Romanian citizens’ net wealth has increased over the past two decades, but citizens have low levels of savings and few financial assets—suggesting that financial education, and long-term planning and resilience have not progressed equally fast. A significant part of the recently accumulated wealth is in real estate, as Romanians have a clear historical preference for owning their houses or apartments. Despite the increase in overall wealth, Romanians have far fewer financial assets than their fellow Central and Western Europeans and the country has one of the lowest savings rates in the region. When Romanians save, they tend to prefer low-risk, low-return options such as cash, current accounts, and deposits. In general, Romanians have little trust in both public and private pensions, and only around 3 percent of the population invest in voluntary financial assets such as pensions or mutual funds.

This article draws on the findings of a consumer survey conducted by McKinsey in Spring 2022 that shed light on Romanians’ attitudes toward money, saving, and financial planning that may explain these trends. The survey targeted the urban population, with varying levels of education, ranging from 18 to 65 years of age.

The survey supports global post-pandemic evidence that there is an increase in saving behavior, or at least an intention to save more. However, around 60 percent of Romanians surveyed say they fail to stick to their savings goals. This may be due to lack of funds. It could also be because they lack the necessary financial education, or access to reliable financial advice, to help them understand how to save or invest. This situation is particularly pronounced and challenging in the lower-income and lower-educated segments of the population.

Moving forward, Romanians could leverage the overall increase in wealth, and higher earnings levels, to build financial security in a way that may allow for greater individual and collective stability. On a national level, this could turn the country’s sustained growth into long-term prosperity. This will take a change in mindset and behavior. And such change may be difficult to achieve at scale on an individual level. There are opportunities for all stakeholders—including consumers, financial institutions, and the state—to work together to increase financial awareness and education. These solutions require collaboration, and concrete measures and actions, and will likely be successful only if built effectively around consumers’ needs and expectations.

