The future of capitalism is here, and it’s not what any of us expected. With breathtaking speed, in the autumn of 2008 the credit markets ceased functioning normally, governments around the world began nationalizing financial systems and considering bailouts of other troubled industries, and major independent US investment banks disappeared or became bank holding companies. Meanwhile, currency values, as well as oil and other commodity prices, lurched wildly, while housing prices in Spain, the United Kingdom, the United States, and elsewhere continued to slide.

As consumers batten down the hatches and the global economy slows, senior executives confront a more profoundly uncertain business environment than most of them have ever faced. Uncertainty surrounds not only the downturn’s depth and duration—though these are decidedly big unknowns—but also the very future of a global economic order until recently characterized by free-flowing capital and trade and by ever-deepening economic ties. A few months ago, the only challenges to this global system seemed to be external ones like climate change, terrorism, and war. Now, every day brings news that makes all of us wonder if the system itself will survive.

The task of business leaders must be to overcome the paralysis that dooms any organization and to begin shaping the future. One starting point is to take stock of what they do know about their industries and the surrounding economic environment; such an understanding will probably suggest needed changes in strategy. Even then, enormous uncertainty will remain, particularly about how governments will behave and how the global real economy and financial system will interact. All these factors, taken together, will determine whether we face just a few declining quarters, a severe global recession, or something in between.

Uncertainty of this magnitude will leave some leaders lost in the fog. To avoid impulsive, uncoordinated, and ultimately ineffective responses, companies must evaluate an unusually broad set of macroeconomic outcomes and strategic responses and then act to make themselves more flexible, aware, and resilient.

Strengthening these organizational muscles will allow companies not only to survive but also to seize the extraordinary opportunities that arise during periods of vast uncertainty. It was during the recessionary 1870s that Rockefeller and Carnegie began grabbing dominant positions in the emerging oil and steel industries by taking advantage of new refining and steel production technologies and of the weakness of competitors. A century later, also in a difficult economy, Warren Buffett converted a struggling textile company called Berkshire Hathaway into a source of funds for far-flung investments.

What we know

The financial electricity that drives our global economy is not working well. Turning it back on isn’t just a matter of flicking a switch, as central banks and governments have tried to do by providing liquidity, guaranteeing debt, and injecting capital into banks. We must repair the grid itself significantly, and this will require coordinated global action.

By the grid, we mean the global capital market, which evolved over a 35 year period following the breakdown of the Bretton Woods accord, in the 1970s. No one designed the global capital market, but it has been a boon to humanity, stimulating globalization and growth by enabling the free international flow of capital and trade. The financial crisis of 2008 severely damaged this useful system. Through greed, neglect, or ignorance, the participants abused it until they broke some of its basic mechanisms.

The implications are far reaching. Most obviously, congestion in the global capital market is exacerbating the US domestic credit crisis. That crisis has spread globally, hitting Europe especially hard. Banks until recently have been scrambling for deposits to replace sources of funding such as direct-issue commercial paper, medium-term notes, and asset-backed paper. The search for deposits is required to finance existing loans, and borrowers will need significantly more of them because all but the strongest have, like the banks, lost access to the securities markets. The US government, in particular, has aggressively tried to address this problem through huge liquidity programs, such as the purchase of mortgage- and other asset-backed securities. But it remains to be seen how effective those efforts will be in mitigating the credit crunch.

The global capital market crisis worsens this credit crunch by sending into reverse the dynamic of cross-border investment and trade flows. A dollar of capital must finance every dollar of trade, so the global capital market has stimulated the international exchange of goods and services. It has facilitated cross-border investments—in intellectual property, talent, brands, and networks—that help economies and companies grow and profit, and it has enabled the companies that make such investments to repatriate their profits. In short, global integration and growth will revive only if the global capital market does. Yet it has sustained a body blow that will have repercussions for years, even if international leaders make the necessary long-term adjustments.

The changing role of government

Since September 2008, governments have assumed a dramatically expanded role in financial markets. Policy makers have gone to great lengths to stabilize them, to support individual companies whose failure might pose systemic risks, and to prevent a deep economic downturn. We can expect higher tax rates to pay for these moves, as well as for the reregulation of finance and many other sectors. In short, governments will have their hand in industry to an extent few imagined possible only recently.

