lenders thrive. In our survey, two institutions exceeded their cost of capital in 2006, while three managed this feat in 2007, surpassing the 15 percent pretax threshold by a wide margin in some cases. As measured by 2007 pretax return on equity (ROE), the top three performers in our sample achieved an ROE that was more than 50 percent higher than that of the bottom three, after normalizing for differences in Tier 1 capital levels. The inferences we draw from this discrepancy must take into consideration the modest size of our survey group. Nonetheless, we believe that a review of the survey data provides a fundamentally sound view of what these top performers do that others do not.

Our analysis allowed us to form a picture of top-performing CRE lenders that looks something like this: they 1. target only established, close-to-home markets; 2. build a narrow portfolio featuring only a few property types, client segments, deal types, and ticket sizes; 3. countercyclically manage the size and growth of the loan book; 4. generate healthy cross-sell margins with a lean infrastructure; and 5. invest significantly in risk management.

How did this picture of outperformance emerge? Let us start with the factors that do not explain it. One might expect that top performers do better on the lending margin. However, lending-related net interest and fee margins fail to explain the difference, with top performers’ lending fee margin actually 30 percent lower than that of the ROE also-rans (Exhibit 2). Cost/income (C/I) ratio also fails to account for the variance. The C/I ratio of the underperformers came in almost 10 percent below that of the top group.

The differentiators of performance

It is only when we review other less conventional metrics that we observe differences that might explain the performance gap. Top performers boasted a cross-sell margin over 150 percent higher than that of banks on the bottom. That is an important distinction, though not as important as the way these two groups treat risk. The ROE laggards needed to make greater loan-loss provisions than their higher-performing counterparts (about 20 bp higher). Thanks to countercyclical loan-loss provisioning in 2006 (that is, making conservative provisions as markets peaked), top performers benefited from write-backs in 2007 as their loan books outperformed relative to peers in another boom year with low actual losses. Write-backs actually allowed these institutions to reduce their loan-loss reserves (via negative loan-loss provisions), while the laggards were forced to replenish theirs as their loans deteriorated beyond initial expectations.

On another risk measurement, the average risk-weighted asset (RWA) level (relative to CRE loan book) of the top performers stood almost 20 percent below that of the bottom group—a substantial difference. While it is difficult to say which of several potential factors (including capital adequacy models, the underlying risk of the loan book, and off-balance-sheet activity) might be responsible, anecdotal evidence from our interviews suggests that the top performers sought a lower level of underlying credit risk than others for the same lending-related margins, implying superior deal-selection skills.

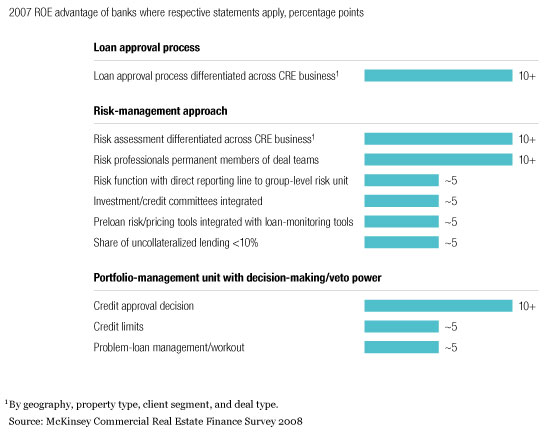

In other words, though their lending margins often lag behind those of their peers in absolute terms, top CRE lenders ultimately generate higher risk-adjusted margins. They achieve this because they manage risk differently. They monitor it more precisely, considering it across geography, property type, client segment, and deal type (i.e., investment or development); lower-performing institutions, on the other hand, tend to take a uniform, one-size-fits-all approach to risk (Exhibit 3). Top CRE lenders also differentiate their loan approval processes across each of these dimensions; once again, the laggards tend to use one process throughout. And at top institutions, risk professionals are full-fledged members of deal teams. Further, the risk function is headed by a peer of the lending-unit head, to ensure objectivity and avoid conflicts of interest. Top performers also empower and integrate their credit-portfolio managers, directly involving them in key decisions regarding loan approval, credit limits, and problem-loan management. Their portfolio managers wield significant influence in building and managing the loan book.

