It takes courage to break up a company. CEOs and boards of directors often fear that investors will view asset divestitures as admissions of failed strategy—that having certain businesses under the same corporate umbrella never made sense. Many worry that shedding assets will cost a company the benefits of scale, cut into the advantages of analyst coverage, or even damage employee morale. Spin-offs in particular draw scrutiny because they shrink the size of the parent company but, unlike sales, don’t generate cash to reinvest.

We don’t believe these arguments hold up. What’s more, they may lead executives to pass up value-creating opportunities. A fundamental principle of corporate finance holds that a business creates the most value for shareholders and the economy as a whole when it is owned by the best—or, at least, a better—owner.1 So it makes sense that companies should continually reallocate their resources as circumstances change. Moreover, the benefits of being part of a large company come at a cost; in fact, many spun-off companies can make substantial cuts in overhead costs once they are independent. Investors typically don’t care about a company being too small once it reaches a threshold of about $500 million in market capitalization.2 And in our experience, executives and employees of spun-off companies often feel liberated and quite happy to be on their own.

So it’s a good sign that there’s been something of a revival in spin-off activity this year. According to Bloomberg, as of August 25, 174 companies had announced spin-offs of all sizes—quickly approaching the previous global record of 230, in 2006. Among the notable deals: Kraft Foods’s spin-off of its North American grocery unit and ConocoPhillips’s spin-offs of its downstream businesses.

The trick to executing a spin-off strategy—and to overcoming predictable objections to it—is to understand where the value is created. Markets typically respond favorably to spin-offs, but savvy managers understand that such deals create value not from some mechanical market reaction but from the sharpened strategic vision that comes with restructuring or the tax advantages relative to a sale.

Spin-offs: A brief history

Company breakups through spin-offs date back at least a hundred years. Many of the earliest and best-known ones were mandated by courts to split up monopolies, including the 1911 breakup of Standard Oil into 34 separate companies, as well as the 1984 breakup of AT&T into 8 companies.

After the AT&T breakup, spin-offs became a more common way for companies to change their strategic direction. American Express, for example, spun off Lehman Brothers in 1994, ending its strategy of becoming a financial supermarket. In 1993, as the historical links between chemical and pharmaceutical businesses became less relevant, the British chemical company Imperial Chemical Industries3 (ICI) spun off its pharmaceutical business as Zeneca.4 Recent spin-offs have reflected similar shifts. In 2008, when the integration of the production and delivery of media content didn’t lead to the anticipated benefits, Time Warner announced that it would spin off its cable television business.

Some of the major conglomerates built in the 1960s and ’70s used spin-offs to break themselves up. ITT, one of the best-known conglomerates of that era, used a double spin-off in 1995 to split itself into three companies, ITT Sheraton (now part of Starwood Hotels and Resorts), Hartford Financial Services, and the remaining industrial businesses, which kept the ITT name. In January 2011, ITT announced that it was further splitting up into three companies: ITT Corporation (industrial process and flow control), Zylem (water and waste water), and ITT Exelis (defense). In an even more extreme example, the company that was Dun & Bradstreet in 1995 has spun out businesses four times (1996, 1998, 1999, and 2000) and now exists as seven different companies.

Understanding the benefits

One common misperception about spin-offs is that they are quick fixes for low valuations. Managers see the typically favorable response that markets have to a spin-off announcement as confirmation that a spin-off itself mechanically illuminates value that investors previously overlooked. But that belief is misleading.

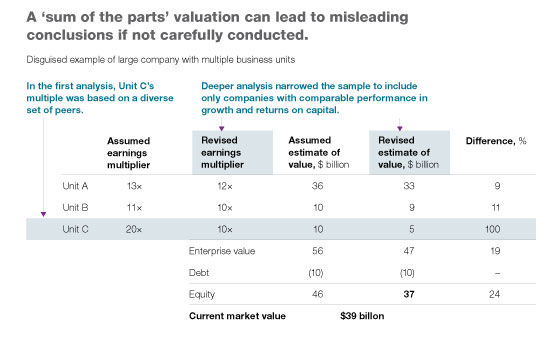

Such assumptions rest errantly on a “sum of the parts” calculation. For each of a company’s businesses, analysts add up an assumed earnings multiple based on the multiples of industry peers. If they find that the sum of the parts is greater than the market value of the company as currently traded, they assume the market hasn’t valued the business properly.

