To some extent, the rebalancing of global economic activity from developed to emerging markets simply reflects economic laws of gravity. In a world where ideas can flow freely and countries are at different stages in adopting modern modes of production, communication, and distribution, less developed nations should grow more rapidly than their counterparts in the West as they catch up.

But it’s also important to understand that emerging-market economies have a structural advantage that is grounded in the operation of the global economy. Saber-rattling Western trade negotiators frequently focus their attention on the “unnaturally” depressed exchange rates of countries such as China, and this is a component of the structural advantage to which I refer. But its roots run far deeper—all the way down to the fundamental issue that labor can’t be freely traded on a single global market, while capital and commodities can. Any company sourcing its production or service operations in a lower-wage emerging-market country therefore can save enormously on labor costs. That’s painful for displaced Western workers, but it’s good for the company’s profits, good for consumers in developed markets, and good for the newly minted citizens of the global economy who are working in emerging-market factories and call centers. This is a dynamic we take so much for granted that it’s easy to imagine it as a semipermanent condition that will underpin global economic development for the foreseeable future.

But what if it weren’t? This article explains why we should consider that seeming improbability and examines the possibility that financial crises may accelerate the transition to a global economy with more balanced trade, capital flows, and consumption. I believe senior executives need to prepare now for a world that—as China’s recent decision to relax its informal peg of the yuan to the US dollar underscores—will be coming to grips with an unsustainable set of economic relationships. Their unwinding will have serious long-term implications for those executives’ strategic priorities, including where they locate operations and what customers they serve in which markets. Equally important is the need for preparedness in case the unwinding process is sudden and abrupt. While we surely seem to be headed toward a new global equilibrium, the transition to that future world may not be smooth and gradual.

Adam Smith meets the global economy

We usually think of the global economy in terms of outputs such as cars and packaged goods. Yet the real integration of the world’s economy begins with factors of production. Of those, commodities, capital, and labor are the most important for understanding our structural economic issues. The test of whether a market has fully formed is whether all customers get the same items at the same price, allowing for transaction and transportation costs. (This condition, called the law of one price, was originally advanced by Adam Smith.) Such market conditions have long existed at a global level for natural commodities, such as crude oil, bauxite, and iron ore, as well as for manufactured commodities, such as petroleum, aluminum, and steel. The law of one price also exists for freely traded foreign exchange and most instruments traded in the capital market. It does not exist for labor, however—which is the fundamental structural issue the global economy faces.

To understand labor’s role, of course, you need to understand arbitrage. Cross-border arbitrage in the financial economy focuses on tradable instruments denominated in various currencies. In the real economy, such arbitrage focuses on capturing differences in the cost of production across geographies. As markets have opened and transaction and transportation costs fallen over the past quarter century, arbitrage opportunities in global financial markets and commodities have been quickly exhausted, so they easily meet the global law-of-one-price test. Yet there are still enormous arbitrage opportunities available in labor rates: the cost of performing the same job in different nations can vary significantly. As a result, multinational corporations that are able to source their production in emerging markets can enjoy large labor cost savings.

Until recently, labor arbitrage across countries was hard to capture because high-quality, highly productive labor was scarce in emerging markets. In the past decade, however, it has become relatively easy for companies to capture such opportunities, thanks to the combination of urbanization, education, infrastructure investments, new technology, the spread of advanced production techniques, and the evolution of digital standards. Even today, the cost of labor in China or India is still only a fraction (often less than a third) of the equivalent labor in the developed world. Yet the productivity of Chinese and Indian labor is rising rapidly and, in specialized areas (such as high-tech assembly in China or software development in India), may equal or exceed the productivity of workers in wealthier nations. Given such differences, more and more companies around the world are locating production in emerging markets.

Labor costs and currencies

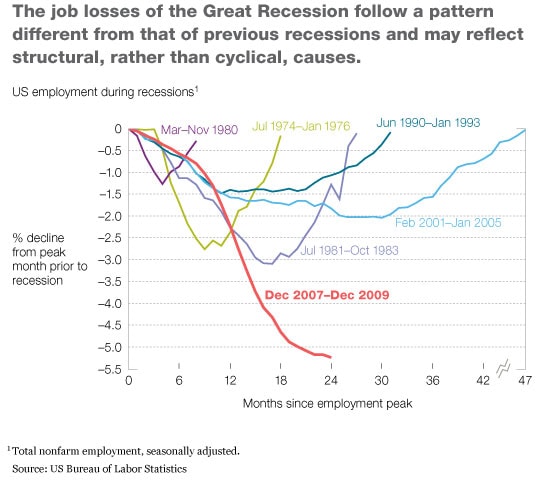

The structural issue facing developed-world nations is that the amount of high-quality, high-productivity labor that will be mobilized over the next decade in Brazil, China, and India (not to mention Mexico, the Philippines, and Thailand) is likely to be measured in the hundreds of millions of people. By comparison, the entire US labor force comprises 150 million people. This is a wonderful trend for humankind and would be a boon for everyone in the world if emerging-market employment were directed largely toward production for domestic consumption. The challenge for developed-world governments and citizens seeking jobs, however, is that a significant fraction of this emerging-world labor displaces jobs that would otherwise be created in Europe, Japan, and the United States. This may be the underlying reason why unemployment in Europe, Japan, and the United States is becoming more structural rather than cyclical and may get worse over time no matter how much public stimulus is provided. Certainly, the job losses of the Great Recession look quite different from those of past recessions (Exhibit 1).1