A differentiated approach

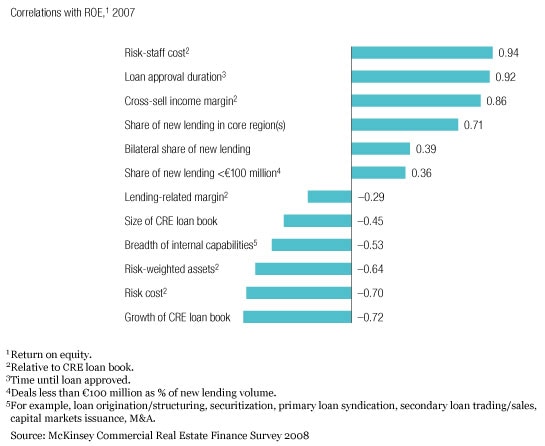

To verify these insights about top ROE performers, we analyzed several dimensions of respondents’ operating models and calculated the correlation of these variables with ROE (Exhibit 4). While the correlations are not statistically significant, we nonetheless believe that they are indicative of their respective contribution to financial performance.

Achieving top performance

For example, we discovered that investment in risk-management staff features the highest positive correlation with ROE. Top players simply have more expensive and presumably higher-caliber people dedicated to scrutinizing the fine print. Similarly, higher ROEs are linked to more rigorous loan approval processes, with top performers taking the time necessary to perform effective due diligence.

Other strongly correlated practices speak in various ways to the focus of top firms. These banks squeeze each deal for its full potential, deriving more income from cross-selling other products. They concentrate their efforts in a few well-defined regions, with most of their new lending done in places that they understand well.

To a lesser degree, two other dimensions are also associated with higher ROE. One is the share of new lending that is bilateral—that is, by a single lender to a single borrower, without any syndication or subsequent securitization. Top performers do more bilateral lending than others. When CRE lenders do not share risk, they naturally take greater care with regard to due diligence. Another dimension is deal, or “ticket,” size. At the better performers, smaller deals (less than €100 million) constitute a higher share of new lending volume.

Some other variables have strongly negative correlations with ROE, including the size of the loan book and its growth. For example, aggressively expanding the loan book in 2007—when the market was topping out—would have been a mistake. Heavy loan-loss provisioning and high RWA levels, as suggested above, were also not characteristic of the best performers in 2007.

One of the more interesting negative correlations deals with the breadth of capabilities housed within the CRE lending units themselves. Logic dictates that units with a lot of ancillary capabilities need to generate significant additional revenue to justify their higher cost. In times of lean revenue, the additional overhead can act as a significant drag on earnings. Whereas top performers tend to maintain leaner cost structures, calling on capabilities in other parts of the bank as needed to generate incremental revenue in a cost-efficient manner, laggards often develop in-house services and capabilities, frequently in “fancy” areas such as M&A, tax advisory, capital markets, and secondary loan trading—but often struggle to cover their incremental cost even in the best of years.

Improving CRE lending

Since the onset of the global financial crisis, the supply-demand imbalance that previously favored borrowers has shifted 180 degrees—this in spite of a simultaneous collapse in transaction volumes as most CRE investment proposals have been shelved. Why do lenders now have the upper hand? The virtual disappearance of the CMBS market, a growing wave of write-downs, the increase in capital requirements as loan books deteriorate, and the limited availability of capital have drastically constrained the balance sheets of most CRE lenders. Supply has thus fallen even further than demand.

The borrowers that remain are mainly in the market to roll over their maturing debt. Their search for lenders has grown increasingly desperate. Margins have gone up—in Western Europe, net interest margins have widened by 100 percent or more in some cases. Top players that exercised prudent restraint in those boom times can today more easily write profitable, lower-risk business while taking the necessary steps to limit loan losses in their current book of business.

But these banks are few. For the rest, in addition to loss mitigation, another challenging task awaits. Many banks conceive of it as slashing costs. But we argue that there should be more to it than that. Banks should view the current crisis-induced lull as an opportunity to build a viable business model for the world after the crisis—a model that enshrines attention to detail in a business where every dollar or euro counts.

Limiting loan losses today

Some experts forecast that the peak annual charge-off rate (net of recoveries) in the United States will approach 4 percent (relative to CRE loan book)—twice the approximately 2 percent rate experienced during the commercial real-estate bust of the early 1990s. These experts base their view on high current charge-off levels relative to timing in the cycle, and pre-crisis capitalization, or “cap,” rates (the ratio between a property’s net operating income and the price paid) that bottomed out about 2 percentage points lower this time around. Historical charge-off data for Europe are harder to come by, but to many observers, a similar peak rate of about 4 percent in some markets that overheated in recent years seems conceivable. At these levels, a single year of charge-offs would be equal to over four good years’ worth of pretax profits6 (survey respondents generated a weighted-average pretax profit margin of 91 bp in 2007).

Clearly, an immediate and necessary step for all banks is to improve their loss-mitigation and, especially, their workout capabilities. In our view, banks that successfully upgrade these skills can reduce the level of nonperforming loans and increase loss recovery rates, which could potentially lead to a reduction in loan losses of 10 percent to 15 percent. For a bank with a €10 billion CRE loan book and a two-year cumulative loss rate (relative to CRE loan book) approaching the 7 percent that some experts foresee as their base-case scenario, that can mean salvaging an extra €70 million to €105 million for the bottom line on a pretax basis.