Net wealth is increasing but financial wealth remains low

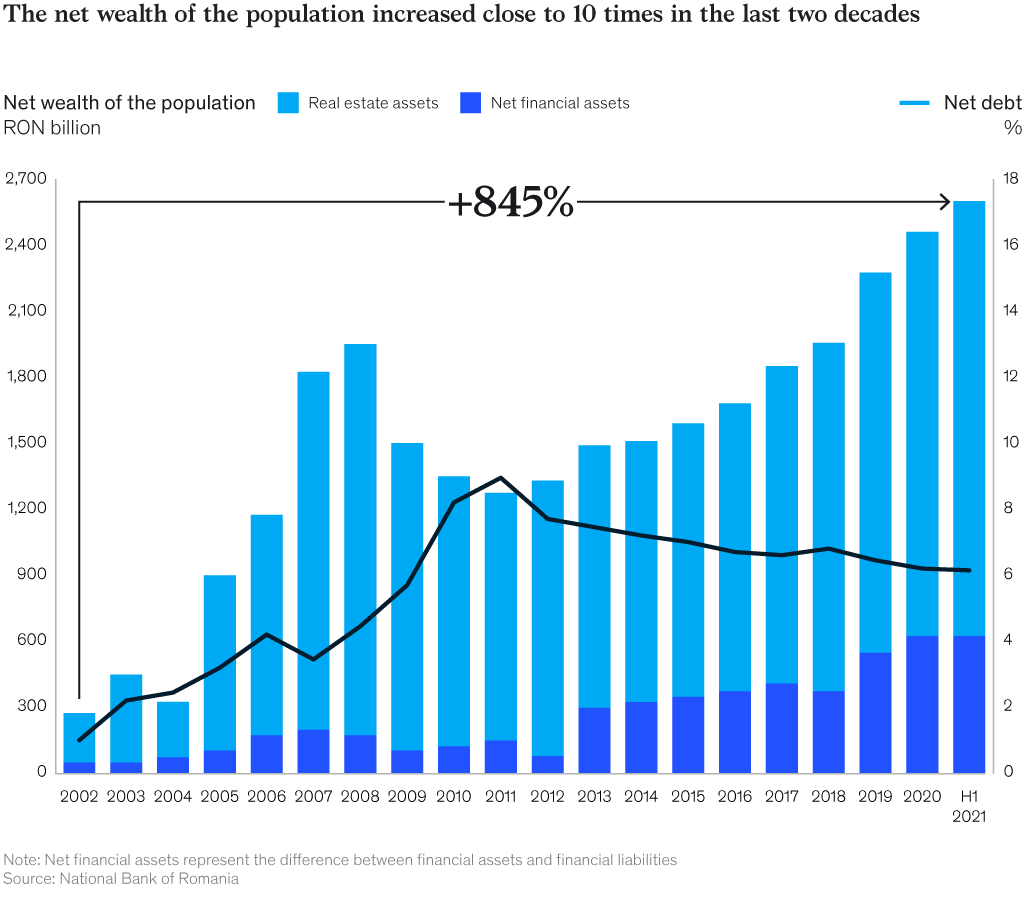

The Romanian economy has followed an upward trend and the net wealth of the Romanian population has increased more than eight times over the past two decades, according to the National Bank of Romania. Disposable income increased significantly between 2000 and 2020, as Romania had the highest annual growth in disposable income per capita in Europe in this period, at 10 percent. This allowed Romania to come close to the levels of disposable income per capita in more advanced Central European countries, closing the gap from 60 percent 20 years ago, to around 15 percent today. Many Romanians have invested their wealth in real estate; in fact, over 95 percent of Romanian adults own an apartment or a house, based on Eurostat data. Despite this economic growth and a culture of investment in real estate, Romanians’ net financial assets have not kept pace with the increase in overall wealth (Exhibit 1).

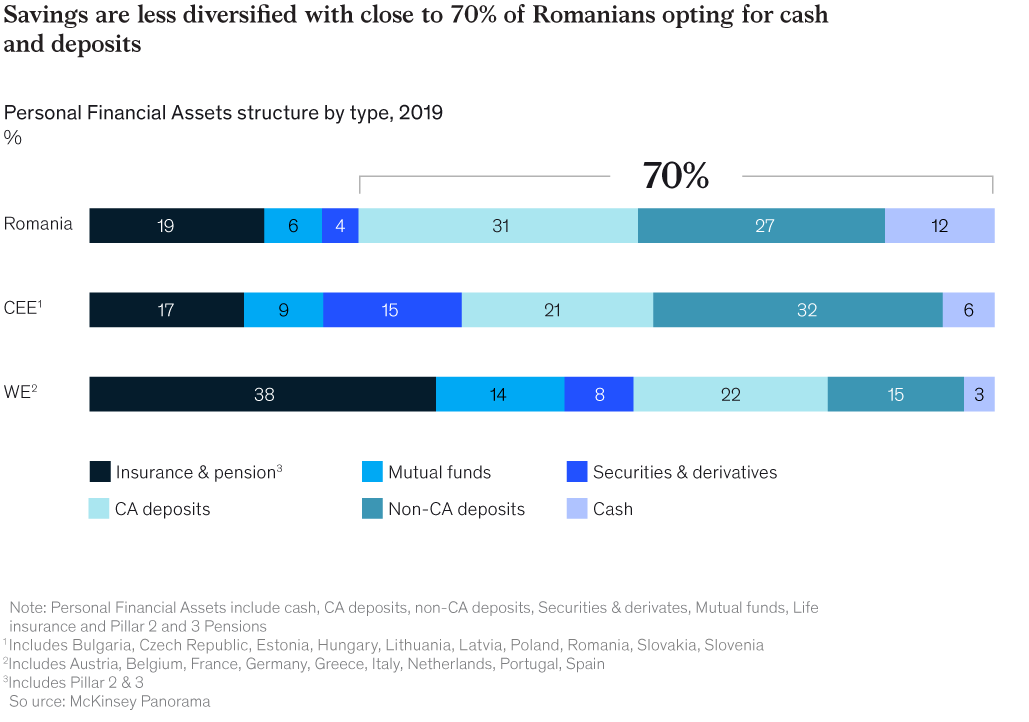

Between 2000 and 2020, Romania showed strong growth in disposable income per capita and got close to the values seen in Central and Western European countries, but citizens did not redirect the extra income into savings. Romania has one of the lowest levels of personal financial wealth compared to other Central and Western European countries, at 36 percent of GDP—which is roughly half the Central European average, according to McKinsey Panorama data.1 Financial wealth per capita is around $5,000. By comparison, Hungary’s financial wealth penetration rate is at 72 percent of GDP, with a per-capita financial wealth of $12,000.