In a completely open global capital market, foreign-exchange rates would adjust until labor markets in the developed world began to be competitive again, even if it took a major currency revaluation to achieve competitive parity. However, exchange rates in countries such as India and China have often been subject to foreign-exchange controls and interventions of various kinds. The result is that exchange rates haven’t adjusted freely, leading to the shifting of developed-world service jobs offshore (particularly to India) and the migration of manufacturing jobs (particularly to China).

Assume, for the moment, that Europe, Japan, and the United States continue to run structural fiscal deficits and relatively loose monetary policies and to struggle with job creation. Also assume that China’s recent announcement of a return to the “managed floating exchange rate” that prevailed from 2005 to 2008 does not mark the end of currency market interventions by emerging-market nations. Both scenarios are likely, so tensions between developed-world currencies and emerging-market currencies will probably continue to build. In particular, as more and more emerging-market citizens capture job opportunities associated with production and services for developed-world nations, the structural pressures on advanced countries will continue to increase. For example, it’s hard to see how the United States can resume the rapid GDP growth necessary to reduce its fiscal deficit—which requires increased tax revenue and lower government spending—when almost 20 percent of its working population is unemployed or underemployed.

As the GDP growth of emerging-market nations continues to outstrip that of the developed world, the pressure on currency values will continue to build. Eventually, the tension must be released, and currency values will readjust. For all of us, the speed of that adjustment makes a big difference. The dollar and euro would need to be devalued by between 30 and 50 percent for financial foreign-exchange rates to reflect the purchasing-power-parity (PPP) exchange rates of emerging-market currencies more closely (and, therefore, for labor of equal quality and productivity to be priced relatively equally across geographies). An adjustment of this magnitude that took just a few weeks, rather than a few years, would obviously jolt the global economy.

Commodity complications

Commodities are a further complication. Ramping up production in China, India, and other countries to capture the economic returns from the increasing supply of high-quality, productive labor requires more commodities to produce more output. Since the global law of one price applies to commodities, this means that, with all else held equal, producers in China and India end up paying more than they would if those countries’ currencies were stronger. Simply put, commodity prices are too high in emerging-market countries and too low in developed-world countries.

As a result, developed-world consumers are using more commodities than they should, while emerging-market consumers are using fewer than they otherwise would. That’s distorting pricing feedback to customers and suppliers. What’s more, some of the returns that companies theoretically should be earning by taking advantage of low-cost, high-quality, productive labor in emerging markets is instead transferred to commodity-exporting nations. The resulting surpluses often then wind up in sovereign-wealth funds for deployment in the global capital market.

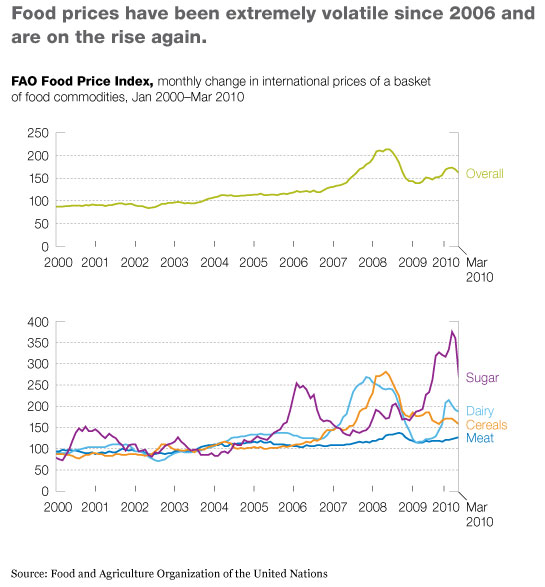

The fact that commodity prices, to a greater extent than currency values, are set in truly global markets where nations have little power over prices suggests that financial tensions will build earlier, and with greater volatility, in commodity than in currency markets. Some argue, in fact, that the last crisis was precipitated by the unbelievably rapid commodity price rise, in mid-2008, that saw oil jump to $140 a barrel, from $60 in early 2007, and coal increase to $170 a metric ton, from $50, over the same period. There are already signs that commodity prices are coming under pressure, even though developed-world growth remains relatively stagnant. Most commodity prices have doubled from their 2009 lows. Perhaps most disquieting, food prices have risen rapidly (Exhibit 2). It seems quite plausible that we could have a repeat of the commodity price movements of 2008 in late 2010 and 2011, even if developed-world GDP growth is only modest.

A dramatic increase in commodity prices could stall global economic recovery and also be the catalyst for emerging markets to revalue their currencies upward against the dollar and euro to reduce the high cost of imported commodities. Even the prospect of such a revaluation could cause large dollar and euro asset holders, such as sovereign-wealth funds, to accelerate the diversification of their holdings away from those currencies into foreign direct investment in emerging markets. That, in turn, could help trigger a currency crisis.

