Amid unprecedented market turmoil, many banks are now rightly focused on shoring up their short-term performance and even, in some cases, ensuring their survival. With so many open questions—How deeply will the global recession bite? How aggressively will regulators react to the crisis? How quickly can balance sheets be rebuilt?—long-term strategy has received little or no attention. And yet, almost unnoticed, one topic has advanced from distant issue to discernible opportunity: the transition to the low-carbon economy.

The global response to the problems of climate change will entail a massive shift of industrial and financial resources. To cut emissions of greenhouse gases (especially carbon dioxide), consumers, companies, industries, and even entire countries will have to abandon current forms of carbon-based consumption and switch to new, less-polluting alternatives. Vast sums of capital will be required to fund emission-reducing projects and infrastructure. New industries will be forged, going far beyond the nascent companies we see today. New financial products and markets will be necessary to manage and transfer the risks and costs of carbon emissions. Increasingly forceful regulatory intervention will drive unprecedented shifts in cash flows and valuations. Investors and regulators will demand better information about the economic impact of climate change.

This shift has already begun. And as cap-and-trade schemes and other regulations proliferate and more companies and industries come within their ambit, the need for financing and trading will grow enormously. Banks, investors, and exchanges have critical roles to play in shaping this transition to a low-carbon economy. Speaking in January 2009 at the World Economic Forum in Davos, Lord Stern, author of one of the most influential reports on the impact and costs of climate change,1 had the following to say about the role and opportunities that climate change could create for banks:

Banking could do very well as [the world] moves toward a low-carbon economy. There will be lots of business opportunities. . . . [B]ankers are particularly strong in this area. They have been very creative over all kinds of issues and they could do it again in the financing of green initiatives.2

By our reckoning, banks’ revenues from just a small subset of carbon trading and infrastructure financing and advisory activities may reach $15 billion in 2020; industry revenues today from all corporate and investment banking activity are in the vicinity of $250 billion. Although responding to climate change will not fully ease banks’ current woes, it can nevertheless be an important part of the puzzle—and one that banks overlook at their cost.

The future has arrived

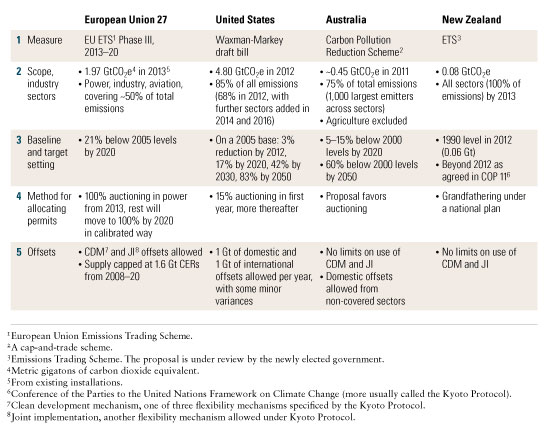

Already, climate change is altering the business environment in which banks and their clients operate. Many parts of the world have begun to ask the businesses to bear the costs of the carbon emissions they create (Exhibit 1). The European Union, for example, has agreed to widen the range of industries covered by its pioneering Emissions Trading Scheme (ETS) and to enforce on these industries a minimum 21 percent reduction of carbon emissions (from 2005 levels) by 2020. The EU has also left the door open to tighten the target further. The new US Congress has suggested that by 2020, the United States must reduce its emissions by 17 percent from 2005 levels, in part by implementing a cap-and-trade system that will cover 66 percent of US emissions. Similar schemes are planned for Australia and under discussion in Canada, Japan, and New Zealand. And such action is not limited to the developed world; Mexico and South Africa, for example, have both made formal commitments to reduce emissions.

Proposed cap-and-trade markets

Business has also been affected by climate change in other ways. Take dealmaking, for example. The $45 billion private-equity purchase of energy utility TXU in 2007 hinged on the buyers’ insistence that TXU scale back its plans to build 11 new coal-fired power plants and instead boost investments in energy efficiency, clean coal technology, and renewable energy. On another front, activist shareholder alliances such as the Carbon Disclosure Project—an alliance of about 385 investors managing more than $57 trillion of assets—are stepping up their demands that companies disclose their emissions data so that members can make more informed investment decisions.