When existing, Romanians’ savings are mostly in cash and deposits. Cash, money held in current accounts, and deposits make up 70 percent of personal financial assets, compared to 59 percent in Central Europe and 40 percent in Western Europe. Romanians tend to hold two to four times more cash when compared to regional peers and generally do not make use of sophisticated investment products such as mutual funds, securities and derivatives (Exhibit 2).

Only a very limited part of Romanian adult population have invested in a voluntary financial asset—around 3 percent in mutual funds, and less than 2 percent in pillar 3 pensions, based on National Bank of Romania data. The level of overall investments in insurance and pension products is close to that seen in Central Europe (just under 20 percent of personal financial assets) but is relatively low compared to Western European countries.

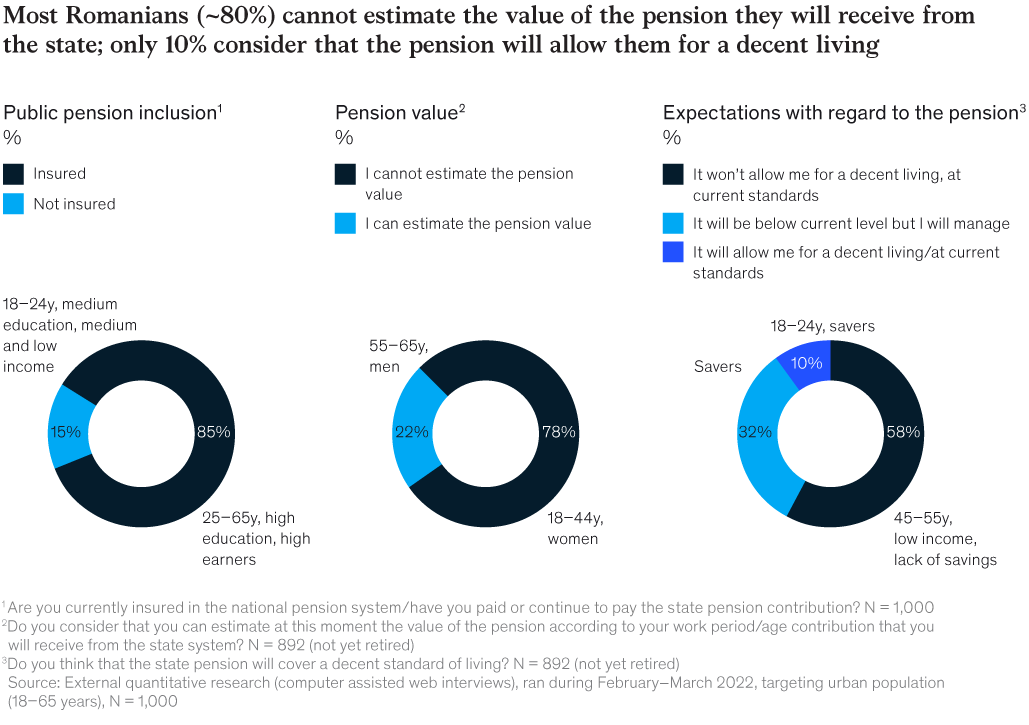

Furthermore, it seems that Romanians generally lack faith in both public and private pensions. The survey found that only one in five Romanians trust the public pension system and only one in four trust the privately-managed one. Additionally, 80 percent of respondents could not estimate the value of the pension they will receive from the state, and 90 percent expect that their pension will be insufficient for them to maintain their lifestyle post retirement (Exhibit 3). Lastly, only 28 percent of Romanians declared that they plan their retirement proactively.

Many Romanians plan to save or invest more, but lack the support to do so

The COVID-19 pandemic boosted savings rates across the world. This may have been due to a lack of spending options during pandemic-related restrictions in combination with heightened fears around financial instability. The pandemic increased awareness among consumers of the importance of saving; and savings increased globally, including in Romania. But this momentum is difficult to maintain as spending restrictions have eased and high inflation has started to dent purchasing power.

Despite the pandemic-related increase in savings, the survey indicated that only one in four Romanians said that they have managed to keep up with their pandemic-induced saving behaviors. This situation is driven by lack of funds or because they lack the financial education or support to help them save. For instance, only 15 percent of respondents said they had attended financial education programs, and just under 30 percent said that their families taught them how to invest.

