CEOs are naturally wary of some investments. Large capital projects in politically unstable countries, common among companies in the mining and oil and gas sectors; speculative R&D projects in high tech and pharmaceuticals; and acquisitions of unproven technologies or businesses in a wide range of industries all carry what many see as an above-average degree of risk. The potential returns are alluring, but what if the projects fail?

Weighing the pros and cons of such deals, executives delve into the usual cash-flow projections, where they often make one seemingly small adjustment: forgetting what many of them learned in business school, they bump up the assumed discount rates in their cost-of-capital calculations to reflect the uncertainty of the project. In doing so, they often unwittingly set these rates at levels that even substantial underlying risks would not justify—and end up rejecting good investment opportunities as a result.1 What many don’t realize is that assumptions of discount rates that are only three to five percentage points higher than the cost of capital can significantly reduce estimates of expected value. Adding just three percentage points to an 8 percent cost of capital for an acquisition, for example, can reduce its present value by 30 to 40 percent (depending on its long-term growth rate).

Moreover, increasing the discount rate embeds opaque risk assumptions into the valuation process that are often based on little more than a gut sense that the risk is higher. The problem arises because companies take shortcuts when they estimate investment cash flows. To calculate net present value (NPV), project analysts should discount the expected cash flows at an appropriate cost of capital. In many cases, though, they use only estimates of cash flow that assume everything goes well. Managers, realizing this, increase the discount rate to compensate for the potentially overstated cash flows.2

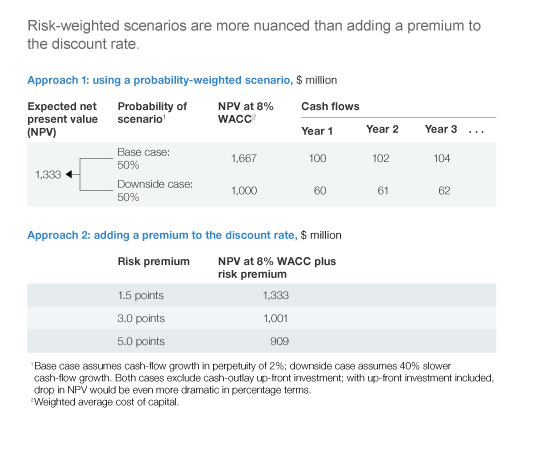

A better approach for determining the expected value of a project is to develop multiple cash-flow scenarios, preferably including at least one downside case, value them at the unadjusted cost of capital, and then calculate the average weighted by the probability that each will happen (Exhibit 1).

This approach has a number of practical advantages:

-

It provides decision makers with more information. Rather than being presented with a project with a single-point estimate of expected value—say, $100 million—decision makers know that there is a 20 percent chance that the project’s NPV is –$20 million and an 80 percent chance it is $120 million. This encourages dialogue about the risk of the project by making implicit risk assumptions explicit.

-

It encourages managers to develop strategies to mitigate specific risks, explicitly highlighting the value of a failed project or a smaller degree of success. For example, they might build more flexibility into a project with options for step-wise investments, scaling up in case of success and scaling down in case of failure. Creating such real options can significantly increase the value of projects.

-

It acknowledges the full range of possible outcomes. When project advocates submit a single scenario, they need it to reflect enough upside to get it approved—but also enough realism that they can commit to its performance targets. That often results in poor compromise scenarios. If advocates present multiple scenarios, they can show a project’s full upside potential, as well as realistic project targets that they can truly commit to—while also fully disclosing a project’s potential downside risk.

Managers applying the scenario approach should be wary of overly simplistic assumptions of, say, a 10 percent increase or decrease to the cash flows. A good scenario analysis will often lead to a high case that is many multiples of the typical “base” case. It will often also include a scenario with a negative NPV. In addition, there may not be a traditional base case. For many projects there is only big success or failure, with low likelihood that a project will just barely earn more than the cost of capital.

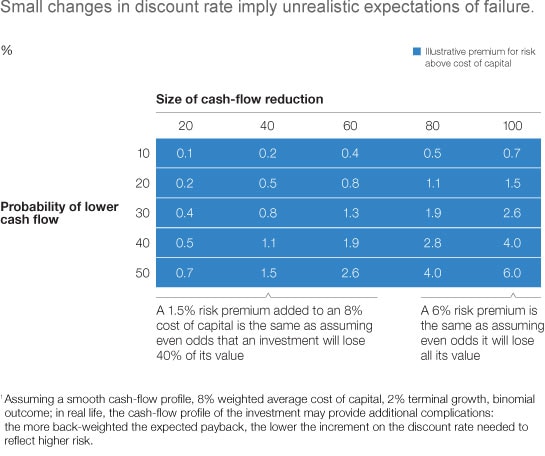

Managers who insist on adjusting the discount rate instead of evaluating scenarios should at least calibrate their markup to their best estimate of the amount that cash flows could fall below base-case assumptions and the probability of such drops occurring. Actual values will vary depending on the assumed cash-flow profile, cost of capital, and estimated terminal growth, but for illustrative purposes, if you believed that there was a 50 percent chance that cash flows would be 40 percent below the base case, you would only want to increase the discount rate by 1.5 percent—far below what we’ve seen many managers propose. Exhibit 2 shows appropriate discount-rate increments given fixed assumptions for cost of capital and cash-flow profile.

Marking up discount rates is a crude way to include project-specific uncertainty in a valuation. Scenario-based approaches have the dual appeal of better answers and more transparency on the assumptions embedded within them.