In the recent boom, CRE lenders did not see the need to invest in large workout organizations. Now, given the unprecedented scale and pace of deterioration in many markets, banks urgently need to expand their workout units—no small matter, as these skills are hard to come by. And they must attend to two other requirements: first, adopting new strategies to recover value, as early exits in many cases are no longer feasible; second, strengthening their early-warning systems—which fared poorly in the crisis—to identify troubled loans and preempt significant value erosion. These moves will help banks establish the needed comprehensive approach to loss mitigation.

Building a business model for the future

Although lending margins at present appear healthy, CRE lenders should not fool themselves—the post-crisis world may not be as rosy as many think. We agree that lending margins will likely remain higher for a time, but we believe that this relief will be transient. As the next property boom takes hold (or perhaps even before), memories will fade, capital will reenter the business, competition will increase, and a willingness to downplay risk will once again push industry margins down.

Furthermore, a new era of regulation and, for some, a new kind of shareholder will likely complicate the lives of CRE lenders in myriad ways. It seems clear already from the guidance provided by regulators and policymakers that capital requirements for most lending businesses, including CRE finance, will increase. And as governments take stakes in banks, these new owners will likely seek, whether subtly or overtly, to influence the way lenders distribute their CRE business. If governments should impose, say, domestic lending requirements on the banks they “own,” that could undermine banks’ need for more careful risk assessment and pricing discipline, and could reduce lenders’ ability to select the most attractive deals.

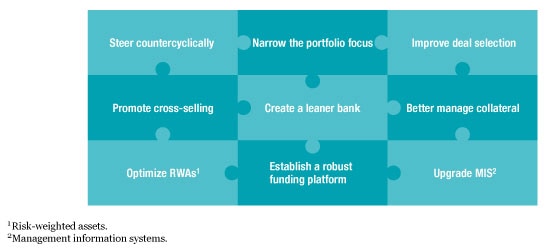

Given this challenging outlook, CRE lenders must take advantage of every opportunity and leave no stone unturned, whether in pricing, cross-selling, cost efficiency, risk management, or capital efficiency. CRE lenders must now begin to reshape their business models and integrate nine levers that we believe will drive strong, sustainable returns in both good and bad times (Exhibit 5).

Reshaping the business model

Steer countercyclically. In boom times, banks must avoid economically unprofitable new business at the margin and take advantage of the prevailing irrational exuberance to make portfolio sales. The survey reconfirmed what we had suspected for a long time: the best players did not grow in 2007. They did not work under the assumptions that “we need to grow to maintain our market share” or “we have to accept pricing levels because they are set by the market.” With admirable prescience, the top performers rightsized their loan books by selling into a rising market, sparing themselves considerable crisis-related trouble. To steer the business counter-cyclically is very difficult: it requires tremendous discipline from top management, a clear view of the credit cycle, and a commitment to long-term value creation, even at the expense of short-term earnings. Despite these profound difficulties, mastering countercyclicality is worth it, as it is an enormous source of profitability.

Narrow the portfolio focus. Lenders should select a limited number of geographies, property types, client segments, deal types, and ticket sizes. Our experience suggests that a tightly controlled portfolio is a substantial lever of profitability. Picking the right categories starts with a careful analysis of both the administrative and risk costs associated with each category—what we call all-in profitability. Very often, transactions with high margins are the least profitable. For example, small development loans might pay 100 bp more than a large investment loan with a middling LTV. But after accounting for the true cost of risk, and the very high administrative cost of handling a small loan relative to a large one (per dollar or euro of loan value), these small development loans are much less profitable than they appear and may even destroy value.

Improve deal selection. Once the target portfolio is defined, banks should identify the most attractive risk-adjusted deals within each category and go all out to win this business. As noted, many banks struggle with deal selection. A poor relationship between origination and risk often lies at the core of the problem. Each group has its own objectives, and these are seldom aligned. In our experience, a joint review of strategy by the front office and risk groups represents the best fix. As soon as origination and risk strategies are jointly developed and hence aligned, senior managers in both groups will more readily support it. These managers should then translate the shared strategy into a collaborative step-by-step selection process, from which the bank may only deviate under predefined (and extremely rare) circumstances—a far cry from the current practice at many banks.