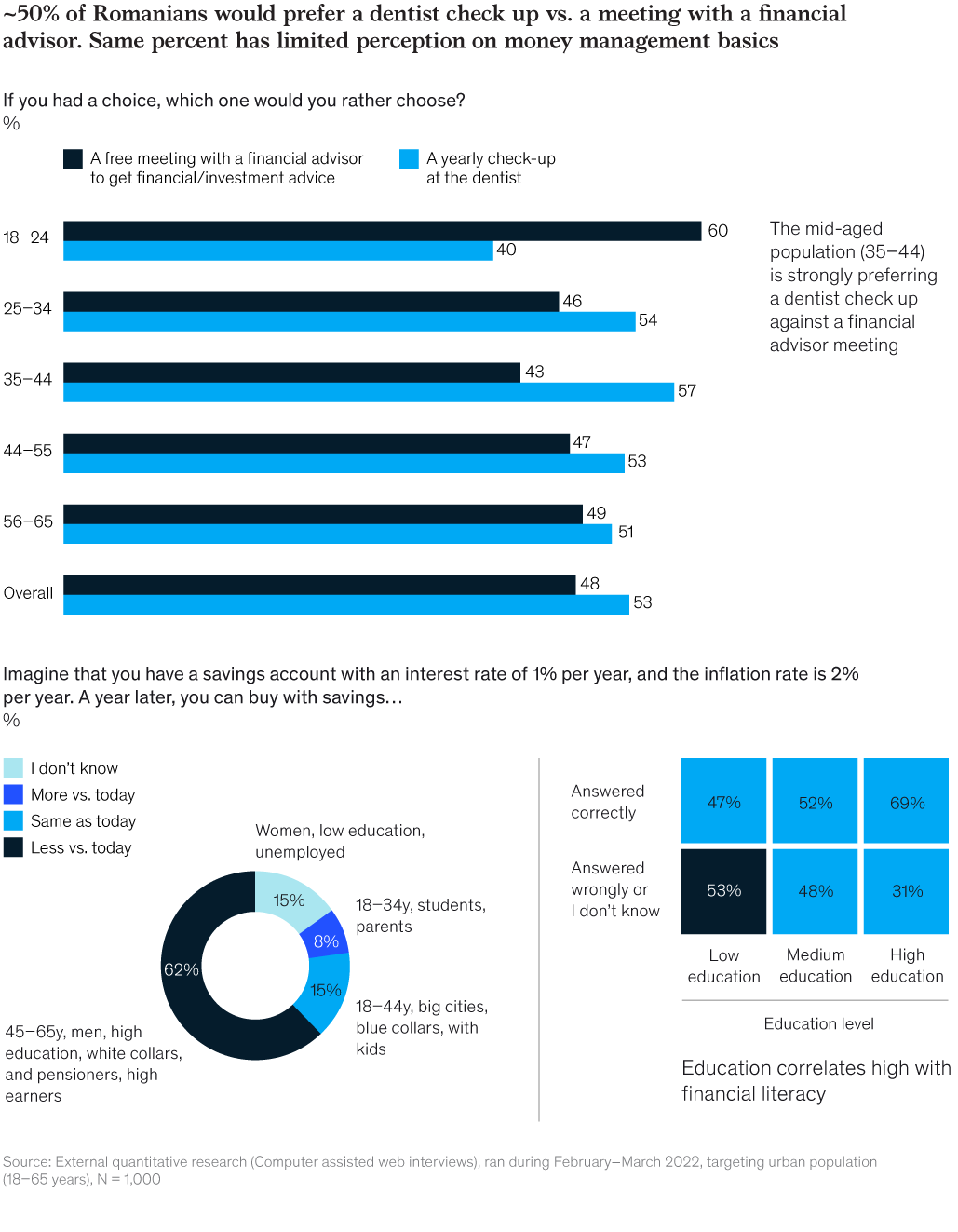

Romanians have long-held attitudes toward saving and financial planning that affect how they choose to save or invest. For instance, although many Romanians wish to save more, they are hesitant about financial planning. In fact, slightly over half of respondents said they would rather schedule a yearly check-up at a dentist than attend a free meeting with a financial advisor. Of course, dental check-ups are necessary, while saving is voluntary, but the sentiment is clear: Romanians are hesitant to seek financial advice even if it is free. A similar percentage had difficulty with fundamental money-management concepts such as understanding the effect that inflation would have on savings (Exhibit 4).

