My colleague and co-author Chris Bradley recently wrote about the perils of the social side of strategy —how “egos and competing agendas, biases and social games” affect the decisions made in the strategy room. There is another dangerous pitfall that I often see trip up management teams striving to develop corporate strategies: the tendency to seek certainty when you should be gauging odds.

Consider the difference between poker and golf. In general, the more skill is involved in a game, the less you need to think about probabilities. If I played a world-class golfer -someone like Bernhard Langer or Rory McIlroy -I’d never win a game against him. On the other hand, the more that luck (or uncertainty) is involved, as in poker, the more you need to ponder the odds. In poker, I’d not only have a chance to win a hand against a world-class player like Phil Hellmuth but would even occasionally beat him, as people do. Hellmuth would certainly beat me over time, but, in the short run, I’d have a chance.

In business, as in poker, there is uncertainty, and strategy is about how to deal with it. Accordingly, your goal is to give yourself the best possible odds. People shouldn’t just get credit for winning and demerits for losing. If five companies each have an 80% chance of succeeding, that still means that one will usually fail. If five companies each have a 20% chance of success, one of the five is still likely to win. Clearly, the superior strategy is the one with an 80% chance of success.

In business, as in poker, there is uncertainty, and strategy is about how to deal with it

Risk, of course, needs to be part of the probability discussion, too. If you have just a slim chance of winning, but a bet costs you little and the potential win is huge, that still may be an investment worth making. The converse is true, too: An expensive investment that generates a high probability of a small success may be a bad idea. Poker players refer to their calculations as “pot odds.” If a $100 bet gives you a 20% chance of winning a $200 pot, you fold. Essentially, you’re paying $100 for $40—that 20% of the $200. But a $100 bet that gives you a 20% chance of winning a $2,000 pot is one you make every time, because you’re paying $100 to get $400—20% of $2,000. Likewise, in business, an assessment of your odds—in terms of competitive, market or regulatory factors—needs to be part of your calculation.

What are your odds?

In a recent post, Martin Hirt, another McKinsey colleague and co-author, described the Power Curve of economic profit - the result of a four-year study we recently conducted that is the subject of our upcoming book, Strategy Beyond the Hockey Stick.

Chris Bradley explains the characteristics of the Power Curve here:

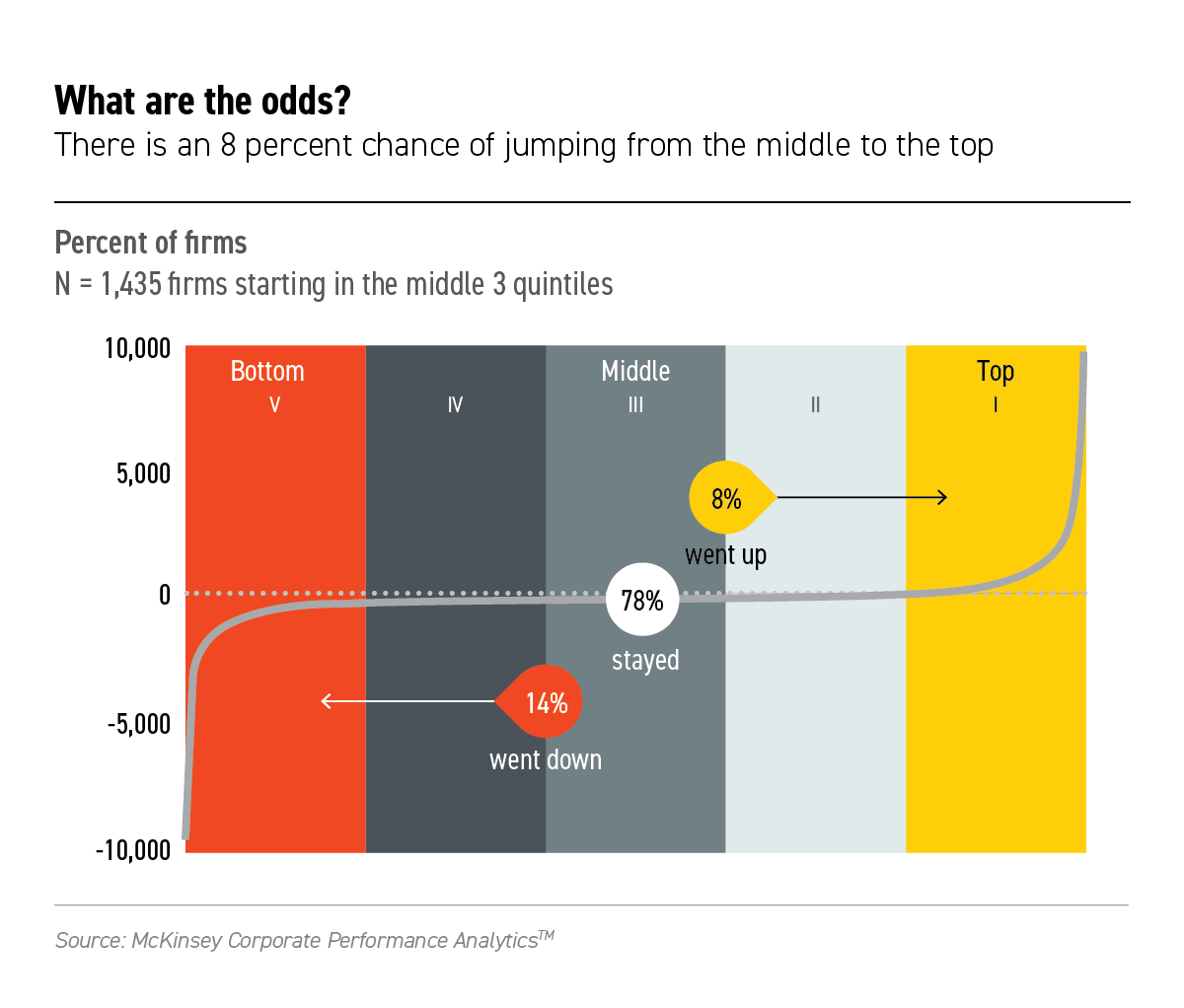

The Power Curve shows a broad swath of companies with middling performance bracketed by steep tails. But what are the odds of moving up or down the curve? At the highest level, your odds of making a move across the quintiles over a 10-year period, if you started in the middle three quintiles, are shown in the chart below.

As you can see, your odds of going from the middle quintiles to the top quintile are 8%.

Eight percent!

Let that sink in for a moment. Of all those strategies that boldly projected growth and got approved a decade ago, not even 1 in 10 made it. And the entire curve is rather sticky. Almost 80% of firms in the flat middle stayed there over the decade we studied.

The odds of individual business units moving up and down the performance curve are roughly the same as for companies. And, when companies make a big move up the curve, it is mostly because one, or at most two, of their businesses made a hockey stick-style surge. Think about that for a moment. If you have a portfolio of 10 businesses, chances are that only one will break out over a 10-year period—and correctly identifying that one and feeding it all the resources it needs will most likely determine whether your company as a whole can make a significant move up the Power Curve.

Where are the odds in the strategy room?

Nevertheless, conversations in the strategy room rarely consider strategic odds. Instead, they tend to mirror the discussion at one consumer goods company with the aspiration of achieving double-digit growth. The firm did a great deal of planning, and the aspiration looked reasonable. But its plan was based on an inside view, building from bottom-up estimates of the business units. A straightforward bit of research showed that, among its industry peers within the same revenue range, only 10% generated sustained double-digit growth over 10 years. The question became: Is our strategy actually better than 90% of our peers? Really? Even though we’d performed like an average company over the prior five years?

In weighing the odds of different strategic options comes the explicit realization of risk, and loss aversion kicks in. That’s because, in strategy rooms, there is a push toward certainty. The work usually begins by entertaining lots of ideas, and then testing and refining them with the goal of reducing uncertainty. Forcing yourself to think in terms of probabilities works against that desire for certainty. As one CEO in Italy told me, “I can’t handle multiple realities.”

With probabilities in the room, evaluating performance becomes uncomfortably complex. The situation resembles that of the FBI office that hears about a gang intending to rob one of three banks. The head of the office dispatches teams to all three banks. Obviously, only one team will capture the gang, but the entire unit should share in the praise and rewards. But we know that, most of the time, only the ones who are in the right place at the right time will be lauded as heroes. Even if you get management to think in terms of probabilities, those probabilities may be forgotten at the end of the year when it comes to performance evaluations. Either you made your numbers, or you didn’t.

Ed Catmull, president of Pixar, for one, is very deliberate about allowing for noble failures. The company labels some projects as being “experimental”—not aimed at theatrical release—to encourage people to try riskier ideas. It also funds some ideas considered to be “unlikely,” so failure does not become a stigma. “We have to try extra hard to make it safe to fail,” he told us.

Calibrating your odds

The CEO needs to know what the odds really are in order to be able to calibrate goals and compensation appropriately. It’s not only hard to set the right goals at the start of the year but difficult to sort out causality at the end of the year. Did success come because of managerial decisions and great execution, or because of an error by a competitor and a favorable market? Did problems occur because bad weather killed demand during the key buying season, or because managers misjudged their customers?

While the odds of moving up the Power Curve, on average, are just 8%, the odds for individual companies vary widely. The obvious questions for CEOs, managers, and investors, of course, are: What is my strategy’s probability of success, and what actions can we take to improve that probability? Real hockey stick plans do exist—you just need to know which ones are real and which ones are fake. I’ll tackle how to calculate those odds in a future blog.

I am a senior partner in McKinsey and Company’s Amsterdam office and leader of our Western European region. I am also the author, with Martin Hirt and Chris Bradley, of the forthcoming book, Strategy Beyond the Hockey Stick: People, Probabilities and Big Moves to Beat the Odds, available February 13, 2018.

Originally published on LinkedIn