In recent months, many governments looking to stimulate their economies have identified low-carbon investment as a compelling source of jobs, growth, energy security, and emissions savings. Stimulus packages in the United Kingdom, the United States, Mexico, China, and elsewhere include provisions for spending on green projects. The Obama plan, for example, allocates $100 billion to be spent on energy efficiency, mass transit, modernizing electricity grids, and energy-focused R&D.

Despite this rapid and far-reaching change in banks’ operating environments, the response from the banking sector has so far been muted. Our discussions with industry players suggest that even those banks that are taking action are doing so in a mostly ad hoc way: tackling their own carbon emissions or opportunistically pursuing occasional financing, investment, or advisory opportunities. And even at those few banks that have drawn up some sort of strategic agenda for climate change, the impetus often comes from within the corporate-social-responsibility group, or even the facilities-management function—areas far from the business’s core decision makers.

Creating the low-carbon economy

To avoid being left behind in the world’s transition to a low-carbon economy, banks must seize the opportunity. We see four broad ways in which banks can both contribute to and profit from the shift: industrializing the market for carbon, financing and investing in the low-carbon economy, creating transparency into carbon-related costs and value, and driving innovation.

Industrializing the market for carbon

By assigning a cost to carbon emissions, regulators have also created a new asset class: carbon allowances, or permits to produce a fixed amount of greenhouse gases during a year. The European Union, for instance, issues allowances to companies in industrial and energy sectors. Companies that exceed their allowances can buy them from others, or they can buy “offsets”: investments in abatement projects, almost always in less developed nations, that can be set against the company’s excess emissions. These offsets can help alternative technologies that are currently uneconomic (compared with the higher-carbon technology they would replace) turn a profit. Banks can finance and intermediate these offsets, make markets in the nascent exchange-traded carbon allowance products, and design, sell, and trade new derivative products.

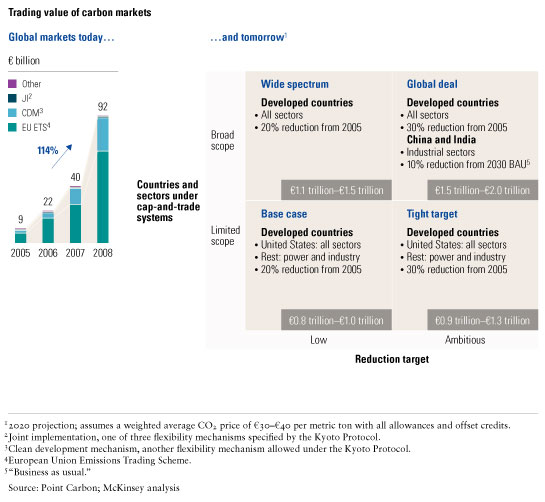

Although still relatively small (with traded volumes of about $92 billion in 2008), global markets for carbon credits and offsets, we expect, should grow to at least $800 billion and possibly as much as $2 trillion by 2020 (Exhibit 2). At that size, they would be more than twice as large as the global commodities derivatives market was in 2007. A big part of the growth will come from offsets. Our research suggests that if the developed world agrees to reduce its 2020 emissions by 25 percent from 1990 levels (the degree necessary to approach levels deemed safe by leading scientists), it might have to buy up to 4 metric gigatons of offsets from the developing world—a thirty- to fortyfold increase over current levels.

Carbon markets, today and tomorrow

To be sure, carbon markets have suffered growing pains. In the first phase of the EU ETS, too many allowances were issued. And more recently, the economic slowdown has caused emitters to reduce their production forecasts. In both cases, the effect has been to create an excess of supply, causing prices to fall sharply. As a result, some banks, faced with lower volumes and prices, have recently shut or scaled back their trading operations.

Notwithstanding these problems, we find the underlying opportunity compelling; a market potentially worth $2 trillion commands attention. Moreover, future cap-and-trade schemes, such as the one proposed for the United States, can reasonably be expected not to suffer from the same problems that have dogged the EU ETS. With better market mechanisms, growth in carbon trading is likely to accelerate quickly.

To prosper, banks must determine the right time to commit to carbon trading and offset sourcing in order to build share in what is changing from a market of one-off, over-the-counter deals into a global flow business comparable to other large commodity markets such as oil. This industrialization process will entail the development of universal standards for market transparency, product specifications, and contract terms; the provision of liquidity; and the development of regulation encouraging blue-chip market participants to trade in size.