That’s not all. Protectionism and nationalism will probably feature more prominently in policy debates. We may see not only old-style populist anger against business, high executive compensation, and layoffs but also the emergence of authoritarian populist movements. Already-dilatory trade discussions will encounter renewed resistance. Although greater global coordination is sorely needed, national political pressures will make it hard to achieve. All this will constrain some business activities but also opens the door to new ventures that depend upon collaboration between the public and private sectors.

Deleveraging

The cheap credit of the past few years most likely won’t return for a long time. For many households, this will mean reducing consumption and postponing retirement; for financial institutions—increasingly, bank holding companies—much higher capital requirements, less freedom to operate and innovate, and probably lower profitability; for governments, even more limited resources for health care, education, pensions, infrastructure, the environment, and security; and for corporations, a different role for capital. More broadly, for many companies the high returns and rapid growth of recent years rested on cheap credit, so deleveraging means that expectations of baseline profitability and economic growth, as well as shareholder returns, must all be seriously recalibrated.

New business models and industry restructuring

Companies engaging with the capital markets will encounter funders who are less tolerant of risk, a reduced ability to hedge it, and greater volatility. Hardest hit will be business models premised on high leverage, consumer credit, large customer-financing operations, or high levels of working capital. Businesses with long or inflexible production cycles or very long-term investment requirements will find it especially difficult to manage their funding. Some won’t make it, so industries will restructure. Corporate leaders already recognize this: in a McKinsey Quarterly executive survey launched the day after the US presidential election, 54 percent of the respondents expected their industries to consolidate.

These are all truths we know. They require a significant shift in thinking about government as a stakeholder, the value talent creates when it is harder to leverage, how to conserve capital, and strategies for sound risk taking—among other things.

What we don’t know

Yet there is much that we don’t know, and won’t for some time: how well will governments work together to develop effective regulatory, trade, fiscal, and monetary policies; what will these responses mean for the long-term health of the global capital market; how will its health or weakness influence the pace and extent of change in areas such as the economic role of government, financial leverage, and business models; and what will all this imply for globalization and economic growth?

Although these questions won’t be answered in the short or even the medium term, decisions made in the immediate future are critical, for they will influence how well organizations manage themselves now and compete over the longer haul. The winners will be companies that make thoughtful choices—despite the complexity, confusion, and uncertainty—by assessing alternative scenarios honestly, considering their implications, and preparing accordingly.

In particular, organizations must think expansively about the possibilities. Even in more normal times, the range of outcomes most companies consider is too narrow. The assumptions used for budgeting and business planning are often modest variations on baseline projections whose major assumptions often are not presented explicitly. Many such budgets and plans are soon overtaken by events. In good times, that matters little because companies continually adapt to the environment, and budgets usually build in conservative assumptions so managers can beat their numbers.

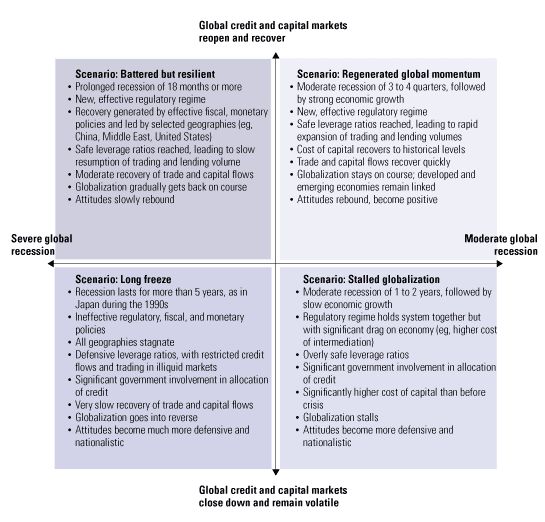

But these are not normal times: the range of potential outcomes—the uncertainty surrounding the global credit crisis and the global recession—is so large that many companies may not survive. We can capture this wide range of outcomes in four scenarios (exhibit).

Hard, harder, hardest times

To see them in perspective, consider some results of the McKinsey Global Institute’s research (see sidebar, “The credit crunch and the real economy”). This research, focusing on the United States, the center of the storm, suggests that if capital markets rebound quickly, GDP would be 2.9 percentage points lower than it would have been if trend growth had continued over the next two years. If financial markets take longer to recover, as the middle two scenarios envision, US GDP growth could fall 4.7 to 6.7 percentage points from trend over the same period. At the “long freeze” end of the spectrum, Japan’s “lost decade” shaved 18 percentage points from GDP compared with its previous growth trend.

