Russia’s economy, like the world economy as a whole, fell off a cliff during the first half of 2009, with GDP down roughly 10 percent.1 It’s a movie the country has seen before: GDP fell more than 40 percent following the Soviet Union’s collapse, in 1991, and in 1998 Russia defaulted on its debt, the ruble plummeted, and economy-wide capacity utilization fell below 50 percent.

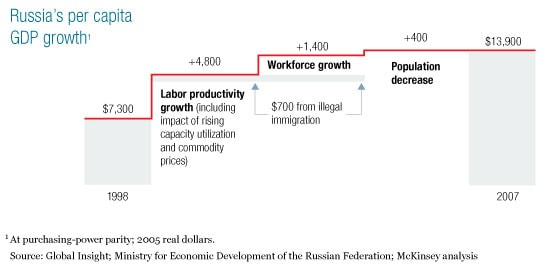

Last time around, Russia experienced a dramatic economic turnaround: GDP grew at an average annual rate of 7 percent between 1998 and 2007, vaulting the country to 53rd (from 72nd) in the world rankings of wealth. Wages increased strongly as well, with disposable income rising 26 percent a year in nominal terms.

Pulling off a similar rebound will be more challenging now. Even before the global downturn, capacity utilization was approaching 80 percent, and the days of relatively easy expansion through better use of the existing capital stock were drawing to a close. An increase in the size of Russia’s workforce, which accounted for almost one-third of the growth in real per capita GDP over the past decade (Exhibit 1),2 was going into reverse. In fact, Russia’s labor force could shrink by as many as ten million people by 2020. The financial crisis has made raising capital for investments more difficult and has battered commodity prices—including those of oil, metal ores, and coal. Commodities collectively represented around 20 percent of Russia’s GDP in recent years. Now Russia must grow by making better use of labor and capital resources—in short, higher productivity. The McKinsey Global Institute (MGI) has twice studied Russian labor productivity: first in 1999 and now in 2009.3 During the intervening years, economy-wide labor productivity increased to 31 percent of US levels, from 22 percent.

On the fast track

To make another leap in productivity and economic performance, Russia must tackle deep structural challenges, such as boosting its competitive intensity, making nuts-and-bolts improvements in operations and business processes, simplifying and clarifying regulations (including those for urban planning and permissions), and allocating financial capital more efficiently. There’s also a human dimension: raising productivity will require a more skilled and mobile workforce.

But Russia has some advantages. It can grow robustly without the need for rapid urbanization and social transformation—needs that are so acute in other emerging markets, notably China and India, countries whose productivity lags behind Russia’s significantly. And there’s a silver lining to Russia’s massive investment requirements: as demand for capital outstrips domestic supply, competition for foreign funds will probably make it necessary to speed up the implementation of Russia’s productivity agenda. Finally, the country’s government, which must play a critical role, has a powerful incentive to move quickly. In recent years, oil-related taxes represented a third to half of federal revenues. If these receipts shrink, Russia will need new ones. Broad-based, productivity-led growth, while far from easy to realize, is an achievable way to create new revenue sources while improving the lives of Russia’s people.

Coming up short

A sector-based view

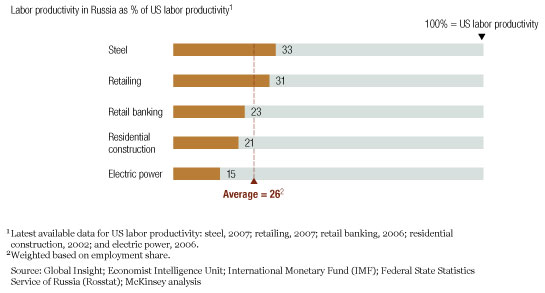

Our research is grounded in an analysis of five important sectors: electric power, retailing, steel, residential construction, and retail banking. Their labor productivity now ranges from 15 percent of US levels, in electric power, to 33 percent, in steel (Exhibit 2).

Three shortcomings are common to all of these sectors: inefficient business processes, obsolete capacity and production methods, and structural problems attributable to economy-wide factors, such as income levels that are lower than those prevailing in advanced economies. Depending on the sector, inefficient processes account for 30 to 80 percent of the labor productivity gap with the United States, outdated capacity for 20 to 60 percent, and structural factors for 5 to 15 percent. (For a view of the barriers to productivity from the general director of a Russian potassium fertilizer producer, see the sidebar “Inside perspective: Analyzing the bottlenecks.”)

