Most bankers would agree that the financial crisis has highlighted major shortcomings in the regulatory framework governing minimum bank capital and liquidity. New standards for regulatory capital and liquidity,1 now under discussion at the Basel Committee on Banking Supervision, will likely establish the rules for European banks at least over the next decade and set the tone for local regulation in other parts of the world. Not surprisingly, bankers have dubbed the new rules “Basel III.”

Basel III could significantly change the composition of banks’ Tier 1 capital; risk weights, especially in trading books; and capital ratios. New McKinsey research estimates that the effect of these new rules on Europe’s banks would be a capital shortfall of about €700 billion. This sum would represent a 40 percent increase in the European banking system’s core Tier 1 capital.

What’s more, Basel III’s proposed new standards for liquidity and funding management would constrain funding severely. We estimate that European banks may be required to hold an additional €2 trillion in highly liquid assets and to raise €3.5 trillion to €5.5 trillion in additional long-term funds. At present, European banks have only about €10 trillion in long-term unsecured debt outstanding.

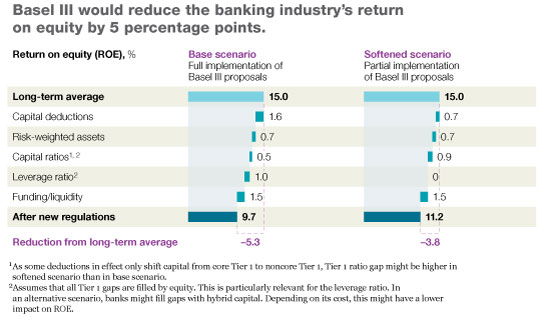

In the absence of any mitigating action, the new costs for additional capital and funding could lower the industry’s return on equity (ROE) in 2012 by five percentage points, or one-third of the industry’s long-term-average 15 percent ROE (exhibit). Basel III may also have some unintended consequences, such as impairing the interbank-lending market and reducing lending capacity.

It is likely that the final Basel III rules will be softened in several areas. Nonetheless, an examination of the range of proposals indicates that the final accord’s impact on banks will be substantial across a range of activities.

Download the full report, Basel III: What the draft proposals might mean for European banking, at the McKinsey & Company Web site.