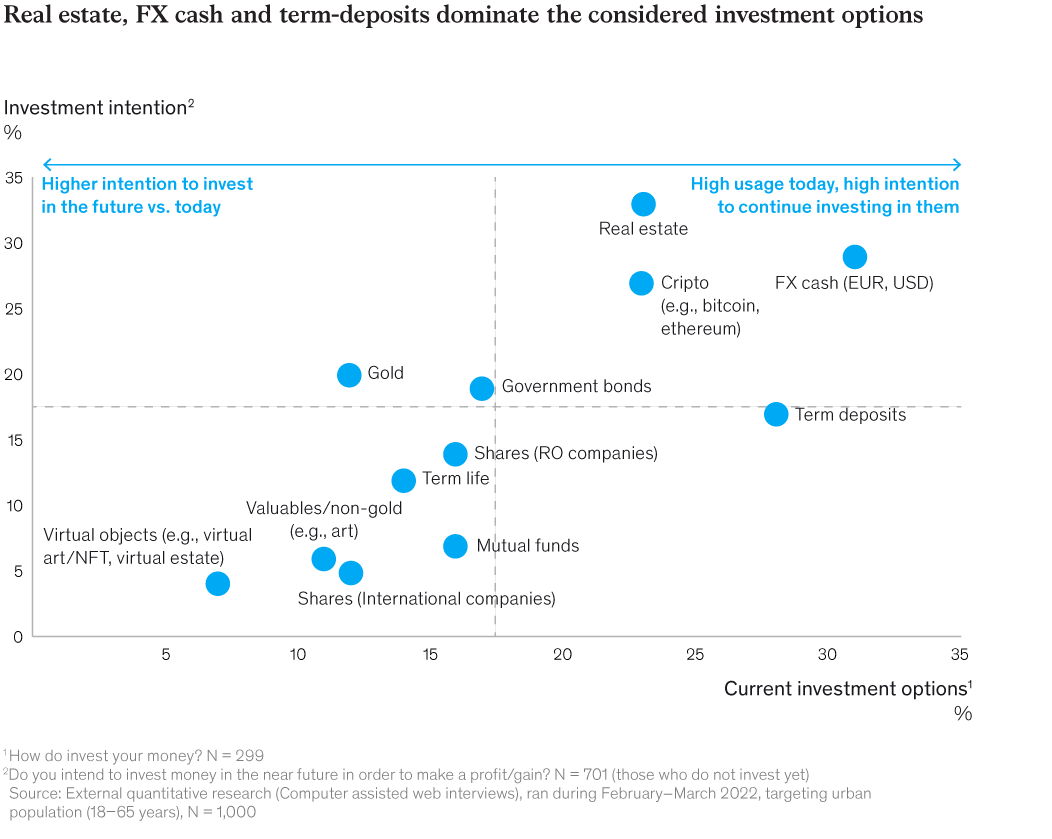

This lack of trust in financial advice, and low levels of financial education, also affect how Romanians choose to invest. The survey found that respondents are either risk averse and choose low-risk, low-return assets such as foreign currency and term deposits or opt for speculative investments such as cryptocurrencies (Exhibit 5).

Even though Romanians are making these investment decisions, the survey indicates that they are making them on their own. An individual’s personal circle of family and friends takes precedence as a credible source of information regarding money management over financial institutions or experts such as financial advisors—and 75 percent of respondents claim to manage their investments alone. Only 20 percent believe that banks offer reliable financial advice and only 18 percent check with their bank when making a money-related decision.

In addition to a risk-averse attitude, a lack of financial knowledge, and mistrust of institutions or individuals who could provide financial advice, many Romanians face other challenges that prevent them from saving or investing. The combination of low income and high debt is a significant challenge. This situation is particularly dire for low-income, low-education segments of the population. The survey shows that only 26 percent of the less educated segment manage to save at all, compared to the national average of 63 percent who manage to save occasionally or monthly. Those who indicate that they save every month, but not a fixed amount—32 percent—tend to live in mid-size cities and have higher education levels.

The younger segments of the population seem equally challenged to cope with financial investments. Even though 31 percent of the 18- to 24-year-old segment surveyed are still financially dependent, they plan to save or invest. But they too lack financial education and show even higher levels of risk adversity than average.