Unfortunately, these analyses often are flawed—usually because the selected peers are not actually comparable in industry, performance, or both. Once truly comparable businesses are identified, the undervaluation typically disappears (exhibit).

The real reason spin-offs are so valuable is tied to expected performance: increased valuations reflect the market’s expectation that performance will improve at both the parent company and the spun-off business once each has the freedom to change its strategies, people, and organization. Indeed, of the 85 spin-offs associated with a major restructuring5 of a company globally since 1992, spun-off businesses nearly doubled their growth rates and increased their operating profit margins by a median of 1.6 percent over five years. Among parent companies, profit margins increased 11 percent in the first year after the spin-off and an additional 3.5 percent by the fifth year.6 Also, one academic study concluded that spin-offs improve the allocation of capital, because researchers observed changes in strategy among spun-off businesses.7 They found that higher-profit businesses tended to increase their investment spending, while lower-profit ones tended to cut it.

This ability to change strategic direction is the biggest source of performance improvements. Consider, for example, Bristol-Myers Squibb, which spun off its Zimmer orthopedic-devices business in 2001 with an initial market value of $5.4 billion. Under Bristol-Myers Squibb, Zimmer relied on pricing to drive revenue growth. The separation allowed Zimmer to invest in developing new technologies, launch new products, and grow in new geographies. The company also more aggressively reduced costs by, for example, improving the efficiency of its manufacturing plants.

Another source of improvement is eliminating conflicts and potential conflicts between the parent and the spun-off company. The pharmaceutical company Merck, for example, spun off Medco, its pharmacy benefits manager, in 2003, with an initial market value of $6.6 billion. Because the parent company was an important supplier to Medco, there were long-standing questions about whether Medco gave preference to Merck drugs over those of other pharmaceutical companies. The separation eliminated that concern in Medco’s negotiations with customers and helped Medco accelerate its growth by shifting clients to generic drugs and a mail-order pharmacy.

Spun-off companies may also attract more desirable management talent. In 2007, Tyco International split itself into three companies: Covidien, Tyco Electronics, and the original Tyco International. Shortly after the spin-off, then-CFO Chris Coughlin described the advantages, reporting that the health care business, Covidien, had made significant strides in attracting new talent that would probably not have been attracted to the old Tyco.8 In a health care company with a clearly defined strategy, employees and prospective employees could see themselves advancing professionally while remaining in health care and playing a significant role in the business.

Sell or spin?

When executives decide to dispose of a business unit because their company is no longer a better owner of it, their first inclination is usually to sell it outright. Yet spinning off these units may have tax advantages over selling them. In fact, most early spin-offs were completed by UK- or US-based companies partly because the tax laws of those two countries treated most spin-offs as tax-free transactions. Several continental-European countries changed their tax laws, beginning in the late 1990s, to facilitate spin-offs. Since the 1998 breakup of Dutch telecommunications company KPN and TNT Post, more continental-European businesses have used spin-offs to break up their companies.

Tax benefits can make a spin-off preferable even if a potential buyer is willing to pay a sizable premium. In the United States today, for example, a company must pay income tax of 35 percent on any gain from the sale of a business but a spin-off can be structured as a tax-free transaction.

Consider a hypothetical example. ParentCo has decided to divest one of its business units, which—if spun off—would have a market capitalization of $1 billion. It also has a $1.3 billion offer from another company to buy the unit outright, reflecting a typical acquisition premium. Since ParentCo’s book value for the unit is $300 million, the outright sale would carry a tax liability of $350 million on a $1 billion gain on the sale, reducing after-tax proceeds to $950 million, less than the unit’s expected market capitalization. From a shareholder value perspective, taxes alone should make ParentCo seriously consider a spin-off rather than a sale.

Three factors determine the breakeven point: the tax rate, the premium from the sale, and the tax book value of the business relative to the sale price. Because of the tax dynamics, companies are more likely to spin off highly profitable businesses and sell less profitable ones. The ratio of the tax book value to the selling price is a good proxy for how profitable a business is. A highly profitable business may have a tax basis that is only 10 percent of the selling price. To break even between selling and spinning off, the company would need to receive a 46 percent premium on the sale. On the other hand, a low-profit business with a tax book value of 80 percent of the selling price would need to receive only an 8 percent premium to break even.9

In many cases, understanding the shareholder benefits that spinning off assets can have should provide executives with the dose of courage they may need to overcome resistance to this type of value-creating divestiture.