Exchanges are already moving quickly to help build this new market. Many of the big exchange groups, such as NYSE Euronext through its Bluenext subsidiary and Nasdaq OMX through its NordPool operation, have launched spot and futures contracts. Volumes are growing smartly, and some exchanges are already turning profits. New brokerages are springing up to help create markets in EU emissions allowances, UN-backed certified emission reductions, and Regional Greenhouse Gas Initiative allowances in the United States.

In short, there is a lot of activity—but we would note that these are early days, analogous to the period from 1980 to 1984 when oil futures first started trading. Considerable opportunities will emerge in coming years, and banks that prepare and act early will have the chance to stake out a leadership position for the time when the market recovers and then takes off.

Financing and investing in the low-carbon economy

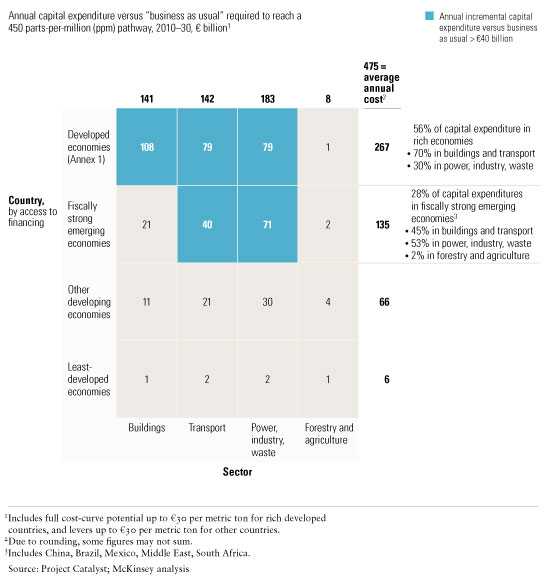

Economists expect that by 2020, governments and companies will spend about $16 trillion annually on investment in big capital projects—buildings, infrastructure, power plants, and so on. By 2030, that figure will rise to more than $24 trillion. Consider this the “business as usual” investment, to which must be added the incremental cost of addressing climate change as spending shifts from high-carbon projects to low-carbon ones. Recent McKinsey research indicates that to get on a pathway to lower emissions—pathways such as the one defined by the Intergovernmental Panel on Climate Change as likely to limit further atmospheric warming to less than 2 degrees Celsius—additional investments will be needed of about €475 billion annually: €350 billion per year for 2010–20, and €595 billion per year for 2021–30 (Exhibit 3).

A costly endeavor

Banks should note that this incremental investment may prove to be the tail that wags the dog. Imagine a new $200 million power plant. Leading-edge abatement technology may require only a relatively paltry $20 million additional outlay. But an understanding of that equipment, the technologies that compete with it, the regulations that govern it, and the carbon markets in which emissions credits are traded will be essential capabilities for the bank that wants to finance the plant. Low-carbon expertise may well become the sine qua non for winning “vanilla” business. And with access both to their own balance sheets and to the capital pools of the global financial community, banks have an unparalleled opportunity to profitably connect investors with the companies and projects critical to the establishment of a low-carbon economy.

Goldman Sachs, for example, generated an internal rate of return of 40 percent to 50 percent on its investment in Horizon Wind, a small player that it built into an industry leader. The IPO of Iberdrola Renovables for $24 billion in late 2007 was another noteworthy success. Clearly the drop in oil prices has taken the momentum (some might even say “froth”) from many solar and wind investments. And though no one can say with certainty where oil is headed next, we believe that the dramatic run-up in prices for the entire petroleum complex that we saw from 2004 to 2008 provided a sort of dry run for the low-carbon economy, showing how demand for renewable energy is likely to evolve. In any case, we expect short-term demand for solar, wind, and other low-carbon sources of energy to be driven mainly by regulation rather than by the price of oil.