Regenerated global momentum

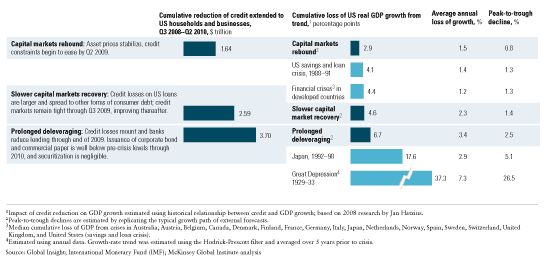

The credit crunch and the real economy

Something extraordinary happened from mid-2007 to mid-2008: net new borrowing by US households and companies plunged 65 percent ($1.4 trillion). This drop abruptly reversed recent trends. During the previous eight years, borrowing had grown by 2.4 percent a year, much faster than it did from 1970 to 2000, when the rate was 0.9 percent.

Credit growth has been correlated with faster GDP growth—consumer borrowing fuels sales of homes, autos, consumer electronics, and more; businesses issue debt to finance new plants and construction. Deleveraging will therefore have a significant effect on the real economy. To understand that impact, we assessed how much further borrowing by households and companies could decline over the next two years in each of the five channels they use to obtain credit and then modeled the resulting reduction in US GDP growth.

Loans from banks: US banks are still writing off credit losses and facing rising defaults on many types of loans. McKinsey analysis suggests that total credit losses on US loans could reach $1.4 trillion to $2.2 trillion, eroding bank equity.1 Although banks have raised new capital from the government and private investors, the credit crunch will continue for some time. After taking into account recapitalization, the reduction in bank leverage ratios, and taxes, we calculate that bank lending to US households and companies could decline by $1.9 trillion to $3.5 trillion from trend over the next two years.2

Lending by nonbank intermediaries: Companies also borrow from pension funds, insurance companies, and the government. This $1.7 trillion source of credit has already been drying up. We assume that this trend will continue over the coming two years as these intermediaries regroup after suffering large portfolio losses.

Debt owned or securitized by government-sponsored enterprises, such as Fannie Mae and Freddie Mac: These giant entities account for nearly 40 percent of credit to US households ($5.1 trillion in the second quarter of 2008). This is the only channel that has increased its lending throughout the crisis, offsetting some of the private-sector credit reduction. We assume that this countercyclical lending activity will continue, offsetting part of the reduction in credit through other channels.

Corporate bond and commercial-paper markets: Borrowing through debt capital markets in the form of bonds or commercial paper is a major source of funding to companies, second only to banks. Although issuance by investment-grade nonfinancial companies declined only modestly, high-yield bonds have declined much more sharply. In our model, issuance continues to decline for the next several quarters and revives in 2009 and 2010 in different recession scenarios.

Securitization markets: Borrowing through private lenders that securitize mortgages, consumer debt, and commercial loans has fallen sharply during the crisis. In our most severe deleveraging scenario, we assume that only the plain-vanilla forms of securitization revive, while some of the more exotic structured products do not.

Adding up the reduction of credit through each of the five channels, we estimate that US household and corporate borrowing could decline by an additional $1.6 trillion to $3.7 trillion over the next two years, depending on the size of credit losses and the speed of the capital markets’ recovery. US economic growth is likely to slow significantly as a result (exhibit).

An uncertain future: Three scenarios for deleveraging

A $1.6 trillion drop implies that US real GDP would be 2.9 percentage points lower than trend growth over the next two years—less than it fell during the recession following the US savings and loan crisis of the 1980s. In a $2.6 trillion drop, credit losses would spread from mortgages to credit cards, car loans, and other forms of consumer debt, and credit markets would remain tight through the third quarter of 2009. The resulting cumulative decline in GDP from trend would be 4.7 percentage points through mid-2010. That would be the worst US recession since 1981 and worse than the financial crises in other developed countries, such as Finland, Sweden, and the United Kingdom. Finally, a $3.7 trillion drop would reflect much larger credit losses for banks and tight credit markets through the middle of 2010 as a result of continuing declines in corporate profits and home prices. The cumulative GDP decline through mid-2010 would be 6.7 percentage points compared with trend.

