The global economy’s future will be powered by leading-edge semiconductors. As geopolitical tensions rise, countries and companies are moving to diversify production beyond Taiwan and South Korea and bring manufacturing closer to home. In this context, foreign direct investment (FDI) is emerging as a key driver of global capacity growth. In fact, FDI could bolster the United States’ capacity, potentially making it the second-largest producer of leading-edge semiconductors by the early 2030s, Senior Partner Olivia White and colleagues note. However, the reliance on global supply chains for raw materials and manufacturing equipment remains a critical factor in the industry’s future stability.

Image description:

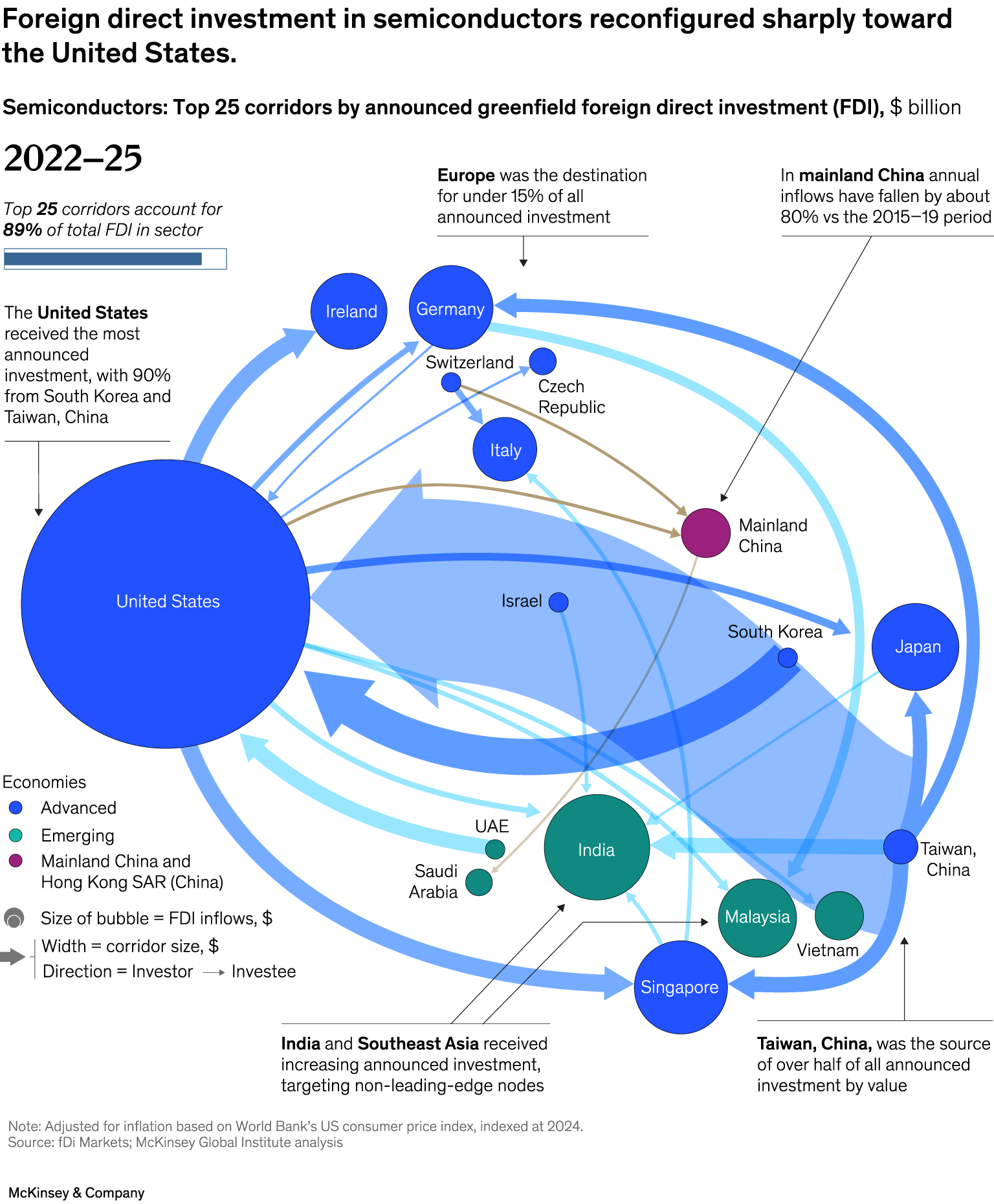

A pair of flow diagrams illustrates the top 25 corridors by announced greenfield foreign direct investment (FDI) for the semiconductor sector during two time periods: 2015–19 and 2022–25. The diagrams show the direction of investment between countries, with the size of the bubbles representing FDI inflows and the width of the arrows indicating corridor size. In 2015-19, the top 25 corridors accounted for 86 percent of total FDI in the sector. Mainland China was the largest recipient of FDI. In contrast, the 2022–25 diagram shows a significant shift, with the United States becoming the largest recipient, driven primarily by investments from South Korea and Taiwan (China), which accounted for 90% of the total. The top 25 corridors accounted for 89% of total FDI. The diagrams also highlight a decline in Mainland China's annual FDI inflows by about 80%, compared to the 2015–19 period.

Note: This image description was completed with the assistance of Writer, a gen AI tool.

Source: Using data provided by fDi Markets; McKinsey Global Institute analysis.

End of image description.

To read the report, see “The FDI shake-up: How foreign direct investment today may shape industry and trade tomorrow,” September 22, 2025.