Creating carbon “transparency”

The shift to a low-carbon economy will favor some businesses and potentially harm others, at least in the short term. Consider the effects on power-intensive sectors such as aluminum, steel, and cement. Management of energy supplies and risks is already a competitive differentiator in these industries, and in coming years, that phenomenon will only become more pronounced. Although many are relieved that oil prices have recently dropped below $50 per barrel, plenty of forecasters agree that because of deep-seated structural trends, prices might easily rise again above $100 per barrel within the next few years, as reflected by Deutsche Bank’s oil economist, who commented in January 2009 that “we do not believe that unusually low oil prices can last forever.”3 Moreover, energy security remains a major concern, as seen this winter in the dispute over gas between Russia and Ukraine.

Adding carbon prices into this volatile mix raises the stakes even higher. Should the price of carbon allowances rise to €55 per metric ton, for example, primary aluminum production costs would go up by 11 percent.4 To take another example, extending EU ETS to include the aviation sector (as is currently being discussed) could cost that already-under-pressure industry $1.3 billion.

At present, continuing uncertainty about regulation and a timeline that extends well beyond the three- to five-year time frame of most analysts’ models means that the long-term effects on corporate valuations are largely ignored by the markets.5 That could soon change, as post-crisis regulation may well push banks to develop a more comprehensive understanding of their risks. An example is the US insurance industry where, under new requirements agreed upon by the National Association of Insurance Commissioners (NAIC), insurers with annual premiums of more than $500 million will have to inform regulators of their exposure to climate change risks and detail their plans for addressing these risks.

Whether pushed by regulation or not, banks that can successfully develop a perspective on climate change and then incorporate this understanding into their valuation models (by assigning lower valuations or ratings to carbon-intensive companies to reflect their higher input costs or capital-expenditure requirements) or lending decisions (by imposing a higher cost of borrowing on companies with greater levels of regulatory risk) will potentially have a competitive advantage that will enable them to outperform the market and protect their—and their clients’—positions.

Driving innovation

Climate change is triggering a burst of entrepreneurial activity and innovation in the financial sector. Many banks, for example, are putting teams on the ground in developing countries to source and finance projects in the hope of producing a stream of cheap carbon credits. Insurers too are helping clients—for example, with climate-linked catastrophe bonds and innovative insurance products such as the Carbon Capture and Sequestration Liability Insurance, recently launched by Zurich, which will cover liabilities from pollution events and business interruption relating to the transmission and storage of carbon. And in commercial real estate, some are going a step further by developing complex financial instruments that make it financially compelling for landlords and tenants to coordinate and finance energy-efficient retrofits with payback periods extending beyond current tenancy agreements.

As markets develop and new needs emerge, banks with an active and healthy innovation process and the ability to harness their employees’ skills will be well placed to develop new ideas on which businesses can be built.

Developing a climate change strategy

Some features of the low-carbon economy—such as the long lead times associated with some of the opportunity areas and the small size of many of the companies currently active in them—do not typically marry well with banks’ operating and coverage models. This makes it essential for banks to have a distinct and clearly articulated strategy to develop market share in these businesses as they develop, supported by appropriate incentive and organizational structures. Moreover, the complexity of the climate change opportunity, and the dynamic nature of its political and regulatory environment, argues for a central pool of expertise that can advise and support the rest of the bank, as demonstrated by HSBC’s Climate Change Centre of Excellence, for example.

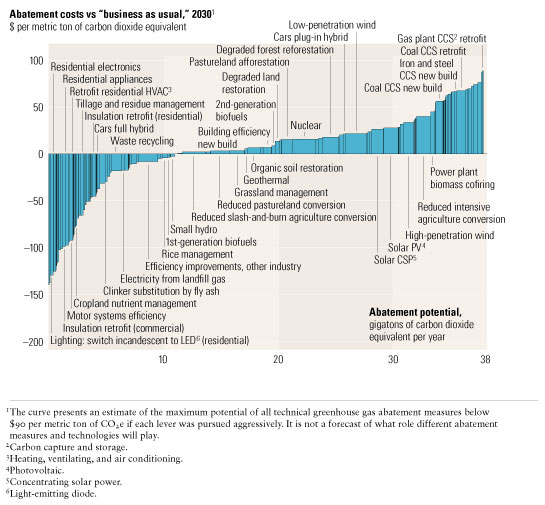

How should banks begin? A first step is to narrow the scope of their work. Thus far, we have discussed the opportunities of the low-carbon economy in general terms. But “low carbon” encompasses an enormous range of markets and technologies. McKinsey has developed an abatement cost curve that incorporates more than 200 technologies in detail across 21 regions of the world, ten major industry sectors, and four different time frames (Exhibit 4).