Each of these scenarios depends on many assumptions and comes with caveats, which offer cause for either hope or worry. The actual GDP loss might be lower, for example, if the government’s aggressive policy responses work. Conversely, the results could be worse if an unexpectedly large decline in household wealth causes a steeper decline in consumer spending, if US business confidence erodes more rapidly and severely than in previous recessions, if the securities market remains inaccessible to banks and other corporate borrowers for an extended time, if the global capital market proves hard to repair, or if economic pain triggers a protectionist backlash that derails globalization.

The worst of these possibilities would occur only if policy makers and business leaders made serious mistakes of the sort that produced Japan’s “lost decade” (which shaved 18 percentage points off GDP growth) and the Great Depression (with its cumulative GDP loss of nearly 40 percentage points compared with trend). Job one for government and business leaders today is to avoid repeating those mistakes.

In the most optimistic scenario, government action revives the global credit system—the massive stimulus packages and aggressive monetary policies already adopted keep the global recession from lasting very long or being very deep. Globalization stays on course: trade and capital flows resume quickly, and the developed and emerging economies continue to integrate as confidence rebounds quickly.

Battered but resilient

In the second scenario, government-wrought improvements in the global credit and capital market are more than offset—for 18 months or more—by the impact of the global recession, which leads to further credit losses and to distrust of cross-border counterparties. Although the recession could be longer and deeper than any in the past 70 years, government action works, and the global capital and credit markets gradually recover. Global confidence, though shaken, does rebound, and trade and capital flows revive moderately. Globalization slowly gets back on course.

Stalled globalization

In the third scenario, the global recession is significant, but its intensity varies greatly from nation to nation—in particular, China and the United States prove surprisingly resilient. The integration of the world’s economies, however, stalls as continuing fear of counterparties makes the global capital market less integrated. Trade flows and capital flows decline and then stagnate. The regulatory regime holds the system together, but various governments overregulate lending and risk, so the world’s banking system becomes “oversafe.” Credit remains expensive and hard to get. As attitudes become more defensive and nationalistic, growth is relatively slow.

The long freeze

Under the final scenario, the global recession lasts more than five years (as Japan’s did in the 1990s) because of ineffective regulatory, fiscal, and monetary policy. Economies everywhere stagnate; overregulation and fear keep the global credit and capital markets closed. Trade and capital flows continue to decline for years as globalization goes into reverse, and the psychology of nations becomes much more defensive and nationalistic.

Leading through uncertainty

These descriptions are intentionally stylized to enliven them; many permutations are possible. Scenarios for any company and industry should of course be tailored to individual circumstances. What we hope to illustrate is the importance for strategists of considering previously unthinkable outcomes, such as the rollback of globalization. Unappealing as three of the four scenarios may be, any company that sets its strategy without taking all of them into account is flying blind.

So executives need a way of operating that’s suited to the most uncertain business environment since the 1930s. They need greater flexibility to create strategic and tactical options they can use defensively and offensively as conditions change. They need a sharper awareness of their own and their competitors’ positions. And they need to make their organizations more resilient.

Most companies acted immediately in the autumn of 2008 when credit markets locked up: they cut discretionary spending, slowed investment, managed cash flows aggressively, laid off employees, shored up financing sources, and built capital by cutting dividends, raising equity, and so forth. While prudent, these actions probably won’t produce the short-term earnings that analysts expect, at least for most companies. In fact, it’s time they abandoned the idea that they can reliably deliver predictable earnings. Quarterly performance is no longer the objective, which must now be to ensure the long-term survival and health of the enterprise.

More flexible

Companies must now take a more flexible approach to planning: each of them should develop several coherent, multipronged strategic-action plans, not just one. Every plan should embrace all of the functions, business units, and geographies of a company and show how it can make the most of a specific economic environment.

These plans can’t be academic exercises; executives must be ready to pursue any of them—quickly—as the future unfolds. In fact, the broad range of plausible outcomes in today’s business environment calls for a “just in time” approach to strategy setting, risk taking, and resource allocation by senior executives. A company’s 10 to 20 top managers, for example, might have weekly or even daily “all hands on deck” meetings to exchange information and make fast operational decisions.

Greater flexibility also means developing as many options as possible that can be exercised either when trigger events occur or the future becomes more certain. Often, options will be offensive moves. Which acquisitions could be attractive on what terms, for instance, and how much capital and management capacity would be required? What new products best fit different scenarios? If one or more major competitors should falter, how will the company react? In which markets can it gain share?