There is a strong consensus among respondents that the state should offer more support for the population to save more than they currently do, as 65 percent of respondents declared that the state should get more involved in helping the population to save or invest by offering incentives. As much as 60 percent felt that banks or insurers should also get more involved in helping the population to save by offering counselling and advice, and providing products that suit customers’ needs. Romanians also believe that families should play a larger role in providing financial education for their children and that the schooling system should also assist in this regard.

Opportunities to build wealth exist

Romanians could build on the recent momentum of increased savings, and they will need wider support, from a variety of stakeholders, to help them build and diversify their personal wealth. Change will be difficult to achieve at an individual level. There are opportunities for financial institutions, the state, and consumers to collaborate in finding ways to increase financial education, provide products or services that meet consumers’ needs, and ultimately build a culture of financial awareness to boost personal wealth, on top of existing efforts, while scaling those that proved efficient.

There are examples of initiatives and best practices in other parts of Europe that have provided accessible financial education. The following four examples highlight ways in which the barriers and challenges of financial inclusion can be overcome. In Belgium, educational websites targeted at potential investors offer easy-to-understand advice, such as tips for taking the first step toward investing in the stock market or key pointers for understanding pensions. There are also platforms for beginner investors that explain the basics of investing and provide an overview of potential investment options. Such platforms are made accessible as they are promoted through social media. Additionally, the Belgian education system plays a part in basic financial education as children from the first to the sixth grade receive financial training as part of their main curriculum.

Financial institutions have also found ways to help new clients begin to build their financial wealth. For example, one German asset management firm develops products specifically to help first-time investors convert their deposits into investment products and uses a defensive asset allocation strategy to minimize risk and provide modest growth, which is often attractive to risk-averse first-time investors.

Another investment management firm saw its investment products grow by 10 percent a year by developing a comprehensive range of products to suit customer needs, including multi-asset products and pension plans. The firm’s number of savings plans, many of which were opened by the younger generation, increased by around 40 percent between 2020 and 2021. Key success factors for this growth include providing clients with extensive support services, such as business planning and management advice, and expanding the ways in which the firm engages with its customers, including sales events and analogue and digital channels. The firm also developed a direct-to-consumer and business-to-business-for-consumer (B2B4C) platform that offers digital advice to both end consumers and financial advisors.

A national bank provided a way to educate members of the public, including children and university students, on financial matters. The bank launched a portal containing resources and information on a variety of topics including family finances, financial planning, savings, and investment principles. It also provided financial education activities in schools and educational centers, and hosted webinars for university students. To date, over 30,000 students have attended financial literacy lectures, over 8,000 children have passed the initiative’s financial literacy quiz, and more than 14,000 children have received financial literacy exercise books.

By drawing on these successes in other countries, Romanian stakeholders could collaborate to improve product offerings, increase the quality and availability of financial education and advice, and work with the public to help them reach their goals of saving and investing. Public institutions, financial institutions, and the education sector could find ways to increase access to financial literacy, for instance by offering programs in schools, and making existing initiatives more-widely accessible. Financial institutions could modify products to appeal to a younger demographic, for instance through gamification, and financial advisors could approach the topical subject of inflation and explain clearly to clients how inflation is likely to affect their purchasing power and savings, and how financial products with implicit or explicit inflation protection might be beneficial.

But change may not happen in the short term, particularly when low income and high debt are drivers of low savings rates. But broader attitudes and behaviors such as risk aversion and mistrust can be overcome through greater financial awareness, and access to reliable information.

Such efforts could have significant positive implications for individual consumers, and for the country. If Romanians were to make savings a priority, supported by relevant public and private initiatives, this could lead to a cumulative contribution of €575 billion to the country’s GDP by 2050 (in real terms, indexed to 2010), according to our analysis. In this scenario, Romania would reach the current level of savings in the Czech Republic, for example. By comparison, this value is approximately the current GDP of Poland (at €520 billion in 2010 prices).

By increasing savings, and redirecting them to investments, Romania has an opportunity to increase GDP by an additional 10 percent by 2050—when compared to the expected increase in GDP if no action is taken. Doing so would not only increase individual’s net wealth, but have positive effects on the labor market, productivity, and innovation. Such an approach would certainly be a passport to greater prosperity for future generations.