Adjustment uncertainty

It is very difficult to say how these issues will play out. The global rebalancing that is needed is obvious: developed-world countries need to save more, consume less, become more fiscally disciplined, and run current-account surpluses (or at least be neutral). Emerging-world countries need to let their currencies rise until PPP rates are closer to financial-exchange rates. They need to consume more, save less, run current-account deficits (or at least be neutral), and continue investing, with some of the capital provided by outsiders. If major national governments work proactively together to rebalance and coordinate their fiscal, monetary, trade, and foreign-exchange policies, the adjustment process could be gradual.

But such a policy adjustment is easier said than done. Developed-world politicians must respond to the demands of voters who don’t understand how the global economy works or what has changed in recent years and who mostly want policies that are fiscally unbalanced. They generally want governments to spend more money on social programs—in the United States, for example, on Social Security and Medicare—without increasing taxes to pay for that additional spending. The usual response by developed-world governments to such dilemmas is to run bigger fiscal deficits and to borrow more money. Yet most developed-world governments have been rapidly exhausting their debt capacity, and some nations, such as Greece, Portugal, and Spain, are already experiencing fiscal crises. At some point, the International Monetary Fund and major nations could become unable, or unwilling, to bail out overly indebted governments, at which point defaults and debt restructurings would become inevitable.

Emerging-market leaders have different challenges. In general, they have been “virtuous”: most have low debt-to-GDP ratios, maintain large currency reserves, continue to run current-account surpluses, and provide more capital to the developed world than they receive. Their economies are based upon undervalued currencies, low-cost labor, high savings rates, exports, and investment in infrastructure. These countries are wary of growing too rapidly or allowing too great a volume of capital inflows, particularly since, with undervalued currencies, they don’t want to sell their assets cheaply. They also are wary of anything that would derail their growth, given the rising expectations of their populations.

Both sides, of course, need to give way. In the longer term, the capital markets will discipline governments if the imbalances—particularly the fiscal imbalances of developed-world governments—continue to grow. But in the short term, the powerful market states involved (for instance, the United States, the eurozone countries, Japan, China, India, Brazil, and major commodity-exporting nations) are so large and can pull so many levers that they exercise significant power in the global capital market, resisting its discipline. If that’s the path they choose, it’s likely that the tensions created by unbalanced and divergent policies will build until they cause rapid currency shifts, massive changes in commodity prices, and punitive interest rate increases (or even defaults) for overly indebted sovereign borrowers.

The corporate agenda

Companies have much more freedom in the global economy than governments do. They can more easily capture the opportunities created by divergent, unbalanced government policies. They can position themselves to capture profits from both cross-geographic labor arbitrage and the consumption growth that results from rising incomes in emerging markets. They also have significant opportunities to serve the changing needs of aging populations in the developed world.2 The underlying global economic processes under way are very powerful, and the profit opportunities will be enormous as four billion people in emerging markets triple or quadruple their incomes and wealth over the next 20 years.

That said, business leaders should not be sanguine about what lies in store. Although it’s impossible to know in advance the speed or intensity of the needed adjustment, turmoil probably lies ahead. Here are four suggestions for executives hoping to get out in front of it:

-

For starters, as companies plot their global footprints, executives should not assume that the prevailing reality of globalization will continue. Labor arbitrage opportunities won’t disappear, of course, but strategies predicated on them could become less remunerative—maybe gradually or perhaps all at once.

-

Second, it would be wise to be prepared for the high probability of future financial shocks. To do so, most companies need to become more adept at risk management and to err on the side of being overcapitalized, overliquid, and overprepared.

-

Third, companies should engage in serious scenario planning around “unthinkables.” These might include the potential for significant, rapid shifts in currency values (for example, a 30 percent decline of the dollar versus emerging-market currencies); an exit from the euro by some nations; dramatic, rapid changes in commodity prices (for example, oil prices spiking to $200 a barrel); or defaults on debt by major nations.

-

Finally, multinational-company executives who set strategy in emerging markets need to stop saying that those markets may someday be at least as important as drivers of consumption as they are platforms for low-cost manufacturing or services—and to start acting as if that day was near. In an upcoming article, my colleagues Jeff Galvin, Jimmy Hexter, and Martin Hirt describe what it would mean for a multinational to treat China as its “second home” (see “Building a second home in China”). China’s scale makes its potential to transform the competitive balance of industries, and thus its importance, somewhat unique. But as currency adjustments bring purchasing power closer to parity around the world, the importance of emerging-market consumption will be reinforced everywhere. (For more on consumer segments in those markets, see “Capturing the world’s emerging middle class.”)

These suggestions represent specific applications of the more dynamic management approach I have urged companies to adopt in the past. The hallmarks of that approach—heightened awareness, greater resilience, more flexibility, and the timely alignment of leadership around needed adjustments—will be invaluable for companies as they navigate the choppy waters of global economic rebalancing. This process will continue and perhaps even accelerate in the years ahead, not despite, but because of the structural adjustments that are needed to put the global economy on a more sustainable trajectory.

Related Articles

Dynamic management: Better decisions in uncertain times