Global carbon abatement cost curve

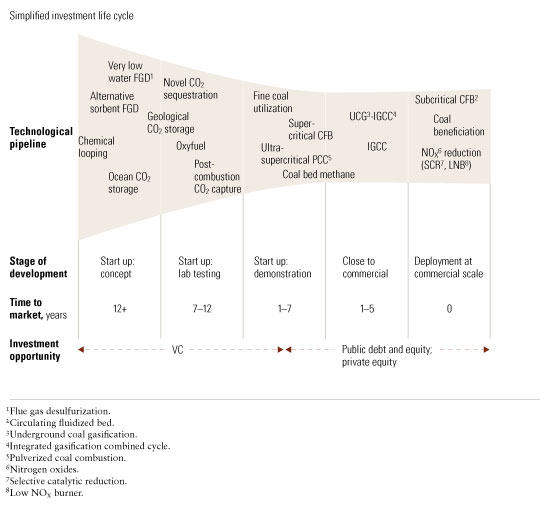

To take one example: clean coal comprises at least 17 different technologies, at varying stages of development and with different financing needs (Exhibit 5). These technologies also come under different subsidy and tax regimes, depending on location. A narrow scope is essential if the bank is to avoid scattering its energies and spreading itself too thin, especially in today’s resource-constrained context.

Clean coal: An in-depth look

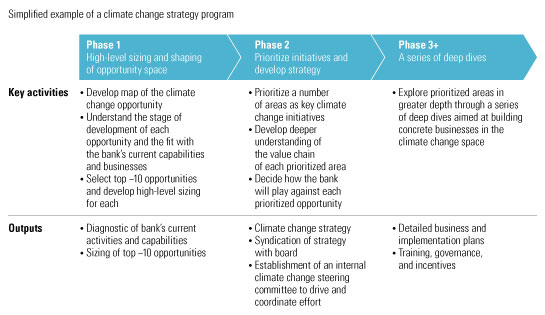

To narrow its scope, a bank needs to create a short list of opportunity areas, prioritized by the size of potential revenues and the time to market. At the same time, a systematic screening of the bank’s current climate change–related activities, across divisions and regions, could well reveal a previously obscure, largely uncoordinated, but nonetheless significant level of activity and revenues that could form the nucleus of a coherent strategy (Exhibit 6).

Developing a climate change strategy

This list should then be prioritized further, identifying those few areas in which the bank believes it can build deep and distinctive expertise and therefore meaningful market share. The bank should then proceed to a more detailed assessment of the specific products, industries, countries, and customers that it will focus on in each area, and the formulation of its key criteria for success in each.

Whether the chosen areas represent a source of immediate opportunity or a longer-term prospect, the final step is for the bank to understand in detail how it should implement the recommendations and what the targets and milestones should be. This step must include thoughts on how to address the opportunities in an integrated manner, capitalizing on the knowledge and insight gained in one part of the bank to win business in another—not an insignificant challenge given banks’ perennial problem of coordinating client service across their businesses. Deutsche Bank is a leading example of how to manage this: it formed an environmental steering committee that brings together the key stakeholders from across the bank, along with an external advisory board that allows it to tap into and validate its progress with leading climate change experts and leaders.

As important as agreeing on where and how to play is deciding on the pace of action. Although the timing of many opportunities is sooner than most people think, the challenge, as in any emerging market, will be for management to agree on how revenues are likely to evolve, the likely competitive response, and the implications for the sequencing of activities and investments of people and time. History has shown that banks that invested early to build a leading position in nascent markets—as Morgan Stanley and Goldman Sachs did in energy trading in the mid-1980s and Société Générale did in equity derivatives in the late 1980s and early 1990s—have reaped enormous benefits as these markets have grown. At a minimum, we suggest that banks take stock of their current climate change–related activities and form a view of how the market is likely to develop. Even if a bank decides to wait before becoming involved, an understanding of the steps it is currently taking, the potential upside, the issues and capabilities needed to succeed, and a commitment to monitor developments will ensure that, when it believes the time is right, it will be ready to act.