Promote cross-selling. Banks must generate profitable ancillary income without creating a bloated infrastructure. There are products and services that can boost ROEs significantly without requiring big investment and new infrastructure. Among these are derivatives, which are often sold in conjunction with new loans. Most, but not all, CRE lenders offer interest, foreign-exchange, and property derivatives products. Those that do not should add these products to their portfolios. Banks can also offer tax optimization solutions that are not related to loans but leverage the lending relationship. Finally, some players successfully cross-sell commercial banking products such as payments and deposits. Naturally, this only makes sense for lenders with a commercial operation, and even then challenges abound; strong cultures and internal politics often stand in the way.

Create a leaner bank. CRE lenders should streamline their business to better contain costs and achieve best-in-class operational efficiency. Given that every basis point counts, this is an important source of profit. Some CRE lenders have already invested significant effort, improving end-to-end credit processes (sometimes using lean-manufacturing principles), standardizing all other critical activities in accordance with best practice, simplifying product portfolios (such as cutting nonlending products that do not add value), closing subscale locations, and so on. Most CRE lenders, however, still have significant potential to improve operational efficiency. On a related note, some banks compensate their CRE staff lavishly, particularly on the origination side. Banks should bear in mind that CRE lending is not investment banking, and with few exceptions (such as for staff with special, highly valued skills), they should not compensate as such.

Better manage collateral. Banks should improve their ability both to monitor the value of their collateral, continually and in near-real time, and to protect and maximize that value. In recent years, many CRE lenders grew lax about the accurate and timely valuation of collateral; they may have relied on the conventional wisdom that property prices would only rise and LTVs could only fall. As CRE lenders originated deals at ever higher LTV levels, they left themselves with an insufficient cushion of collateral. The market turned, lenders realized much too late that they were undercollateralized, and they had to learn again about the difficulty of selling collateral into a falling market.

CRE lenders must institutionalize an ongoing collateral valuation process that supports a disciplined overall collateral-management approach, irrespective of boom or bust. The approach should also include the establishment of a “remarketing” network of potential buyers, especially those CRE investors that are willing to pay above-market prices in exchange for a first look at strong properties, and the development of the asset restructuring and active asset-management skills necessary to safeguard the collateral until a more opportune time for exit.

Optimize RWAs. Lenders must better manage their RWA structure to reduce capital requirements and get a bigger “bang for the buck.” In our experience, programs to reduce capital waste can lower the level of RWAs for a given credit exposure by 10 percent to 15 percent, resulting in a commensurate increase in revenue per RWA. We have identified more than 100 levers to this end, ranging from revisiting risk-model assumptions to the above-mentioned proper and timely accounting for collateral. While such optimization does not change the underlying risk of the loan book, it can provide capital relief, thereby boosting ROEs.

Establish a robust funding platform. A full spectrum of funding sources is essential to CRE lending success. Prior to the crisis, this issue attracted little notice. Many CRE lenders that are part of larger banking groups did not have their own dedicated funding operations and instead relied on the group’s treasury. Others relied on “maturity gapping” as a source of both funding and apparently limitless incremental profits. The crisis has shown the inadequacy of both these approaches.

For some time to come, banks will need to rely primarily on their own balance sheets for funding. CRE lenders with the capability to issue covered bonds—and the Pfandbrief, in particular—will have a significant funding advantage, as spreads between secured and unsecured funding are unlikely to return to pre-crisis levels anytime soon. While club deals7 will dominate larger transactions for some time, syndication in the more traditional sense (and subsequently plain-vanilla CMBS) will eventually come back. In anticipation, CRE banks must build the requisite capabilities to exploit these sources of funding, and—when market conditions justify it—be prepared to tap into them.

Upgrade MIS. Lenders’ management information systems (MIS) must be robust enough to capture the information that is critical to steering the business. Ideally, such systems should deliver, among other things, a granular view of the business by geography, property type, client segment, deal type, ticket size, and staff. Not surprisingly, MIS is a broad topic, and we will touch only on one part: the role of MIS in deal selection.

Many players’ MIS-driven deal selection tools and methods are too simplistic. For example, our survey showed that some players use a minimum net interest margin as their hurdle rate, a relatively useless measure for distinguishing between desirable and value-destroying deals. Other players use ROE or economic value added—but their systems often fail to account for the vast differences in acquisition and production costs associated with varying deal types or ticket sizes. In many cases, these tools are also not sensitive enough to fully capture a true picture of risk cost, nor do most factor in broader portfolio considerations.

We have seen banks that believed they had the right tools and were doing business in certain geographies at levels that exceeded their hurdle rate. However, a closer look revealed that these markets were not profitable and that the loans often did not earn their cost of capital. Ultimately, the solutions for such MIS-related issues will vary significantly among CRE lenders, depending on their respective starting positions.

CRE finance represents perhaps one of the most competitive businesses in banking. As our research confirms, however, it can be a very attractive one for those lenders that design their business models with great rigor and manage them at a level of detail and attention more commonly found in an institutionally established manufacturing business.