The underlying causes of these shortcomings are diverse. Differing levels of competition within sectors clearly play a role: retailing and steel are the most productive and competitive of the five sectors we studied, while electric power and construction are among the least on both fronts. Regulatory procedures and processes may obstruct operational improvements. Complex, opaque rules for planning and permissions make development projects riskier, and the absence of a comprehensive financial infrastructure hampers the efficient raising and allocation of capital. These challenges cut across each sector we studied, but to make them—and the potential solutions—more tangible, we address them in the context of individual economic sectors.

The competition problem in electric power

Russia’s electric-power sector, a monopoly until 2008, is a poster child for the inefficiencies arising in the absence of vigorous competition. Although the sector is the world’s fourth largest, its labor productivity is just 15 percent of the US level. The end, last year, of the electric-power monopoly could stimulate productivity growth, but only if real market-based price competition emerges. (For a view of the electric-power sector from leaders of an established Russian player and a new entrant from Italy, see the sidebar “Inside perspective: Change and transformation.”)

The industry’s central challenge is that Russia must replace much of its aging capacity, but electricity prices don’t cover the full cost of investments in new plants. Without price liberalization, private power companies have little reason to invest in new generating capacity—and the government has historically favored low prices as a social good.

One way the government could help make plants cheaper to build (and perhaps limit the price increases needed to pay for them) would be to relax complex equipment-licensing procedures. These rules—combined with the sector’s suboptimal procurement practices, opaque cost controls, and lack of standardization—make building new capacity pricier than it is in other countries. Coal-fired plants, for example, are 25 to 40 percent more expensive than similar facilities in Europe and the United States.

The sector itself can do much to boost the efficiency of existing operations. Russia’s coal-fired plants are 8 percent less fuel efficient than European ones, and its gas-powered plants are 6 percent less fuel efficient. The low density and long distances of Russia’s high-voltage transmission lines raise technical “leakages” to almost twice the US level. Commercial transmission losses are four times higher because of electricity “theft”—the nonpayment of bills and inaccurate metering. Tackling these problems will make a difference. Nonetheless, productivity won’t leap ahead until competitive pricing gives the sector financial incentives to replace obsolete generating capacity and to reduce operating costs in existing plants.

The road to operational excellence in retailing and steel

Competition isn’t the problem for Russia’s retailing and steel sectors: both have no government-owned enterprises, and retailers face foreign rivals at home, while the steelmakers contend with global competitors in Russia’s export markets. But although these are the most productive sectors we studied, both still have huge opportunities—for the steelmakers, shutting down antiquated technology; for the retailers, replacing dated store formats and improving business processes.

Such opportunities exist, in part because of complicated, time-consuming regulatory procedures and processes. These slow down not only the development of commercial real estate (and therefore the modernization of retail formats) but also the consolidation of the steel sector and the adoption of lean business processes. (For executive views on business process improvements in another metal industry, aluminum, see the sidebar “Inside perspective: Too many signatures.”)

Retailing. Over the past decade, Russian retailing (which, with the wholesale sector, accounts for 10 percent of GDP) has increased its turnover sixfold, created five million new jobs, and doubled its productivity from 15 percent of the US level to 31 percent today—the best performance of the five sectors we analyzed. The heart of this transformation was the rise of modern retail formats, which are three times as productive as traditional ones.

Despite this progress, modern formats account for just 11 percent of retail employment and 35 percent of sales in Russia, compared with 82 and 86 percent of retail turnover in France and Germany, respectively. To double the retailing sector’s productivity, Russia must increase the share of modern formats dramatically. In fact, the country should also boost their productivity, which lags behind that of their counterparts elsewhere. Russia’s modern outlets, for instance, employ nearly three times as many people per square meter of retail space as their US counterparts do, and their workforce isn’t well organized; staffing levels, for example, are often out of synch with customer traffic. But the throngs of customers who fill Russia’s modern-format stores help compensate for their higher operating costs: revenues per square meter are roughly two times those in the United States.

Overall, the low share of modern formats in Russian retailing accounts for three-quarters of the productivity gap with the United States; the rest is due to inefficient processes. The country’s network of roads is congested and underdeveloped, lengthening delivery times and increasing transport costs. The domination of logistics networks by small regional providers means that supply chains tend to be fragmented and therefore unreliable. Russian stores also don’t exploit IT sufficiently and use part-time labor much less than their counterparts in other markets do, so they are overstaffed during low-traffic periods and understaffed during peak ones.