As companies prepare for such opportunities, they should also create options to maintain good health under difficult circumstances. If capital market breakdowns make global sourcing too risky, for example, companies that restructure their supply chains quickly will be in much better shape. If changes in the global economy could make a certain kind of business unit obsolete, it’s critical to finish all the preparatory work needed to sell it before every company with that kind of unit reaches the same conclusion.

A crisis tends to surface options—such as how to slash structural costs while minimizing damage to long-term competitiveness—that organizations ordinarily wouldn’t consider. Unless executives evaluate their options early on, they could later find themselves moving with too little information or preparation and therefore make faulty decisions, delay action, or forgo options altogether.

More aware

As problems with credit destroy and remake business models and market volatility whipsaws valuations, companies desperately need to understand how their revenues, costs, profits, cash flows, risks, and balance sheets will fare under different scenarios. With that information, executives can plan for the worst even as they hope for the best. If the recession lasted more than five years, for example, could the company survive? Is it prepared for the bankruptcy of major customers? Could it halve capital spending quickly? The answers should help companies to be better prepared and to recognize, as early as possible, which scenario is developing. That is critical knowledge in a crisis, when lead times disappear quickly and companies can seize the initiative only if they act before the entire world understands the probable outcome.

Better business intelligence promotes faster, more effective decision making as well. Companies can often gain insights into the potential moves of competitors by weighing news reports about their activities, stock analyst reports, and private information gathered by talking to customers and suppliers. Such intelligence is always important; in a crisis it can make the difference between missing opportunities to buy distressed assets and leaping in to snare them.

To get this kind of business intelligence, companies need a network, typically led by someone with strong support from the top. This executive’s mandate should include creating “eyes and ears” across businesses and geographies in particular areas of focus (such as the competition’s response to the crisis), as well as gathering and exchanging information. A network is critical because information is most useful if it moves not just vertically, up and down the organization, but also horizontally. Salespeople in a network, for example, should exchange knowledge about what’s working in economically distressed regions so that employees can help each other.

Assembling bits of information, facts, and anecdotes helps companies to make sense of what’s happening in an industry. Say, for example, that a supplier says it has no difficulties with funding, though first-hand knowledge from other sources indicates that the company is struggling to meet its payroll. Such warnings can allow executives to get a full picture much more quickly than they could by sitting in their offices and interacting only with direct subordinates.

More resilient

A crisis is a chance to break ingrained structures and behaviors that sap the productivity and effectiveness of many organizations. Such moves aren’t a short-term crisis response—they often take a year or more to pay dividends—but are valuable in any scenario and could help a company survive if hard times persist. Although employees may dislike this approach, most will understand why management aims to make the organization more effective.

This may, for example, be the time to destroy the vertical organizational structures, retrofitted with ad hoc and matrix overlays, that encumber companies large and small. Such structures can burden professionals with several competing bosses. Internecine battles and unclear decisions are common. Turf wars between product, sales, and geographic managers kill promising projects. Searches for information aren’t productive, and countless hours are wasted on pointless e-mails, telephone calls, and meetings.

Experience shows that streamlining an organization to define roles and the way those who hold them collaborate can greatly improve its effectiveness and decision making. When jobs must be eliminated, the cuts mostly reduce unproductive complexity rather than valuable work. As Matthew Guthridge, John R. McPherson, and William J. Wolf point out in “Smart cost-cutting in the downturn: Upgrading talent” (available on December 4), Cisco took that approach in shedding 8,500 jobs in 2001. When the company redesigned roles and responsibilities to improve cooperation among functions and reduce duplication of effort, talented employees were more satisfied in a more collaborative workplace.

In fact, many functional areas offer big opportunities: greater effectiveness, lower fixed costs, freed-up capital, and reduced risk. This could be the moment to redefine and reprioritize the use of IT to increase its impact and cut its cost. Other companies could seize the moment to control inventory; to reexamine their cash flow management, including payments and receivables; or to change the mix of marketing vehicles and sales models in response to the rising cost of traditional media and the growing effectiveness of new ones.1

As customer preferences change, competitors falter, opportunities to gain distressed assets emerge, and governments shift from crisis control to economic stimulus, the next year or two will probably produce new laggards, leaders, and industry dynamics. The future will belong to companies whose senior executives remain calm, carefully assess their options, and nurture the flexibility, awareness, and resiliency needed to deal with whatever the world throws at them.

Related Articles