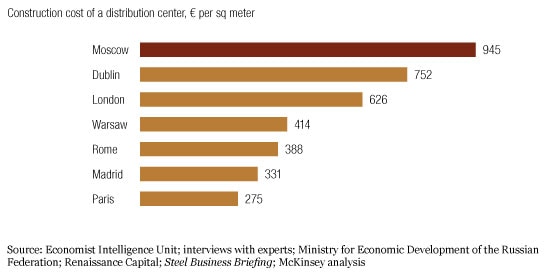

Upgrading these operating practices represents an enormous opportunity for Russian retailers, which should start now to centralize their administrative functions, optimize staffing, and improve processes. The current economic squeeze also gives retailers an opportunity to acquire new sites at lower prices and to consolidate smaller and poorly performing players. The government can help by streamlining regulations in order to accelerate the construction of new commercial real-estate projects, which are often dramatically more expensive than they are in developed countries (Exhibit 3), and by improving the transport and utility infrastructure.

Overpriced

Steel. Russia has traditionally had a strong, globally competitive steel industry, which accounts for 3 percent of the country’s GDP and 6 percent of its exports and employs more than a million people. The industry’s productivity has risen sharply since 1997, but almost entirely on the back of higher capacity utilization, not improved efficiency.

Outdated, subscale steelmaking technology is a major cause of the industry’s low productivity in Russia: it still produces 16 percent of its steel in open-hearth rather than basic oxygen furnaces, which are 50 percent more labor efficient. The other reason for the low productivity is inefficient business processes. Russian steelmakers employ 60 to 100 percent more administrative workers than best-practice companies do.

Higher productivity is achievable—already, the top three plants in Russia operate at 77 percent of US levels, more than three times the productivity of the country’s smaller, older plants. Significant opportunities remain to boost the industry’s productivity through automation, IT investments, and improved work organization. The government can lend support by emulating the European Union’s approach to rationalizing its steel industry: job creation, retraining, and outsourcing and subcontracting programs.

The planning and permissions imperatives in residential construction

A lack of effective planning increases the uncertainty and risks of development projects in every sector we studied. But its impact is particularly pronounced in residential construction, which accounts for 6 percent of Russia’s GDP and 8 percent of official employment. Just before the crisis, Russia’s government committed itself to increasing per capita housing space to 33 square meters, from 21, by 2020, in line with EU levels. This standard would require average yearly residential construction at more than twice its historic peak. Improving the sector’s productivity—now 21 percent of the US level—is vital to spur the supply of new housing.

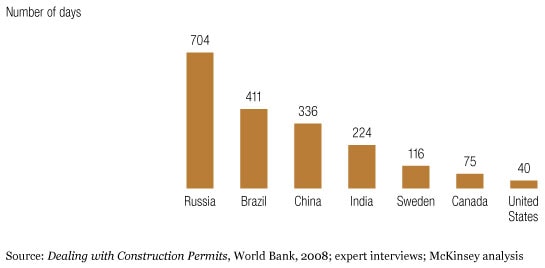

It takes, on average, 700 days to get a construction permit in Russia—significantly longer than in Brazil, China, and India, and six times longer than in Sweden (Exhibit 4). Extended project cycles make planning less effective and create supply chain and financing problems; bank financing is virtually unobtainable for small and medium-sized developers. The risk and uncertainty for both them and investors is all the greater because two-thirds of Russia’s cities haven’t approved the master plans required by the country’s city building codes. Developing and ensuring the effective implementation of such plans for cities and regions, along with creating a unified database of land plots, would make construction more productive by minimizing the time required to obtain permits and approvals. When Russia took such steps for construction projects related to the 2014 Winter Olympics in Sochi, approval times fell to six months, from three years.

On hold

Regulatory issues aren’t the only problems bedeviling Russian residential construction. The industry, for example, should increase its use of productive modern materials and build larger housing developments. Only 17 percent of Russia’s new houses, compared with 70 to 80 percent of US ones, take advantage of high-productivity prefabricated wall materials (including concrete and wooden panels) and metal frames. Similarly, traditional homes built, with relatively unproductive methods, by their future occupants account for three-quarters of Russia’s single-family housing output. (For the views of executives on the high cost of construction in Russia, see the sidebar “Inside perspective: Thicker pipes and walls.”)

Retail banking and Russia’s financial system

The restructuring and resource reallocation needed throughout Russia’s economy will be possible only with a comprehensive financial infrastructure. To create one, the country needs credible rating agencies, better-developed financial instruments, and a bigger pool of long-term savings, as well as a banking sector that can pool domestic capital resources effectively and allocate them efficiently. Before the crisis, Russia had the world’s fastest-growing retail-banking market, with risk-adjusted revenues expanding at a compound annual rate of 60 percent from 2000 to 2007.

Yet most of Russia’s 1,000-plus banks lack the financial or physical scale to operate efficiently. The government could foster consolidation effectively by gradually tightening capital and reporting requirements and risk-management standards—moves now being implemented with much caution. Restructuring of this sort would also increase productivity, now 23 percent of US levels after adjusting for differences in incomes and ten times lower when measured by physical transactions per employee.

Besides promoting such a restructuring, the government can also encourage higher productivity by curbing its regulation of the banks’ branch-based transactions and cutting the bureaucracy involved in basic transaction processing. Meanwhile, the industry should centralize back-office and administrative functions and work with utilities to expand the use of electronic bill payments and transfers.

Just consider a few facts. Russian banks must fill in large numbers of forms. One directive requires the regular submission of some 74 different reports to the central bank, compared with 1 report US banks submit every 15 days to the Federal Reserve System. Russian bank branches require up to three people, compared with one in the United States, to execute a single cash withdrawal. As a result, making a withdrawal, a deposit, or a payment from an account takes between two and five times as long as it does at US banks. Only about one-third of payment transactions in Russia are automated, compared with 70 percent in the United States and 90 percent in the Netherlands. Nonautomated transactions are on average 12 times more labor intensive than electronic ones.

Most banks haven’t begun to centralize their back-office and administrative functions. To double the sector’s productivity, the number of electronic payments must increase by 150 percent, and half of all payments will have to be undertaken outside bank branches. The experience of some local banks that have implemented productivity efforts suggests that these targets are quite achievable, with minimal capital investment.

The human dimension

Labor productivity improves only when work changes—because people undertake their current jobs more efficiently or move to other, more productive roles. To realize both possibilities, Russia must improve the way it educates and trains professionals and make it easier for workers to move around the economy and the country.

Labor skills

Despite high literacy rates and excellent technical education, Russia lacks key skills. By far the largest gaps, evident in all five sectors we studied, are in project management, largely as a result of 20 years of underinvestment and the resulting inexperience of managing large capital projects.

The electric-power sector also doesn’t have enough people with plant design and construction know-how, and it is difficult to fill these gaps on a short-term basis by engaging engineers who have experience in construction contracting, since there are so few of them and the market is only emerging. In steel, even recent graduates tend to lack the project-management, teamwork, leadership, and foreign-language skills needed to oversee technological-modernization projects.

Upgrading outdated educational programs will help address this shortfall. Many design-management students in residential construction, for instance, still use equipment dating back to the 1950s. Topics such as designing to cost are often covered by antiquated curriculums. Adjusting them to global best-practice standards, as well as increasing the practical component in relevant courses, would raise skill levels throughout the economy.

Labor mobility

Russia can achieve its potential only if it promotes labor mobility among geographic regions and industry sectors. Historically, rapid per capita GDP growth has almost invariably been accompanied by such a shift in employment—first, from agriculture to manufacturing and, more recently, from manufacturing to financial, business, and trade services. In Russia, however, housing, infrastructure, legal, and cultural barriers hinder labor mobility.

Russia’s federal and local governments, as well as its businesses, can facilitate the reallocation of labor by focusing on regional economic-development initiatives that create new jobs. Enhanced job-placement services and improved social programs will also help the country’s workers become more mobile.

The restructuring of Europe’s steel and automotive industries during the past two decades provides some guidance. From 1986 to 1996, 12 EU countries decreased employment in the steel sector by 200,000 people, a number roughly equivalent to the sector’s excess employment in Russia. Likewise, during the 1990s a shift in automotive production to lower-cost countries led Volkswagen to shed 20 percent of the employees at its headquarters, in Wolfsburg, Germany. Virtually overnight, unemployment there soared to 18 percent. Five years later, thanks to a joint venture between the company and the municipal government, more than 11,000 new jobs had been created and the city’s unemployment rate was 50 percent lower.

Russia’s economy has made enormous strides over the past decade, but the forces behind its recent growth are weakening. By boosting productivity in the years ahead, the country can make its economy more competitive and improve the lives of its people.